Markets digested the reverberations of escalating US-Israeli military strikes on Iran that began over the weekend, with oil surging and safe-haven flows dominating price action as traders weighed inflation risks from potential energy disruptions against manufacturing data showing persistent price pressures.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- Military conflict erupts in the Middle East this weekend after U.S. and Israel attack Iran, followed by regional attacks by Iran on U.S. bases and allies.

- Australia S&P Global Manufacturing PMI Final for February 2026: 51.0 (51.5 forecast; 52.3 previous)

- Australia TD-MI Inflation Gauge for February 2026: -0.2% m/m (0.2% m/m forecast; 0.2% m/m previous)

- Japan S&P Global Manufacturing PMI Final for February 2026: 53.0 (52.8 forecast; 51.5 previous)

- Germany Retail Sales for January 2026: -0.9% m/m (0.5% m/m forecast; 0.1% m/m previous); 1.2% y/y (1.9% y/y forecast; 1.5% y/y previous)

- U.K. Nationwide Housing Prices for February 2026: 1.0% y/y (1.1% y/y forecast; 1.0% y/y previous); 0.3% m/m (0.3% m/m forecast; 0.3% m/m previous)

- Swiss Retail Sales for January 2026: 1.1% m/m (-0.2% m/m forecast; 1.0% m/m previous); -1.1% y/y (1.8% y/y forecast; 2.9% y/y previous)

-

European Final PMI updates:

- Swiss procure.ch Manufacturing PMI for February 2026: 47.4 (46.5 forecast; 48.8 previous)

- Germany HCOB Manufacturing PMI Final for February 2026: 50.9 (50.7 forecast; 49.1 previous)

- Euro area HCOB Manufacturing PMI Final for February 2026: 50.8 (50.8 forecast; 49.5 previous)

- U.K. S&P Global Manufacturing PMI Final for February 2026: 51.7 (52.0 forecast; 51.8 previous)

- BoE Consumer Credit for January 2026: 1.81B (1.2B forecast; 1.52B previous

- U.K. Mortgage Approvals for January 2026: 60.0k (62.5k forecast; 61.01k previous)

- Canada S&P Global Manufacturing PMI for February 2026: 51.0 (50.7 forecast; 50.4 previous)

- U.S. S&P Global Manufacturing PMI Final for February 2026: 51.6 (51.2 forecast; 52.4 previous)

-

ISM U.S. Manufacturing PMI for February 2026: 52.4 (51.3 forecast; 52.6 previous)

- ISM Manufacturing Employment for February 2026: 48.8 (48.0 forecast; 48.1 previous)

- ISM Manufacturing Prices for February 2026: 70.5 (58.2 forecast; 59.0 previous)

- Monetary Policy Committee (MPC) member Alan Taylor warned on Monday that the UK economy is at risk of entering a state of “deficient demand” and indicated that the BoE may soon no longer face a trade-off between fighting inflation and supporting a slowing economy

- The Swiss National Bank said it stands ready to intervene in response to potential currency market impacts from the Iran crisis.

Promotion: Use TradeZella’s AI Powered trade journal to deep-dive into your execution and see exactly how you performed during today’s trading session. Click here to get the TradeZella Edge and use code PIPS20 to save 20% on your subscription!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Monday’s session delivered sharp divergences across asset classes as markets grappled with the unfolding geopolitical crisis in the Middle East while simultaneously processing stronger-than-expected US manufacturing data that revealed surging input costs.

WTI crude oil emerged as the session’s dominant performer, surging 6.80% to close around $71.60 per barrel. The rally began explosively at the Sunday evening open, with prices initially spiking above $75 as traders reacted to weekend developments in Iran, before profit-taking pushed the commodity back below opening levels. Oil found support and trended higher throughout the Monday session as reports confirmed Iran had stepped up drone strikes at key energy facilities across the region, targeting major installations like Aramco’s Ras Tanura refinery and Qatar’s Ras Laffan facility. The sustained advance likely reflected growing concerns about the near halt to traffic through the Strait of Hormuz and disruption at a big refinery in Saudi Arabia, which underscored potential threats to global oil supplies.

