Bitcoin volatility could explode in April as SEC reviews the market behind ETF leverage

On Apr. 16, the Securities and Exchange Commission will host a public roundtable on listed options market structure covering quote-driven competition, customer experience, and growth.

This is standard regulatory fare, except that Bitcoin exposure is migrating into regulated, centrally cleared products just as the SEC is reconsidering how the machinery works.

Small changes to spreads, routing, and quoting can alter leverage costs, and when leverage gets cheaper, volatility patterns change.

The Mar. 5 announcement gives markets 42 days to prepare for the discussion going live.

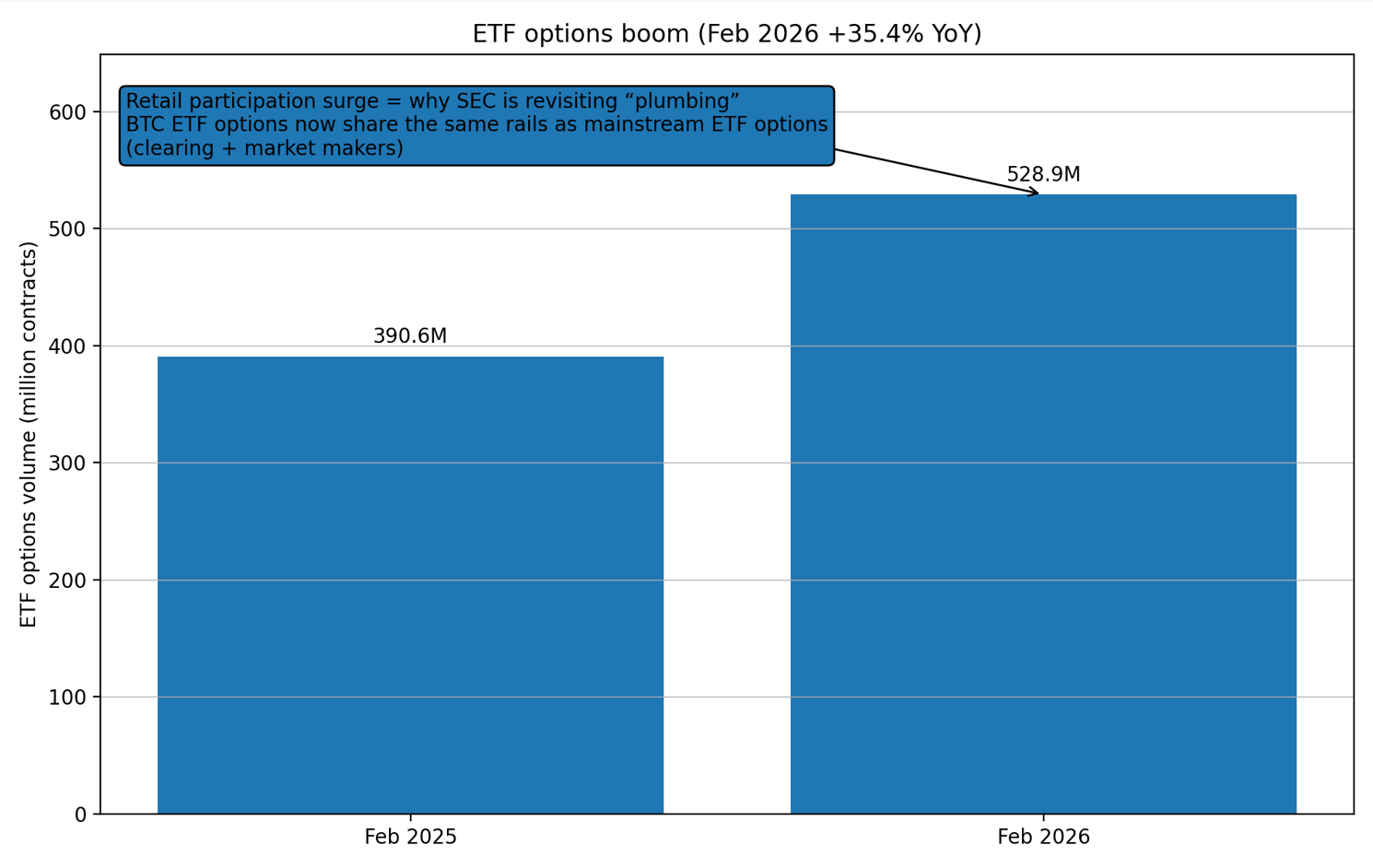

Commissioner Hester Peirce framed it as celebrating achievement while inviting “further reflection,” signaling that the SEC recognizes that retail options participation has exploded. What she didn’t mention: Bitcoin ETF options now sit inside that infrastructure, using the same clearing and market-maker networks as traditional equity derivatives.

