2026-03-17 01:48:00

The Bank of Canada (BOC) is still widely expected to keep rates on hold for the time being, but markets are eager to see how the policy outlook changed with the ongoing US-Iran conflict.

Will central bankers adjust their inflation assessment? Or will they express optimism that Canada can weather the oil crisis?

Here’s what to look out for in this top-tier event.

Event in Focus:

Bank of Canada (BOC) Monetary Policy Statement

When Will it Be Released:

March 18, 2026 (Wednesday): 2:45 pm GMT

- BOC press conference to follow at 3:30 pm GMT

Use our Forex Market Hours tool to convert GMT to your local time zone.

Expectations:

- The BOC is expected to keep interest rates steady at 2.25%

Forecast as of March 16, at 3:32 am GMT

Previous Releases and Risk Environment Influence on CAD

January 28, 2026

Action/results:

The BOC kept rates on hold at 2.25% as expected in their January decision, with BOC Governor Macklem keeping the door open for potential easing should economic conditions warrant it. Policymakers assessed the current stance as appropriate and that the outlook for growth and inflation remained broadly in line with projections.

Although the actual announcement sparked some weakness for the Canadian dollar, the commodity-related currency was able to brush this off quickly.

Risk environment and Intermarket behaviors:

Tariffs-related troubles put the Loonie on shaky ground early in the week, with additional downside stemming from Trump’s fresh threats of 100% levies on Canadian goods. Still, the energy-related currency was able to benefit from a jump in crude oil prices stemming from escalating US-Iran tensions later on.

December 10, 2025

Action/results:

As expected, the BOC kept interest rates on hold at 2.25% in their December decision, but Governor Macklem noted that rates are at the “lower end of the neutral range” and refrained from ruling out further easing.

This sparked a steady decline for the Loonie, except against the dollar weighed down by the Fed decision later on, which lasted against most of its counterparts for the next couple of trading sessions.

Risk environment and Intermarket behaviors:

The oil-related Canadian dollar was already on wobbly ground early in the week, as weaker crude oil prices and cautious positioning ahead of the BOC decision came in play.

A couple of downbeat U.S. data points reinforced the dovish Fed statement later in the week, spurring some risk-on flows that briefly lifted the Loonie, along with a net bullish lean for energy commodities.