Bitcoin rallied 5.78% to trade around $69,316, marking the cryptocurrency’s strongest performance among major assets. The advance appeared to reflect Bitcoin’s growing role as an alternative store of value during geopolitical uncertainty, though the rally occurred alongside both safe-haven and risk assets, suggesting complex positioning dynamics rather than a clear directional bet on market sentiment.

U.S. 10-year Treasury yields climbed 2.61% to settle around 4.05%, reversing early Asian session weakness that had initially pushed yields lower on safe-haven demand. Weighing on Treasuries were figures showing manufacturing expanded, with input prices jumping. The yield advance accelerated following the 10:00 AM ET release of ISM Manufacturing data showing the Prices Paid index surging to 70.5 from 59.0, the highest reading since June 2022. The move likely reflected traders repricing inflation expectations higher given elevated oil prices combined with evidence of persistent manufacturing cost pressures, which together diminished expectations for Federal Reserve rate cuts. Market pricing showed traders are now fully pricing in a first Federal Reserve rate cut for September, with bets on a third reduction in 2026 almost evaporating.

Gold gained 1.15% to close near $5,339 per ounce, continuing its ascent toward record territory as geopolitical tensions drove safe-haven demand. Gold hit above $5,400 during the session before settling slightly lower, with the precious metal supported by its dual role as both an inflation hedge amid rising energy costs and a safe-haven asset during periods of geopolitical stress.

The S&P 500 eked out a modest 0.30% gain to close around 6,885, recovering from an early session decline that had pushed the index down more than 1%. Several tech firms with solid balance sheets rallied. Airlines sank. Energy and defense shares gained amid the geopolitical backdrop, while the recovery in major equity indexes from session lows suggests that, for now, the market views the conflict as a relevant geopolitical risk, but one that remains financially contained in the immediate term.

Promoted: Day traders & Scalpers have better odds of making great decisions if they see & hear market catalysts right away. Get the real-time feed that pros use to catch the news.

Join FinancialJuice for Free to learn more!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

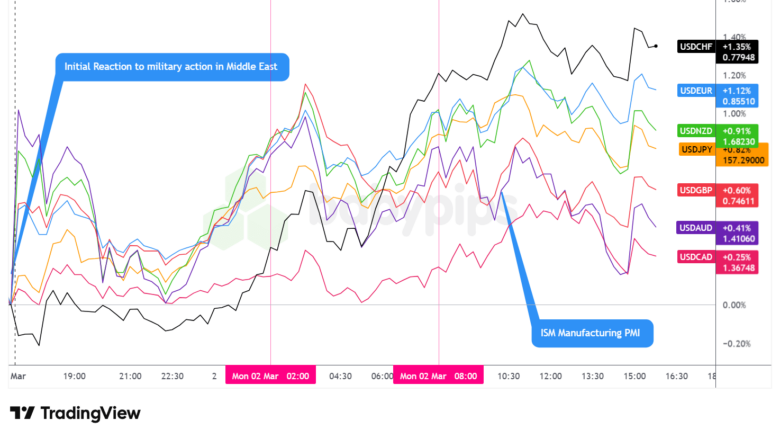

FX Market Behavior: U.S. Dollar vs. Majors

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar emerged as Monday’s strongest performing major currency, posting broad-based gains as geopolitical tensions intersected with hawkish repricing of Federal Reserve rate expectations following the ISM Manufacturing data release.

During the Asian session, the dollar gapped higher on net against the major currencies at the Sunday evening open, likely reflecting positioning ahead of potential energy market disruptions from the Iran conflict. After reaching early peaks, the greenback pulled back by mid-Asia morning as profit-taking emerged and traders assessed the initial oil price action. The dollar found support and rebounded heading into the London session open, with the recovery possibly correlating with oil prices stabilizing at elevated levels after their initial spike and subsequent retracement.

The London session brought choppy price action for the dollar, which initially continued to lean higher before pulling back by mid-morning. The greenback found short-term support around 6:00 AM Eastern Time and slowly trended higher heading into the US session open. During the European morning, the Swiss National Bank delivered an unscheduled intervention warning that sent reverberations through currency markets. The SNB said it stands ready to intervene in currency markets, hardening its tone on foreign exchange to respond to reverberations from the Iran crisis. The central bank’s statement emphasized readiness to intervene in the foreign exchange market to curb a rapid and excessive appreciation of the Swiss franc, which would jeopardize price stability in Switzerland. Following the announcement, the currency fell as much as 1.3% to 0.7795 per dollar, its weakest in a month, marking one of Monday’s most dramatic currency moves.

