US President Donald Trump signed an government order on Aug. 7, permitting crypto in 401(ok) retirement plans. The crypto trade has referred to as the transfer a win for adoption, however funding professionals warn it comes with important threat.

The order “Democratizing Entry to Various Belongings for 401(ok) Traders” directed US monetary regulators to develop entry to crypto and personal firms in 401(ok) plans.

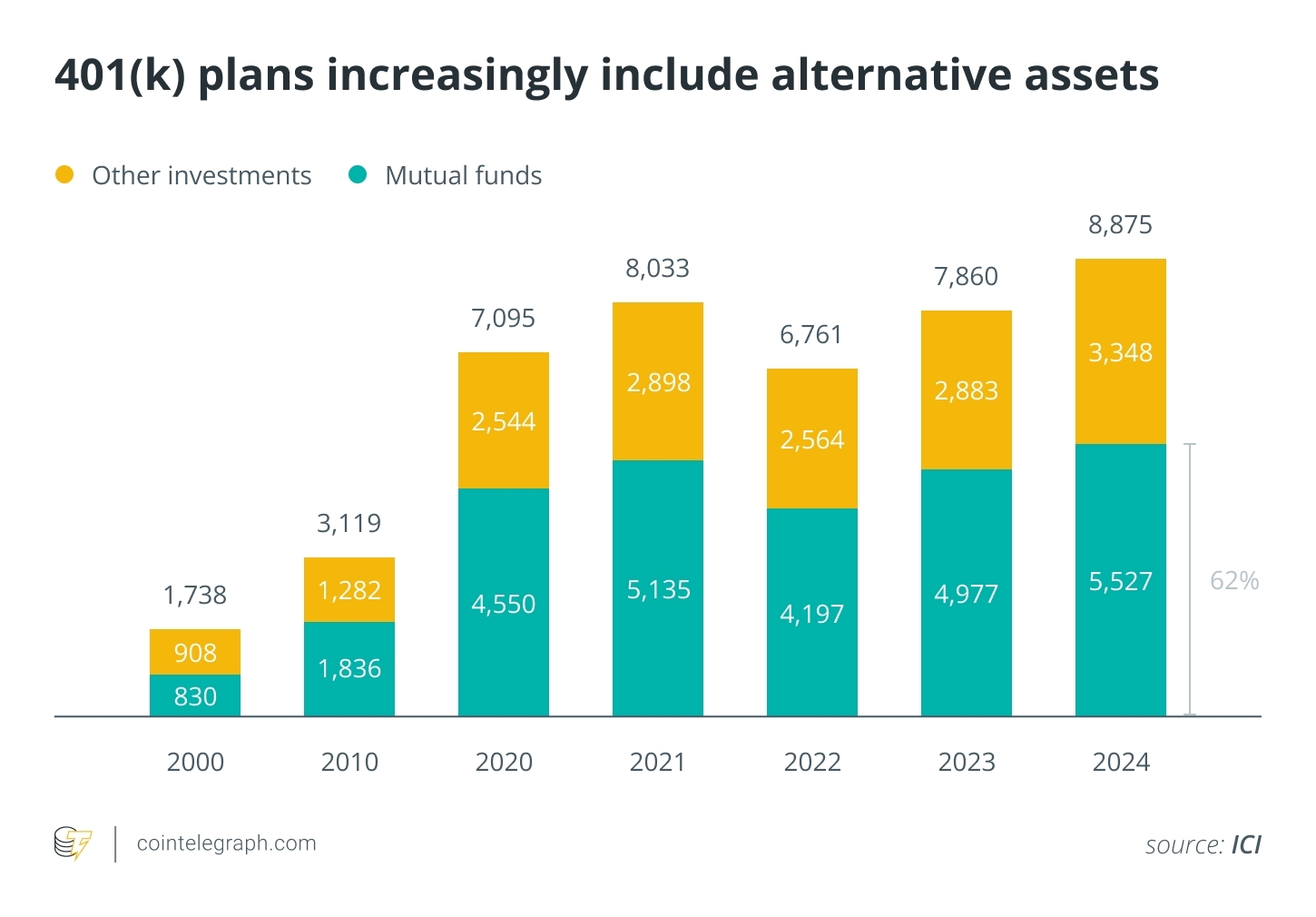

The 401(ok) employee-sponsored funding scheme is among the hottest retirement plans within the US. As of 2024, 401(ok) plans held $8.9 trillion in belongings. As such, it could characterize an enormous supply of demand for cryptocurrencies and will ship costs skyrocketing.

Crypto merchants might even see the transfer as a bullish sign for additional worth spikes, however monetary professionals and market observers say there are important dangers.

What dangers does Bitcoin pose for 401(ok) traders?

Trump’s order opens up avenues of funding that have been beforehand locked out of America’s hottest retirement plan, directing the US Labor Division to reevaluate restrictions on six totally different asset teams:

-

Personal fairness

-

Actual property (together with debt devices secured by actual property)

-

Crypto funding merchandise which might be actively managed

-

Commodities

-

Initiatives financing infrastructure improvement

-

Longevity risk-sharing swimming pools.

Trade observers have claimed that extra capital coming into crypto markets will drive crypto costs upward. André Dragosch, head of European analysis at crypto asset supervisor Bitwise, advised Cointelegraph in a “Chain Response” present on X that this might see Bitcoin’s worth move $200,000 by the tip of the 12 months.