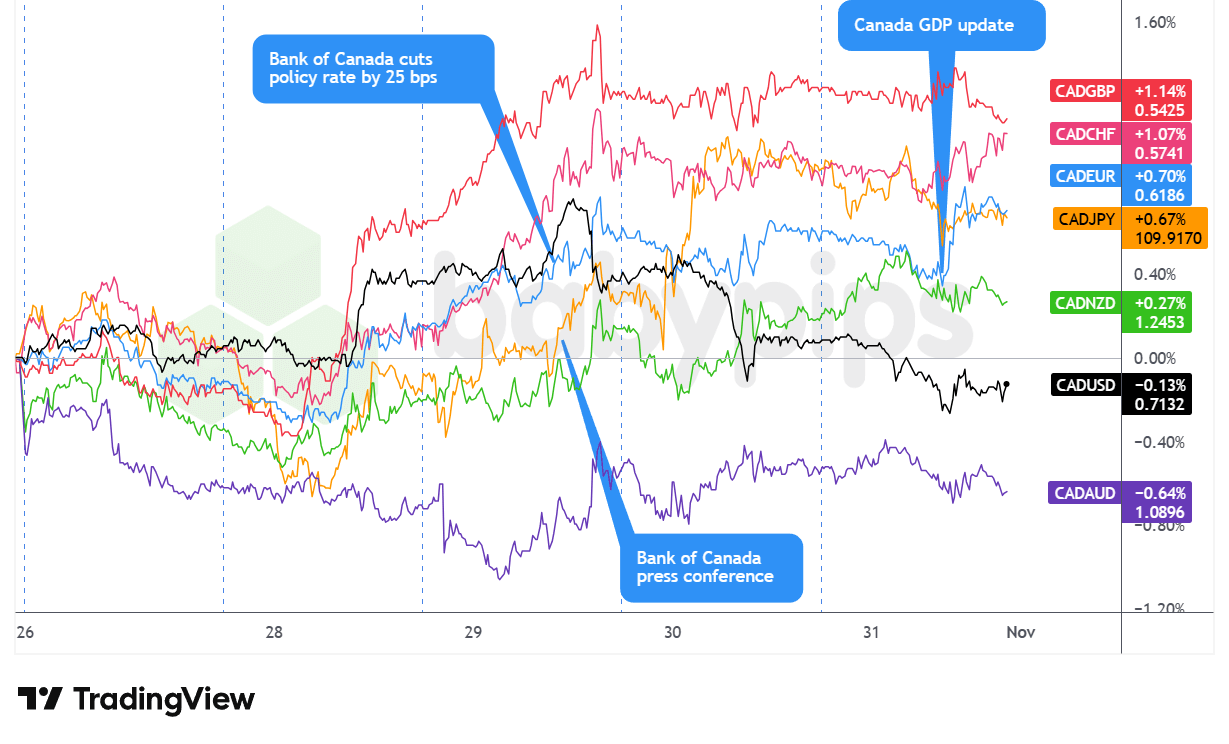

October 29, 2025

Overlay of CAD vs. Major Currencies Chart by TradingView

Action/results:

The BOC cut its interest rates by 25bps to 2.25% as expected, but surprised markets by signaling the easing cycle may be over. BOC Gov. Macklem shared that further cuts would require “a materially altered economic outlook,” as the opposing effects of tariffs on demand and costs largely balance out.

The Canadian dollar, which turned lower shortly after the U.S. session opened, jumped after the BOC announcement as traders viewed the statement that rates are “about the right level” as a hawkish signal.

But by the London close and mid-U.S. trading, focus shifted to the FOMC policy event. The Loonie’s rally quickly faded after the Fed decision, as Powell’s comment that a December rate cut was “not a foregone conclusion” lifted the U.S. dollar. Despite a moderation of gains into the close, CAD capped the day higher against its major counterparts.

Risk environment and Intermarket behaviors:

Central banks dominated the day’s market themes as the Fed delivered an expected rate cut while simultaneously clouding the outlook for December, triggering sharp reversals across asset classes and sending a clear message that policy is “not on a preset course.”

Stocks reversed lower, gold sank, Bitcoin slid, and Treasury yields ripped higher, signaling a clear shift into defensive positioning even though oil held up on inventory data.

Promotion: Tired of “demo-only” prop firms? Lux Trading Firm funds you with real capital and refunds your evaluation fee 100% after Stage 1. Trade Forex, Indices, and Commodities with a 6% fixed drawdown.

Relevant Canadian Data Since the Last BOC Statement:

-

Canada Employment Change for February 2026: -83.9k (-15.0k forecast; -24.8k previous)

- Canada Unemployment Rate for February 2026: 6.7% (6.7% forecast; 6.5% previous)

- Canada Average Hourly Wages for February 2026: 4.2% y/y (3.2% y/y forecast; 3.3% y/y previous)

- Canada Balance of Trade for January 2026: -3.65B (-0.9B forecast; -1.31B previous)

- Canada Building Permits for January 2026: 4.8% m/m (2.1% m/m forecast; 6.8% m/m previous)

- Canada S&P Global Manufacturing PMI for February 2026: 51.0 (50.7 forecast; 50.4 previous)

- Canada S&P Global Services PMI for February 2026: 46.5 (46.0 forecast; 45.8 previous)

- Canada Ivey PMI for February 2026: 56.6 (50.5 forecast; 50.9 previous)

- Canada GDP Growth Rate for December 31, 2025: -0.2% q/q (-0.1% q/q forecast; 0.6% q/q previous); -0.6% y/y (0.0% y/y forecast; 2.6% y/y previous)

- Canada CPI Growth Rate for January 2026: 0.0% m/m (0.2% m/m forecast; -0.2% m/m previous); 2.3% y/y (2.5% y/y forecast; 2.4% y/y previous)

- Canada BoC Market Participants Survey: The survey shows market participants expect a soft Canadian growth backdrop, inflation close to target, and a very steady BoC policy rate through 2026, with liftoff pushed into 2027.

