Markets rebounded sharply on Wednesday as unexpectedly robust U.S. economic data suggested the economy remains resilient despite escalating geopolitical tensions in the Middle East, with risk assets rallying broadly while the dollar weakened against most major currencies.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- Australia AIG Manufacturing Index for February 2026: -15.6 (-19.0 forecast; -19.4 previous)

- Australia GDP Growth Rate for December 31, 2025: 0.8% q/q (0.8% q/q forecast; 0.4% q/q previous); 2.6% y/y (2.5% y/y forecast; 2.1% y/y previous)

- Japan S&P Global Services PMI Final for February 2026: 53.8 (53.8 forecast; 53.7 previous)

-

China RatingDog Manufacturing PMI for February 2026: 52.1 (50.5 forecast; 50.3 previous)

- China RatingDog Services PMI for February 2026: 56.7 (51.7 forecast; 52.3 previous)

- Japan Consumer Confidence for February 2026: 40.0 (38.1 forecast; 37.9 previous)

- Swiss CPI Growth Rate for February 2026: 0.6% m/m (0.3% m/m forecast; -0.1% m/m previous); 0.1% y/y (0.0% y/y forecast; 0.1% y/y previous)

- Euro area HCOB Services PMI Final for February 2026: 51.9 (51.8 forecast; 51.6 previous)

- U.K. S&P Global Services PMI Final for February 2026: 53.9 (53.9 forecast; 54.0 previous)

- Euro area PPI for January 2026: 0.7% m/m (0.3% m/m forecast; -0.3% m/m previous); -2.1% y/y (-2.6% y/y forecast; -2.1% y/y previous)

- Euro area Unemployment Rate for January 2026: 6.1% (6.2% forecast; 6.2% previous)

- U.S. MBA Mortgage Applications for February 27, 2026: 11.0% (0.4% previous)

- U.S. MBA 30-Year Mortgage Rate for February 27, 2026: 6.09% (6.09% previous)

- U.S. ADP National Employment Report for February 2026: 63.0k (19.0k forecast; 22.0k previous)

- Canada Labor Productivity for December 31, 2025: -0.1% q/q (0.7% q/q forecast; 0.9% q/q previous)

- Canada S&P Global Services PMI for February 2026: 46.5 (46.0 forecast; 45.8 previous)

- U.S. S&P Global Services PMI Final for February 2026: 51.7 (52.3 forecast; 52.7 previous)

- U.S. ISM Services PMI for February 2026: 56.1 (53.0 forecast; 53.8 previous)

- U.S. EIA Crude Oil Stocks Change for February 27, 2026: 3.48M (15.99M previous)

Promotion: Use TradeZella’s AI Powered trade journal to deep-dive into your execution and see exactly how you performed during today’s trading session. Click here to get the TradeZella Edge and use code PIPS20 to save 20% on your subscription!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Wednesday’s session delivered a notable rebound in risk sentiment as stronger-than-expected U.S. economic data appeared to outweigh concerns about escalating Middle East tensions, with Bitcoin surging to lead gains across major asset classes.

Bitcoin posted the session’s strongest performance, rallying 7.39% to close around $73,041. The cryptocurrency benefited from a powerful risk-on rally that developed during the London and U.S. sessions, likely correlating with the surprisingly robust PMI releases in Europe and the US. The digital asset climbed steadily from its Asian session lows near $68,000, briefly touching $74,075 before settling near current levels. The move appeared to reflect broader appetite for speculative assets as traders focused on economic resilience rather than geopolitical risks.

Gold gained 1.00% to trade near $5,140 per ounce. The precious metal experienced relatively choppy trading through the Asian and London sessions before sliding a bit during U.S. afternoon hours. The overall advance likely reflected a mix of ongoing safe-haven demand amid Middle East uncertainties and a rebound from Tuesday’s dip, though the magnitude remained modest compared to Bitcoin’s explosive rally, suggesting investors were balancing caution against improving economic data.

The S&P 500 climbed 0.95% to close around 6,869, reclaiming ground lost in recent sessions. The equity rally accelerated following the 10:00 AM ET release of the ISM Services PMI, which registered 56.1 versus 53.0 expected, marking the highest reading since July 2022. The Business Activity component surged to 59.9 and New Orders jumped to 58.6, both well above forecasts. Technology shares led the advance, with investors interpreting the robust services data as evidence that the economy’s largest sector remains on solid footing despite ongoing geopolitical volatility.

