Markets whipsawed through a dramatic Monday session as oil prices first surged above $100 per barrel on escalating Middle East conflict fears before crashing more than 20% after President Trump signaled the Iran war could conclude sooner than expected. The wild intraday reversal sent equities from deep losses to modest gains while the U.S. dollar traded mixed against major currencies despite sustained safe-haven demand throughout Asian and early European hours.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- China CPI Growth Rate for February 2026: 1.0% m/m (0.3% m/m forecast; 0.2% m/m previous); 1.3% y/y (0.7% y/y forecast; 0.2% y/y previous)

- China PPI for February 2026: -0.9% y/y (-1.2% y/y forecast; -1.4% y/y previous)

- Japan Leading Economic Index Prel for January 2026: 112.4 (113.0 forecast; 111.0 previous)

- Japan Eco Watchers Survey Outlook for February 2026: 50.0 (50.4 forecast; 50.1 previous)

- Japan Eco Watchers Survey Current for February 2026: 48.9 (48.0 forecast; 47.6 previous)

- Germany Factory Orders for January 2026: -11.1% m/m (-4.3% m/m forecast; 7.8% m/m previous)

- Germany Industrial Production for January 2026: -0.5% m/m (1.2% m/m forecast; -1.9% m/m previous)

- Swiss Consumer Confidence for February 2026: -30.0 (-30.0 forecast; -30.0 previous)

- U.S. Consumer Inflation Expectations for February 2026: 3.0% (3.1% forecast; 3.1% previous)

- Iran named Mojtaba Khamenei, the hardline son of the assassinated Ayatollah Ali Khamenei, as its new supreme leader on Monday, signaling Tehran’s determination to continue the conflict. The appointment came as Israel struck Iranian oil storage facilities over the weekend, triggering massive fires across Tehran and further choking global energy supplies through the Strait of Hormuz.

- President Trump posted on social media that $100 crude was “a very small price to pay” for safety and peace, while later telling CBS the conflict is “very complete, pretty much” and noted it’s “very far” ahead of his four to five week timeline. The conflicting messages contributed to extreme volatility across asset classes.

- Group of Seven finance ministers said they were ready to take steps to support energy supply, including releasing strategic oil reserves, though the group stopped short of committing to immediate action.

Promotion: Use TradeZella’s AI Powered trade journal to deep-dive into your execution and see exactly how you performed during today’s trading session.

Click here to get the TradeZella Edge and use code PIPS20 to save 20% on your first purchase!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

Monday delivered one of the most volatile trading sessions in recent years as markets lurched between stagflation fears and relief rallies following rapidly shifting war developments and presidential commentary.

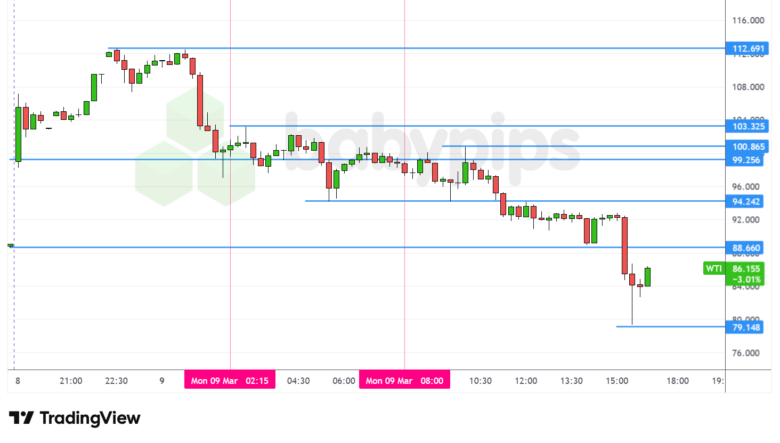

WTI crude oil experienced historic intraday swings, initially surging to approximately $112.69 per barrel during Asian trading hours as reports confirmed the effective closure of the Strait of Hormuz and strikes on energy infrastructure across the Persian Gulf. The spike marked oil’s highest level since Russia’s 2022 invasion of Ukraine and reflected fears that roughly 20% of global oil supply could remain offline for an extended period. However, crude reversed violently following Trump’s CBS interview comments suggesting the war could end soon, combined with G7 discussions about coordinated strategic reserve releases. Oil ultimately closed near $86 per barrel (rebounding after touching $80), down approximately 1% on the day despite the dramatic intraday journey. The $30 per barrel intraday range from peak to trough represented one of the largest single-day swings on record. Check out the chart below!

