Nasdaq’s latest tokenization push is another attempt to bring stocks onto blockchain rails. Yet the real significance lies more in the structure.

Rather than endorsing the offshore model of stock wrappers and synthetic equity exposure, Nasdaq is trying to build a version where the token is the share. As a result, the token shares the same legal status, a direct link to the issuer’s ownership record, and a path to voting, governance, and corporate actions.

That makes this less a crypto-adoption story than a control story. If tokenized equities are going to scale, someone will decide whether investors own a legally equivalent on-chain share or just a programmable claim that behaves like one.

Nasdaq’s design suggests Wall Street does not want to leave that decision to offshore wrappers or third-party token issuers.

The SEC just drew the battle lines

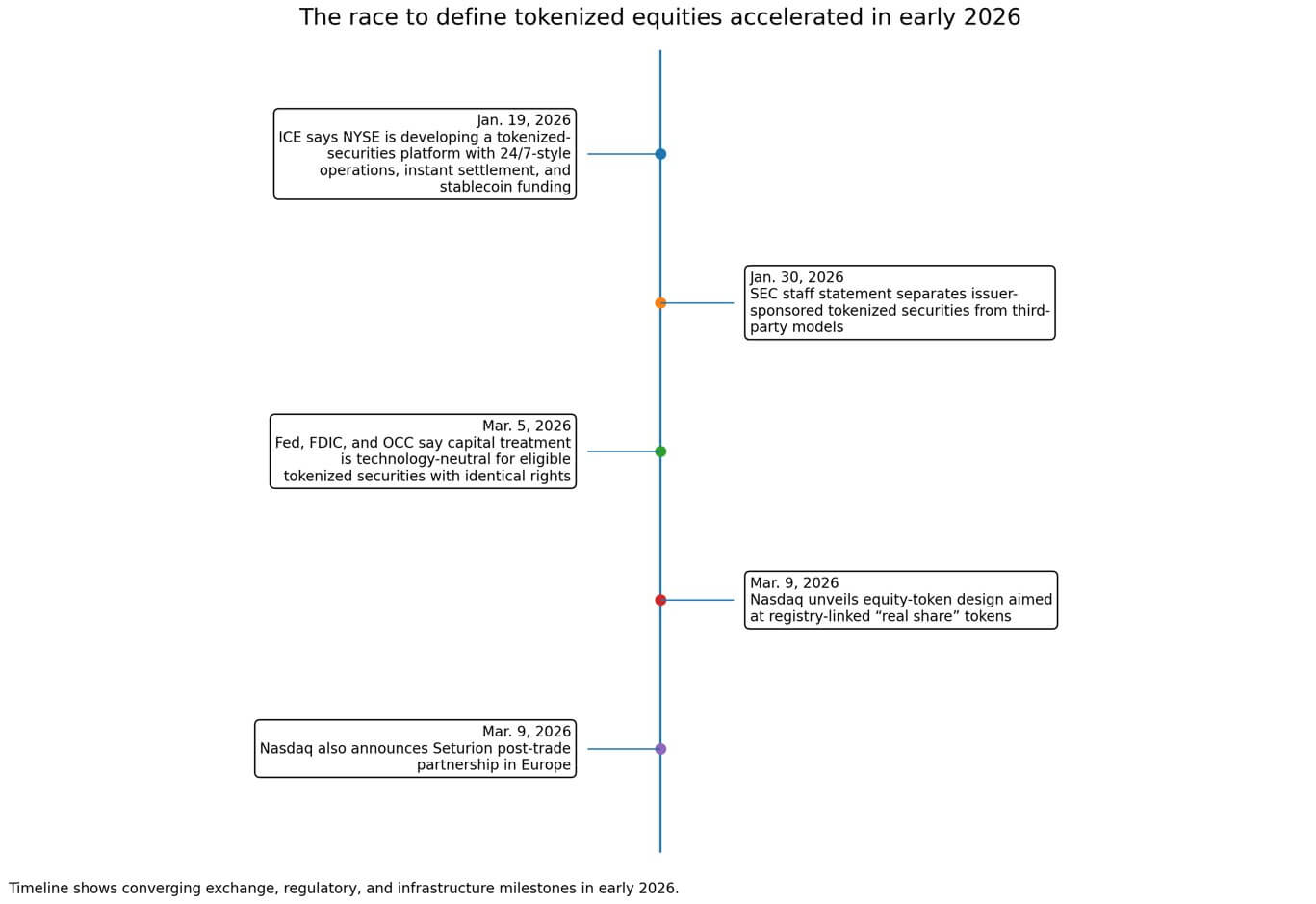

On Jan. 30, the SEC’s staff issued a statement explicitly separating issuer-sponsored tokenized securities from third-party models.

In the issuer-sponsored version, the issuer integrates distributed ledger technology into the master securityholder file, so transferring the token updates the actual ownership record.

In third-party models, holders may have only exposure or an indirect entitlement and may face additional risks.

Nasdaq’s Mar. 9 announcement leans into that framework. The exchange is pitching tokens tied to the official registry, with proxy actions, corporate actions, governance rights, and legal equivalence to the underlying security.

The program targets operational readiness in the first half of 2027.

Nasdaq’s 2025 rule proposal clarifies the rights question. The exchange would treat tokenized shares as equivalent to traditional shares only if they have the same CUSIP and confer the same dividends, voting rights, and claims to residual assets.