WTI crude oil advanced 0.90% to settle near $74.90 per barrel. Oil prices traded in a relatively narrow range through most of the session, with the energy complex appearing to stabilize after recent volatility tied to concerns about potential disruptions to Persian Gulf shipping routes. The modest gain possibly reflected ongoing tensions surrounding the Strait of Hormuz, though prices remained well below recent spikes as traders assessed the actual impact on oil flows versus feared scenarios.

The 10-year Treasury yield rose 0.86% to approximately 4.10%. Yields climbed modestly as bond traders adjusted expectations following the stronger economic data, with the robust ISM Services report suggesting the Federal Reserve may maintain its restrictive policy stance longer than previously anticipated. The move came despite ongoing geopolitical uncertainties that would typically support safe-haven Treasury demand.

Promoted: Day traders & Scalpers have better odds of making great decisions if they see & hear market catalysts right away. Get the real-time feed that pros use to catch the news.

Join FinancialJuice for Free to learn more!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

FX Market Behavior: U.S. Dollar vs. Majors

Overlay of USD vs. Majors – Chart Faster With TradingView

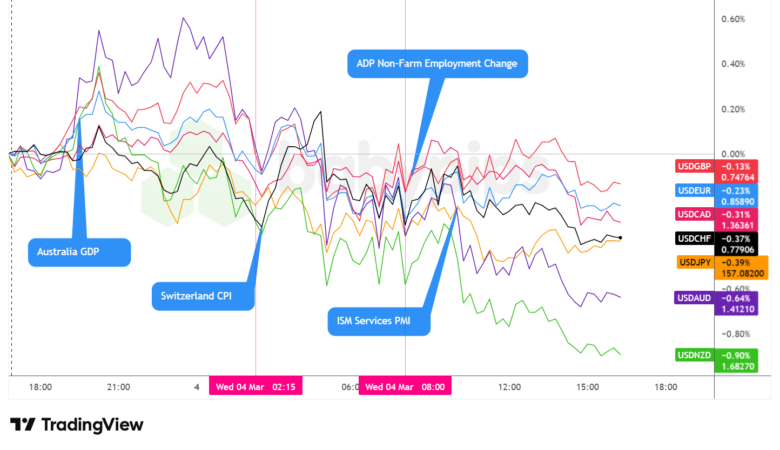

The U.S. dollar experienced a choppy trading session on Wednesday, ultimately closing as the worst-performing major currency despite early strength during Asian hours, as traders shifted focus from geopolitical risks to surprisingly robust U.S. economic data that bolstered risk appetite.

During the Asian session, the dollar traded mostly sideways and mixed, but arguably net positive up until just ahead of the London session open. The early strength possibly reflected ongoing safe-haven flows related to the U.S.-Iran conflict, with the war entering its fifth day and tensions remaining elevated across the Persian Gulf region. Australia’s Q4 GDP expanded 0.8% quarter-on-quarter, exceeding the 0.6% forecast and marking an acceleration from Q3’s 0.4% growth, while the annual rate came in at 2.6% versus 2.5% expected. However, the Australian dollar failed to benefit from the stronger data, trading lower against the greenback as risk-off sentiment from geopolitical tensions appeared to dominate positioning. Chinese PMI data disappointed, with the NBS Manufacturing PMI falling to 49.0 versus 49.9 expected, adding to regional growth concerns.

Ahead of the London session open, the dollar started to dip and continued to slowly move lower against the major currencies on net until the U.S. session opened. The shift possibly reflected profit-taking on recent dollar strength or positioning adjustments ahead of the key U.S. data releases scheduled for the American morning. European data releases provided mixed signals, with Swiss CPI coming in slightly above expectations at 0.1% year-over-year versus 0.0% forecast, while euro area Producer Price Index surged 0.7% month-over-month, well above the 0.3% consensus. The stronger inflation readings in Europe had minimal impact on dollar direction, as traders appeared focused on upcoming U.S. employment and services sector data.