WTI Crude Oil – Chart Faster With TradingView

The S&P 500 mirrored oil’s volatility pattern, initially plunging more than 1.5% during overnight futures trading on stagflation concerns as surging energy costs threatened to rekindle inflation while simultaneously damaging economic growth. Asian equity markets suffered severe losses, with Japan’s Nikkei 225 tumbling over 5% and South Korea’s KOSPI dropping nearly 6% as investors in major oil-importing nations priced in the economic damage from sustained triple-digit crude prices. However, U.S. stocks staged a remarkable reversal following Trump’s war timeline comments, with the S&P 500 ultimately climbing approximately 0.8% to close around 6,784. The index erased an intraday loss of more than 1.5% for the first time since April, with technology shares leading the advance as traders bet that a swift war resolution would prevent the sustained inflation shock that could force the Federal Reserve to maintain restrictive policy longer than anticipated.

Gold declined 0.5% to settle near $5,147 per ounce despite the geopolitical chaos that would typically support safe-haven demand. The precious metal’s weakness likely reflected the massive intraday rally in the dollar during Asian hours, which made gold more expensive for international buyers, combined with profit-taking after recent gains. Gold traded in a relatively tight range throughout most of the session, suggesting investors remained uncertain whether the war developments warranted additional safe-haven positioning or whether Trump’s optimistic timeline commentary justified reducing hedges.

Bitcoin rallied 1.1% to trade around $69,002, extending recent gains as the cryptocurrency continued to trade as a risk asset rather than following its occasional safe-haven behavior. With no notable crypto focused news to point to, the advance tracked the recovery in sentiment after Trump’s timeline commentary and hints that the G-7 were ready to take steps to support energy supply.

Treasury yields declined sharply, with the 10-year yield falling approximately 0.9% to close around 4.10%. The bond market rally accelerated during U.S. trading hours, likely correlating with Trump’s comments suggesting a faster war resolution than previously feared. Lower yields reflected reduced stagflation concerns, as a quicker war conclusion would limit the duration of the energy price shock and reduce the risk that the Federal Reserve would need to choose between fighting inflation and supporting growth. The yield decline came despite rising breakeven inflation rates earlier in the session, suggesting traders shifted focus to growth risks and the possibility of Fed rate cuts if the oil shock proves temporary.

Promoted: Capitalize on News Catalysts Without Risking Your Own Funds.

In a geopolitical shock regime, the S&P 500 can swing 200+ points intraday. Why risk your personal capital during extreme volatility?

Most proprietary firms terminate your evaluation account if you execute a trade during a major macroeconomic release, but FundedNext permits news trading across all models. Test your thesis with up to $300,000 in simulated capital, or take advantage of their Free Trial to experience the platform risk-free.

Explore FundedNext and Start Your Free Trial!

Disclosure: We may earn a commission from our partners if you sign up through our links.

FX Market Behavior: U.S. Dollar vs. Majors

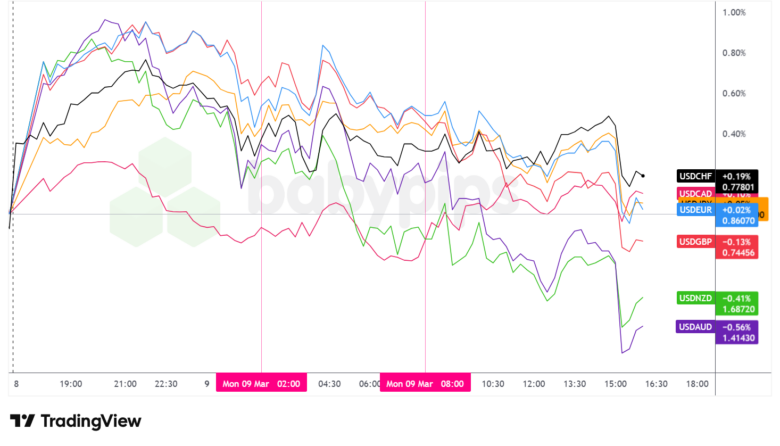

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar experienced choppy and directionally unstable trading throughout Monday’s volatile session, ultimately closing mixed against major currencies with an arguably neutral to slightly bearish lean despite intense safe-haven flows during Asian hours.