If a token lacks those rights, Nasdaq would treat it as a distinct instrument.

| Feature | Nasdaq issuer-sponsored model | Rights-light / wrapper model (example: xStocks) |

|---|---|---|

| Official ownership record | Linked to issuer’s registry / master securityholder file | Separate third-party structure |

| Legal status | Intended to be legally equivalent to the share | Exposure or indirect entitlement |

| CUSIP / same-share treatment | Same CUSIP required for equivalence | Not the same share |

| Voting rights | Intended to travel with token | No voting rights |

| Dividends | Intended to travel with token | No dividend rights |

| Residual asset claim | Preserved | No legal claim to residual assets |

| Corporate actions / proxy actions | Built into design | Limited or absent |

| Investor relationship | Issuer remains central | Intermediary or wrapper provider sits in middle |

| Main tradeoff | Stronger rights, heavier compliance | Easier distribution, weaker rights |

Crypto wrappers proved that investors will trade stock-like exposure on-chain. Nasdaq’s point is that proxy rights, corporate actions, and legal ownership should travel with the token.

What rights-light products already prove

Kraken’s xStocks provide the contrast. The platform’s FAQ states that xStocks “do not confer shareholder rights like voting or dividends,” provide “synthetic exposure” with “no legal claims” to the underlying shares or residual assets, and are restricted to non-U.S. retail clients.

Yet demand exists. Payward says xStocks have surpassed $25 billion in total transaction volume, including more than $4 billion settled on-chain, with more than 85,000 unique holders. The tokenized stocks are deployed into Solana, Ethereum, and TON infrastructures.

Nasdaq is trying to intercept that demand and redirect it into a more regulated, issuer-centered format.

The hidden battleground is whether the official ownership record stays within issuer-sponsored rails or migrates to wrappers that are easier to distribute but weaker in terms of rights.

If users are satisfied with wrappers that trade around the clock, incumbent markets risk finding that the internet has already chosen a de facto equity product.

Preserving incumbent economics while extending the stack

Nasdaq’s proposal preserves price discovery, best execution, DTC settlement, and the mechanics of a regulated exchange.

The 2025 filing describes tokenized securities trading on the same order book as traditional securities and settling through DTC infrastructure.

The proposed process would let a participant flag a trade for token settlement, after which DTC would convert the position into token form.

This extends the existing market stack while preserving the things incumbents monetize: liquidity, clearing, settlement, collateral, and compliance. The broader economics are likely to be driven by turnover, collateral reuse, financing, after-hours access, issuer services, and governance workflows.

Payward frames the gateway in terms of capital mobility and collateral efficiency.

The partnership is designed to enable tokenized equities to move between regulated markets and on-chain markets while preserving issuer rights and price integrity.

The opportunity is large even before mass adoption

Nasdaq is home to roughly 4,000 listings, valued at about $14 trillion. Even modest token-rail adoption would be strategically meaningful.

A simple sizing exercise: if only 0.1% of that value touches issuer-sponsored token rails, that implies roughly $14 billion of equity value, while 1% implies $140 billion.

The broader tokenization backdrop justifies a Wall Street framing.

McKinsey’s 2024 model centers on about $2 trillion in tokenized financial assets by 2030, excluding cryptocurrencies and stablecoins. That explains why exchanges, brokers, custodians, and crypto venues are now fighting over standards and distribution.

The competitive backdrop is heating up. ICE announced in January that NYSE is developing a tokenized-securities platform with operations approaching around-the-clock trading, instant settlement, and stablecoin-based funding.

Nasdaq also announced a post-trade partnership with Seturion in Europe. Legacy exchanges now compete on listings, liquidity, and the architecture of tokenized market access.

On Mar. 5, the Federal Reserve, FDIC, and OCC said the capital rule is technology-neutral and that eligible tokenized securities with identical legal rights should be treated the same as non-tokenized securities for capital purposes.

The clarification reduces one source of institutional hesitation while broader legal questions remain.

Nasdaq emphasizes that participation remains voluntary and that future enhancements will be guided by evidence and regulatory review.

The exchange plans to engage with issuers, transfer agents, regulators, and market participants as the framework evolves.

Can legal design catch distribution?

Rights-light products are the threat vector.

The deciding questions are: Can Nasdaq make the rights-preserving version easy enough that investors stop settling for wrappers? Can regulated infrastructure support the benefits people want from crypto-native products without losing the legal attributes of the share? Will issuers actually sponsor tokenized shares?

The most plausible near-term outcome is coexistence. Issuer-sponsored tokens arrive, but wrappers continue to dominate crypto-native distribution because they are simpler and already have traction.

Nasdaq creates a regulated standard for some issuers and institutions, but not a universal default.

The bull case consists of the SEC taxonomy, bank-capital neutrality, and an exchange-led infrastructure shift that moves the market toward rights-preserving tokenized equities.

Tokenized shares start to look less like crypto wrappers and more like a modernized distribution and settlement layer for ordinary listed equities.

In the bear case, rights-light stock tokens continue to grow faster because they are globally accessible, wallet-native, and already integrated into crypto trading flows. Nasdaq’s model proves legally cleaner but operationally heavier, and the market splits between “real shares” for institutions and “good-enough wrappers” for everyone else.

A major failure in a wrapper-based product, or a visible dispute over voting or liquidation rights, could abruptly increase the value of issuer-sponsored models.

The reverse is also possible: if exchange-led systems prove too slow or too closed, markets may decide that legal perfection matters less than access.

Nasdaq’s proposal preserves the same market architecture while making equity rights programmable rather than optional.

The real economic prize is likely control over clearing, collateral mobility, issuer services, governance workflows, and cross-network interoperability.

Wall Street is racing to make the real share programmable before offshore wrappers become good enough to replace it. Nasdaq is trying to make sure that, when equities become internet-native, the token that wins is the actual share.