The numbers that make this matter

IBIT holds $56.8 billion across 1.36 billion shares, trading roughly 86 million shares daily, with a median spread of 0.03%. Options began trading on Nov. 19, 2024. Six months later, the SEC approved raising position limits from 250,000 to 1,000,000 contracts.

As of Feb. 11, 1,000,000 contracts represent 7.474% of IBIT shares outstanding. At 100 shares per contract, that’s 100 million shares, more than a full day’s volume.

Even a quarter of that limit, with a 0.40 delta, generates 10 million shares of dealer hedge demand, 12% of daily volume, enough to move markets during fast action or around expiration.

IBIT isn’t alone. Nasdaq filings cover multiple Bitcoin and Ethereum ETFs. Cboe offers cash-settled Bitcoin ETF index options. The Options Clearing Corporation now clears crypto-linked products using mainstream infrastructure.

February 2026 ETF options volume hit 528.9 million contracts, up 35.4% year-over-year.

Why market structure reforms leak into volatility

The roundtable examines quote-driven competition, customer experience, and growth. These themes directly translate into execution quality.

Listed options operate as quote-driven markets, with market makers dominating liquidity. Small rule changes around quoting obligations, tick sizes, or auctions can significantly alter transaction costs.

If the SEC leans pro-competition, tightening spreads and improving price discovery, IBIT options get cheaper to trade. Cheaper options attract participants. More participants generate open interest. More open interest requires dealer hedging.

Dealer hedging in ETF shares translates into creation and redemption activity that touches Bitcoin spot through authorized participant flows.

The mechanism is mechanical. Market makers hedge options by trading underlying shares. For IBIT, that means ETF shares. Significant share quantities trigger either secondary-market trades or creation/redemption with authorized participants.

BlackRock’s structure uses Bitcoin to create IBIT shares, establishing the direct link between listed options hedging and spot markets.

This matters most around expiration and sharp moves.

As Bitcoin approaches strikes with heavy open interest, gamma accelerates. Delta changes quickly, forcing rapid hedge adjustments. If 250,000 contracts sit at a strike and price gravitates there into expiration, dealers managing that exposure pull significant ETF volume feeding back into Bitcoin.

The cryptocurrency industry is developing equity-derivatives-style reflexivity, with pinning behavior, expiration effects, and volatility surface dynamics that traditional traders recognize.

Three scenarios for Bitcoin price

Changes to options could create three potential scenarios for Bitcoin.

The first scenario consists of pro-competition reforms: the SEC emphasizes quote competition, price improvement, and transparency. IBIT spreads tighten.

Volume and open interest rise. Bitcoin shows consistent calendar effects, with monthly expiries matter, implied vol repricing drives spot, and large strikes act as magnets. If reforms reduce spreads by 20-30%, hedging flows could routinely hit 10-15% of daily ETF volume during key periods.

The second scenario presents guardrails first. The SEC tilts toward retail protection, offering enhanced disclosures, stricter suitability requirements, and friction that slows aggressive behavior.

Growth continues but slowly. Leverage costs stay elevated. Bitcoin remains driven by macro liquidity rather than listed options flow.

Lastly, a scenario of structural evolution comes to life. Even without dramatic policy shifts, the category continues to expand. Multiple ETF underlyings gain listings. Cash-settled index products deepen. Central clearing brings institutions that have avoided offshore venues.

Bitcoin gradually exhibits equity-like behavior, with basis trading across spot/ETF/, and options, volatility-surface arbitrage, and systematic strategies treating Bitcoin as a high-beta tech with listed leverage.