During the Asian session, the dollar rallied higher until mid-morning as traders sought safety amid the oil price surge and reports of Iran’s new hardline supreme leader. The greenback’s strength likely reflected positioning adjustments as investors anticipated a prolonged energy crisis that could benefit the U.S. economy relative to major oil-importing nations like Japan and European countries. However, the dollar pulled back heading into the London open, possibly as traders digested the initial shock and began questioning whether the energy disruption would persist long enough to meaningfully alter central bank policy trajectories.

The London session brought continued dollar weakness from its intraday high going into the U.S. session open. European data disappointed significantly, with Germany’s factory orders plunging 11.1% and industrial production missing forecasts, yet the euro and other European currencies held relatively steady against the dollar. This resilience likely reflected market positioning that focused on the oil shock’s greater impact on oil-importing Asian economies rather than on eurozone growth concerns, combined with speculation that G7 coordination on strategic reserve releases could stabilize energy markets.

After the U.S. session opened, the dollar continued to trend lower on net against the major currencies, with a pronounced spike lower ahead of the daily close. This afternoon weakness accelerated following Trump’s CBS interview comments suggesting the war is “pretty much” complete and ahead of his initial timeline. The dovish implications for oil prices and stagflation risks appeared to reduce safe-haven dollar demand more than concerns about U.S. economic impact from higher energy costs.

At Monday’s close, the dollar posted mixed results across the major currency pairs but with an arguably slightly bearish lean overall. The greenback’s losses against the Australian dollar, New Zealand dollar, and British pound significantly exceeded its modest gains against the Canadian dollar, euro, Japanese yen, and Swiss franc. The pattern suggested commodity-linked and growth-sensitive currencies outperformed as traders positioned for potential war de-escalation, while traditional safe havens like the yen and franc lagged despite the day’s geopolitical turmoil.

Promoted: Protecting your trading capital starts with securing your access. Don’t let a weak password be the single point of failure for your brokerage or exchange accounts. LastPass simplifies your digital life by generating and storing complex, encrypted passwords for every site you use. Secure Your Accounts with LastPass Today!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Upcoming Potential Catalysts on the Economic Calendar

- Australia Westpac Consumer Confidence Change for March 2026 at 11:30 pm GMT

- Japan Average Cash Earnings for January 2026 at 11:30 pm GMT

- Japan Household Spending for January 2026 at 11:30 pm GMT

- Japan GDP & Price Index Final for December 31, 2025 at 11:50 pm GMT

- U.K. BRC Retail Sales Monitor YoY for February 2026 at 12:01 am GMT

- Australia Building Permits Final for January 2026 at 12:30 am GMT

- Australia NAB Business Confidence for February 2026 at 12:30 am GMT

- China Balance of Trade for February 28, 2026 at 3:00 am GMT

- Japan Machine Tool Orders for February 2026 at 6:00 am GMT

- Germany Balance of Trade for January 2026 at 7:00 am GMT

- U.S. NFIB Business Optimism Index for February 2026 at 10:00 am GMT

- U.S. ADP Employment Change Weekly for February 21, 2026 at 12:15 pm GMT

- U.S. Existing Home Sales for February 2026 at 2:00 pm GMT

Tuesday’s calendar features China’s trade balance data, which could provide insight into how the world’s second-largest economy is navigating both domestic recovery efforts and the evolving energy crisis. Japan’s wage and spending data will be closely watched for signs of sustained inflation pressure that might support further Bank of Japan policy normalization, particularly given the yen’s recent weakness.

The U.S. session brings the weekly ADP employment report and existing home sales data, though traders will likely remain focused on geopolitical headlines and oil price movements as primary drivers of market direction. Any additional commentary from President Trump about war timelines or from Iranian leadership about retaliation plans could spark renewed volatility across all asset classes.

Markets remain highly sensitive to developments in the Middle East, with participants closely monitoring tanker traffic through the Strait of Hormuz and any signs that energy infrastructure strikes might escalate or de-escalate. The extreme intraday price swings on Monday underscore the difficulty of positioning in an environment where presidential social media posts and war developments can instantly reverse multi-billion dollar market moves.

Stay frosty out there, forex friends!

Promoted: The Strategy is Half the Battle; Your Mindset is the Rest.

In “Unknown Market Wizards (4.6⭐| 1.4K+ reviews on Amazon),” Jack Schwager interviews successful traders to reveal a common truth: their edge isn’t just knowledge or skills—it’s their psychological resilience and rigid risk control. Whether you’re navigating the 15% tariff shock or Nvidia’s earnings, learn how the “wizards” stay clinical when the rest of the market is emotional.

Learn more about “Unknown Market Wizards” on Amazon!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.