During the U.S. session, the dollar rebounded slightly against the major currencies following the 8:15 AM ET ADP employment release, which showed private payrolls rising by 63,000 in February, crushing the 19,000 consensus and reversing January’s revised 11,000 gain. However, the greenback then pulled back lower once again ahead of the London close and during the U.S. afternoon session, particularly following the 10:00 AM ET ISM Services PMI release showing the index surged to 56.1 in February, jumping 2.3 percentage points above January’s 53.8 reading and marking the highest level since July 2022. The Business Activity Index accelerated to 59.9 from 57.4, while New Orders jumped to 58.6 from 53.1, both significantly exceeding forecasts.

The dollar’s weakness into the close appeared to reflect the market’s interpretation that robust economic data reduces immediate recession risks and supports risk assets, while the Prices Paid component declining to 63.0 from 66.6 suggested inflation pressures might be moderating despite strong activity levels. This combination appeared to fuel risk appetite at the dollar’s expense, with traders rotating into higher-yielding and risk-sensitive currencies.

Promoted: While new firms come and go with the volatility, The5ers has spent the last 10 years perfecting a funding model that works for the trader. It’s why over 1.6 million traders worldwide trust them to provide the capital and scaling needed to turn market analysis into meaningful professional growth.

Learn more about The5ers Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Upcoming Potential Catalysts on the Economic Calendar

- Australia S&P Global Services PMI Final for February 2026 at 10:00 pm GMT

- Australia AIG Manufacturing Index for February 2026 at 10:00 pm GMT

- Australia GDP Growth Rate for December 31, 2025 at 12:30 am GMT

- Japan S&P Global Services PMI Final for February 2026 at 12:30 am GMT

- Japan Consumer Confidence for February 2026 at 5:00 am GMT

- Swiss Inflation Rate for February 2026 at 7:30 am GMT

- Germany HCOB Services PMI Final for February 2026 at 8:55 am GMT

- Euro area HCOB Services PMI Final for February 2026 at 9:00 am GMT

- U.K. S&P Global Services PMI Final for February 2026 at 9:30 am GMT

- Euro area PPI for January 2026 at 10:00 am GMT

- Euro area Unemployment Rate for January 2026 at 10:00 am GMT

- U.S. MBA Mortgage Applications for February 27, 2026 at 12:00 pm GMT

- U.S. MBA 30-Year Mortgage Rate for February 27, 2026 at 12:00 pm GMT

- U.S. ADP National Employment Report for February 2026 at 1:15 pm GMT

- Canada Labor Productivity for December 31, 2025 at 1:30 pm GMT

- Canada S&P Global Services PMI for February 2026 at 2:30 pm GMT

- U.S. S&P Global Services PMI Final for February 2026 at 2:45 pm GMT

- ISM Services PMI for February 2026 at 3:00 pm GMT

- U.S. EIA Crude Oil Stocks Change for February 27, 2026 at 3:30 pm GMT

Thursday’s calendar features euro area retail sales data that could provide insight into consumer resilience amid ongoing economic headwinds, while ECB President Lagarde’s speech at 5:00 pm GMT will be closely monitored for any signals regarding the central bank’s policy trajectory following Wednesday’s stronger-than-expected inflation data from the PPI release.

The U.S. session brings weekly initial jobless claims and preliminary productivity data, though these releases may receive less attention than usual given that markets are still digesting Wednesday’s surprisingly robust ISM Services PMI reading. Productivity data could be particularly relevant for Federal Reserve policy considerations, as improving productivity would allow stronger economic growth without necessarily fueling inflation pressures.

Geopolitical developments remain a wildcard, with markets continuing to monitor escalation risks from the U.S.-Iran conflict. Any significant developments affecting Persian Gulf shipping routes or oil production facilities could quickly shift market sentiment away from economic data and back toward safe-haven positioning.

Stay frosty out there, forex friends!

Promoted: How Do Professionals Trade Geopolitical Shocks?

You’ve seen the retail reaction to the military strikes in the Middle East—now see the institutional one. Brent Donnelly’s “The Art of Currency Trading” (4.7 stars & 517 reviews on Amazon) bridges the gap between the news headlines you read and the execution on your screen. It’s a practical, “no-fluff” guide to how professional FX desks navigate the exact type of geopolitical volatility described in today’s report.

Learn more about “The Art of Currency Trading” at Amazon

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.