Bitcoin isn’t isolated from traditional finance, it’s embedded in it. Microstructure improvements accelerate that by lowering barriers for traditional participants.

| Scenario | SEC emphasis (plain English) | What changes in options trading (spreads/routing/quotes) | What happens in IBIT options (volume/OI/spreads) | BTC market behavior you’d expect | What to watch (post–Apr 16) |

|---|---|---|---|---|---|

| Pro-competition reforms | “Make the market more competitive and cheaper to trade” (tighter quotes, better fills) | More competitive quoting; stronger price-improvement/auction outcomes; lower friction in execution quality | Spreads tighten, volume + open interest rise, more strikes/expiries trade actively; deeper screens | More consistent options-calendar effects: sharper moves into expiries, more “magnet” behavior around big strikes, faster IV repricing leaking into spot | IBIT options bid/ask spreads; OI growth rate; volume share by expiry; implied vol level + skew (calls vs puts); strike concentration near spot; “expiration-week” intraday volatility changes |

| Guardrails first | “Protect retail; slow the hottest behavior” | More emphasis on disclosures, suitability/risk controls, and potentially frictions that reduce aggressive retail-style flow; execution quality focus is secondary to protection | Growth continues but slower; spreads improve modestly (if at all); OI growth is more measured | BTC remains driven mostly by macro liquidity, with less incremental reflexivity from listed options; fewer “expiry-driven” dislocations | Changes in broker risk controls / approvals for options; IBIT options retail-heavy strike activity (lot sizes, short-dated flow); spreads and OI growth staying flat; IV skew less “call-bid” |

| Structural evolution | “No dramatic rule shift, but the ecosystem keeps scaling” | Incremental microstructure tweaks; listings broaden across underlyings; institutions participate more because rails are familiar | More BTC-linked listed products (more ETF underlyings; index options deepen); steady increases in OI and liquidity over time | BTC gradually looks more equity-derivatives-like: basis trading across spot/ETF/options, vol-surface arb becomes more visible, volatility timing shifts toward listed expiries | New listings (more ETF options series / index options depth); IBIT OI as % of ADV over time; term structure of IV (short vs long dated); ETF premium/discount to NAV around heavy options days; creation/redemption activity proxies (flows) |

What to watch starting Apr. 16

The roundtable won’t produce immediate rules.

The SEC will publish an agenda, stream discussion live, and accept comments under File Number 4-887. Real policy shifts arrive months later through formal rulemaking. But markets don’t wait to reprice expectations.

Nevertheless, it is important to track IBIT options volume, open interest, and bid-ask spreads. Growth acceleration with tightening spreads signals expectations of a favorable competitive environment.

Additionally, investors should monitor implied volatility and skew, as upside calls being aggressively bid relative to puts suggests leveraged positioning migrating into listed options.

Another metric to observe is expiration-week behavior. Do monthly expiries show different intraday volatility? Does Bitcoin gravitate toward concentrated strikes?

A comparison of IBIT premium/discount to NAV around heavy options activity must be drawn then, as hedging can temporarily push ETF pricing away from fair value, forcing creation/redemption activity that moves Bitcoin.

Bitcoin remains highly sensitive to financial conditions and monetary policy. The options market structure operates within that framework: it can amplify or dampen moves, shift the timing of volatility, and change who drives price discovery.

However, it doesn’t override the fundamental: when the Fed tightens and risk sells, Bitcoin sells too, regardless of how tight IBIT spreads are.

The plumbing to think about

Retail investors discovering options through commission-free platforms don’t concern themselves with quote competition or routing incentives.

They see prices and execute trades. But the machinery determining those prices shapes every transaction.

When the SEC reconsiders that machinery during explosive retail growth, the subtext is clear: the current structure may not scale indefinitely. Bitcoin arriving in that structure as a listed, cleared, exchange-traded product transforms the stakes.

Crypto spent years building parallel infrastructure, with its own venues, clearing, and culture. That separation is ending.

Not because Bitcoin is forced into traditional structures, but because traditional structures are adapting to Bitcoin demand. Spot ETFs were the first step. Listed options are second. Each integration creates transmission channels between crypto and traditional finance.

Apr. 16 won’t determine Bitcoin’s price or directly change rules. Yet, it marks regulators publicly acknowledging that listed options infrastructure now carries meaningful cryptocurrency exposure.

How they optimize it for competition, growth, protection, or some balance will influence how quickly Bitcoin’s volatility regime comes to resemble equity derivatives rather than pure spot crypto trading.

The plumbing is boring until you realize what’s flowing through it.