Price action probabilities

Risk Sentiment Probabilities

Traders seemed to wake up on the right side of the bed this week, starting Monday off strong with a risk rally as the focus turned to diplomatic efforts to address the Strait of Hormuz situation. Still, as previous weeks have proven, sentiment could shift on a dime and reports of escalating tensions could trigger another flight to safety.

Another major event that could steal the show is the FOMC decision midweek, as the announcement comes up with updated economic projections and the Fed’s dot plot of interest rates. Pay attention to evolving central bank narratives (including that of the RBA, BOJ, ECB and SNB) influenced by the US-Iran war and the oil crisis.

Potential CAD Scenarios

Top-tier economic reports from Canada haven’t been so impressive lately, as employment, inflation, trade activity and growth have fallen short of expectations. However, it’s also important to note that these are backwards-looking data and that the surge in crude oil prices may have changed the economic picture.

Although the BOC is likely to sit on its hands for the time being, traders will be paying extra close attention to changes in rhetoric and forward guidance in the official statement and press conference. In this scenario, look out for a muted reaction to the actual rate announcement as Loonie traders read between the lines of their decision and brace for Governor Macklem’s remarks.

Should policymakers downplay the impact of higher crude oil prices on overall inflation and instead focus on sluggish domestic growth and external risks stemming from tariffs uncertainty, there could be a case for mild Loonie weakness.

AUD/CAD and NZD/CAD could be poised to recover, especially if the RBA sticks to its hawkish bias or if risk-on flows are extended, while CAD/JPY or CAD/CHF could see some downside in a risk-off scenario. Still, keep in mind that yen or franc gains could be limited since the BOJ and SNB decisions are lined up on Thursday.

Meanwhile, a more optimistic tone during the BOC announcement and presser could translate to another leg higher for the Loonie. In this case, the Canadian currency could be better-positioned to take advantage of weakness among European currencies which appear more vulnerable to the Middle East conflict.

EUR/CAD or GBP/CAD could see a breakdown from their current consolidation while CAD/CHF could gain further traction on its climb, particularly if the SNB repeats its jawboning. USD/CAD could also turn lower, though the U.S. dollar is prone to additional volatility during the FOMC event later in the session.

Whichever bias you end up trading, remember to prepare for increased intraday volatility. Consider waiting for the actual announcement to unfold (including the press conference) to see how the market digests the news.

Make sure to factor all this into your trade and risk management plan in a way that suits your trading strategy and market outlook!

Disclaimer: The Event Guide is provided for educational and informational purposes only. It is not intended as investment or trading advice, nor should it be interpreted as a recommendation to take any position in the market. The goal of this content is to help readers become aware of recent economic developments that may influence market behavior. These insights are designed to support the development of each trader’s own scenarios and directional biases, which may require further analysis and due diligence before acting upon.

All trading decisions—including entry, exit, risk management, and position sizing—are entirely the responsibility of the individual trader. The scenarios and interpretations discussed may not be suitable for all trading strategies, risk profiles, or portfolio objectives. Past market behavior does not guarantee future results. Please trade responsibly and at your own risk.

BabyPips Premium Annual Members have exclusive access to our highest-tier partnership deal: 30% off your first year of TradeZella annual subscription ($120 savings)! If you’re SERIOUS about mastering your performance and psychology, TradeZella’s AI-powered journaling and backtesting tools are the industry gold standard.

This discount effectively covers the entire cost of an annual BabyPips Premium subscription—and then some!

To Claim the Exclusive 30% off, email us at [email protected] to verify membership status and receive the promo code. Please reference “TradeZella Annual Plan Promo Code” in your email subject line.

{kind=link}