Is Bitcoin Headed for a 2025 Peak? Or is the 4-12 months Cycle Useless? https://t.co/DckFjvkJIx

— Cointelegraph (@Cointelegraph) August 18, 2025

CJ Burnett, chief income officer of Compass Mining, advised Cointelegraph, “Elevated adoption of Bitcoin in 401(ok)s unlocks a big pool of capital and passive funding flows that drive stability and scale back volatility of the asset.”

A 401(ok) is an employer-sponsored retirement financial savings plan within the US that enables staff to contribute a part of their revenue, usually matched partly by an employer, to be invested in varied funds. 401(ok)s are sometimes tax-deferred or tax-advantaged.

401(ok)s could also be good for crypto, however monetary professionals aren’t as sure whether or not crypto can be good for 401(ok)s.

One difficulty that involved observers was the excessive charges related to a few of these various investments. In accordance with the Funding Firm Institute (ICI), most 401(ok) plan belongings have charges averaging simply 0.26%, whereas personal fairness usually makes use of a “2 and 20” construction, whereby managers accumulate a 2% total charge and 20% of any returns.

Philitsa Hanson, head of product, fairness and fund administration at Allvue Programs, mentioned, “I don’t suppose individuals are speaking sufficient in regards to the potential for larger charges.”

The chief order “raises extra questions than solutions,” Hanson continued. “Somebody will must be very considerate about how a lot of these belongings might be included.”

Bitcoin (BTC) exchange-traded funds (ETFs) usually get pleasure from charges akin to the ICI common, though some main outliers, similar to ProShares Bitcoin Technique ETF, Valkyrie Bitcoin and Ether Technique ETF and Grayscale Bitcoin Belief ETF, have charges of 0.95%, 1.24% and 1.50%, respectively. Charges additionally don’t embrace different features affecting profitability, like liquidity and buying and selling prices.

Associated: Michigan pension fund deepens Bitcoin publicity with $11M stake in ARK ETF

Ary Rosenbaum of the Rosenbaum regulation agency wrote that Bitcoin is way too risky to be included in a 401(ok): “When Bitcoin drops 40% in every week — and it’ll — plaintiffs’ attorneys will come knocking. ‘Why did you supply such a dangerous asset?’ ‘What due diligence did you carry out?’ ‘The place was the chance disclosure?’”

He referred to as crypto a “fiduciary minefield.” It accommodates complicated mechanisms like staking, forks and air drops and has complicated tax remedy. “Out of the blue you’ve constructed a participant training nightmare.”

Margaret Rosenfeld, chief authorized officer of staking supplier Everstake, advised Cointelegraph, “The largest dangers are acquainted ones for any investments: market volatility, cybersecurity, and fiduciary publicity.”

“That mentioned, these dangers aren’t insurmountable.”

401(ok) plans want “plumbing improve”

Rosenfeld mentioned that updates to laws and steering round 401(ok)s may alleviate lots of the related dangers. Firstly, she recommended creating a transparent commonplace for what could possibly be thought-about a “prudent” digital asset.

She mentioned that the Worker Retirement Revenue Safety Act of 1974, which regulates what must be included in retirement plans, “was constructed for shares and bonds, not blockchains.”

Rosenfeld really useful an “improve to the retirement system’s plumbing,” stating, “The recordkeeping programs that energy 401(ok)s aren’t designed for forks, airdrops or real-time volatility. We’d like digital asset-ready platforms that observe each onchain occasion routinely.”

She additionally mentioned that regulators ought to outline benchmarks for liquidity, clear pricing, custody and cybersecurity to make sure that sure digital belongings are “retirement-ready,” together with impartial threat rankings.

“Managed correctly, crypto in 401(ok)s may diversify retirement portfolios and convey higher transparency to an area that has usually operated outdoors institutional oversight,” Rosenfeld mentioned.

However a lot is contingent on crypto being managed correctly. Rosenbaum wrote that crypto generally is a priceless addition to a retirement portfolio, because it offers diversification, a hedge towards inflation and “publicity to monetary innovation.” Nonetheless, it doesn’t belong in a 401(ok).

“Use a brokerage account. Use a Roth IRA with a self-directed choice. Use your discretionary revenue. However don’t use the plan designed to be the monetary lifeline for somebody’s retirement,” he mentioned.

Rosenbaum wrote that, as issues stand, crypto just isn’t a viable asset for 401(ok)s. “It’s a shiny object, and chasing it places contributors — and sponsors — at pointless threat. A conservative 1%–5% allocation doesn’t repair the elemental difficulty: volatility and complexity don’t combine with retirement plans.”

The Trump administration’s transfer to loosen necessities on 401(ok)s repeats a sample in latest lawmaking whereby person safety and systemic dangers take a again seat to spice up crypto adoption and the digital asset trade. The combination of crypto into the normal monetary system hasn’t been stress-tested, and the outcomes are unpredictable.

Journal: Can privateness survive in US crypto coverage after Roman Storm’s conviction?

This text doesn’t comprise funding recommendation or suggestions. Each funding and buying and selling transfer entails threat, and readers ought to conduct their very own analysis when making a choice.