The U.S. session delivered increased volatility and choppy dollar price action, with the greenback initially pulling lower after US equities opened around 9:30 AM ET before rebounding into the London close at 11:00 AM ET. The 10:00 AM ET ISM Manufacturing release provided a hawkish jolt to markets, with the Prices Paid component surging to 70.5 versus 58.2 expected—an 11.5 percentage point jump from January’s 59.0 reading and the highest since June 2022. The data suggested that inflationary pressures from tariffs and supply chain constraints were intensifying even before oil prices began their geopolitical-driven surge, likely reinforcing trader concerns about sticky inflation that could keep the Federal Reserve on hold for longer.

After the London close, the dollar leaned net bearish but maintained choppy and volatile trading patterns through the afternoon. The greenback’s afternoon weakness may have reflected profit-taking after the morning’s strong advance, though the dollar retained most of its session gains into the close. The complex price action possibly reflected competing forces: safe-haven demand and petrodollar flows supporting the greenback against higher inflation expectations that could eventually force more aggressive Fed tightening, which would be dollar-positive but growth-negative.

Promoted: While new firms come and go with the volatility, The5ers has spent the last 10 years perfecting a funding model that works for the trader. It’s why over 1.6 million traders worldwide trust them to provide the capital and scaling needed to turn market analysis into meaningful professional growth.

Learn more about The5ers Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Upcoming Potential Catalysts on the Economic Calendar

- Australia RBA Bullock Speech at 9:10 pm GMT

- New Zealand Building Permits for January 2026 at 9:45 pm GMT

- Japan Unemployment Rate for January 2026 at 11:30 pm GMT

- U.K. BRC Shop Price Inflation for February 2026 at 12:01 am GMT

- Australia Building Permits Prel for January 2026 at 12:30 am GMT

- Australia Current Account for December 31, 2025 at 12:30 am GMT

- Bank of Japan Gov Ueda Speech at 4:00 am GMT

- Euro area CPI Growth Rate Flash for February 2026 at 10:00 am GMT

- U.K. Spring Economic Statement

- New Zealand Global Dairy Trade Price Index for March 3, 2026

- U.S. Fed Williams Speech at 2:55 pm GMT

- U.S. Fed Kashkari Speech at 4:55 pm GMT

Tuesday’s calendar features the closely watched eurozone flash inflation report at 10:00 am GMT, which will provide critical insight into whether energy price pressures are beginning to flow through to consumer prices following the geopolitical escalation. The reading comes as traders assess whether the European Central Bank’s recent cautious stance on further rate cuts will require adjustment given the new inflationary impulse from oil markets.

RBA Governor Bullock’s evening speech and BOJ Governor Ueda’s morning address will be scrutinized for any commentary on how their respective central banks view the inflation implications of the Middle East conflict, particularly given Japan’s heavy reliance on energy imports and Australia’s position as a major commodity exporter.

Fed speakers Williams and Kashkari during the US session may provide clarity on whether policymakers view the geopolitical risk premium in oil prices as transitory or a more persistent inflation threat that could delay the start of the Fed’s easing cycle.

The UK Spring Economic Statement could provide fiscal policy signals that influence gilt markets and sterling, particularly given MPC member Taylor’s Monday warnings about deficient demand risks that suggest growing divergence between fiscal and monetary policy priorities.

Stay frosty out there, forex friends!

Promoted: How Do Professionals Trade Geopolitical Shocks?

You’ve seen the retail reaction to the military strikes in the Middle East—now see the institutional one. Brent Donnelly’s “The Art of Currency Trading” (4.7 stars & 517 reviews on Amazon) bridges the gap between the news headlines you read and the execution on your screen. It’s a practical, “no-fluff” guide to how professional FX desks navigate the exact type of geopolitical volatility described in today’s report.

Learn more about “The Art of Currency Trading” at Amazon

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.