Ethereum is approaching a milestone that few investors would welcome: its longest run of consecutive monthly losses since the 2018 crypto winter.

Since September 2025, ETH has posted six straight monthly declines, a stretch that has cut its price by roughly 60% from its August 2025 record high of $4,953 to below $2,000.

A losing streak of this length is uncommon for a network that is simultaneously posting record transaction activity, and that contrast makes the current phase notable.

As a result, the immediate issue is not only that ETH has been falling.

The run suggests the market is reevaluating Ethereum’s value amid strong network usage, but the mechanisms that once supported a simple bullish thesis for ETH have become harder to model.

That makes the current drawdown different from the 2018 collapse, when the broader crypto market was coming off an initial coin offering boom and much of the sector was still trying to prove it had enduring product-market fit.

Ethereum in 2026 is a much more mature network. It has deeper institutional relevance, larger on-chain economic activity, and broader use across tokenization, stablecoins, and layer-2 networks.

Yet the token tied to that system is still struggling to hold value.

Bitcoin acts like the index, ETH like the high-beta trade

In broad crypto selloffs, Bitcoin increasingly behaves like the market benchmark, while ETH trades more like the high-beta expression of the sector.

That matters when liquidity thins and sentiment turns defensive. ETH’s market depth is smaller than Bitcoin’s, its positioning is often more leveraged, and its marginal buyer is more sensitive to shifts in macro risk appetite.

When the market de-risks, that structure can turn a broad crypto decline into a sharper move in Ethereum, especially when derivatives rather than spot markets are setting the tone.

This is why ETH’s leverage footprint remains central to that story.

Data from CoinGlass shows that ETH futures open interest has dropped 65% from an August 2025 peak of nearly $70 billion to around $24 billion as of press time. This drastic decline explains the market’s dearth of risks.

Still, it also shows that the ETH price is being formed in a market where forced positioning changes can dominate. Liquidations, hedging, and contract roll-down can overwhelm discretionary buying when traders pull risk.

Notably, options markets have reflected the same tension.

Deribit analytics have shown sharp jumps in short-dated implied volatility and a heavily negative skew, the classic sign of a market paying more for downside protection than upside exposure.

In practical terms, traders are not just expecting movement. They are paying a premium to guard against the move being lower.

That helps explain the market-implied range of outcomes. With seven-day at-the-money implied volatility recently around the high-70% area, the one-standard deviation band suggests roughly a plus-or-minus $200 move over a week, around $1,950 spot.

That widens to about $430 plus or minus over a month and $740 plus or minus over a quarter.

These are not price targets. They are a snapshot of how uncertain the next quarter remains and how wide the market believes the possible paths have become.

The flow picture has not helped ETH bulls

While the derivatives market explains how ETH prices move, they do not fully explain why dips are not finding a more durable buyer.

That brings the focus to capital formation, the slower-moving support that determines whether declines attract fresh money or merely trigger temporary rebounds driven by short covering.

On that front, two signals for ETH have remained weak.

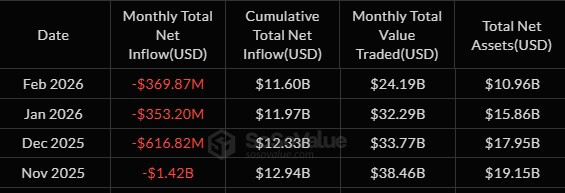

The first is the ETF story.

While daily numbers vary, the broader multi-month trend for U.S.-listed Ethereum ETFs has been net redemptions, with the nine funds registering $2.6 billion outflows over the past four months.

That matters less as a headline about immediate selling pressure than as a statement on institutional persistence.

When ETF flows are not structurally positive, rallies have to be financed elsewhere. In practice, that often means leaning more heavily on the same derivatives complex that can magnify fragility.

At the same time, institutional acquisitions from digital asset treasury firms have slowed significantly, with BitMine being the only major purchaser in recent months.

In fact, ETHZilla, another ETH-focused treasury firm, has dumped its ETH holdings and pivoted towards tokenized real-world assets.

The second is stablecoin supply, one of the clearest real-time proxies for crypto-native purchasing power.

Over the past months, the major stablecoins have experienced a significant slowdown, which has presented challenging possibilities for a broader market recovery.

For context, Tether’s USDT market capitalization has dropped for two consecutive months, signalling that there has not been an expanding pool of fresh liquidity in the space. Notably, this has not occurred since the 2022 collapse of Terra’s USDT algorithmic stablecoin.

That matters for Ethereum because its strongest bull phases have tended to coincide with expanding on-chain purchasing power.

When the stablecoin base is flat, price action can degrade into rotations and leverage-driven moves rather than sustained spot accumulation.

In that kind of environment, rebounds can happen, but they struggle to become self-sustaining.

Ethereum is scaling, but that has complicated the value story

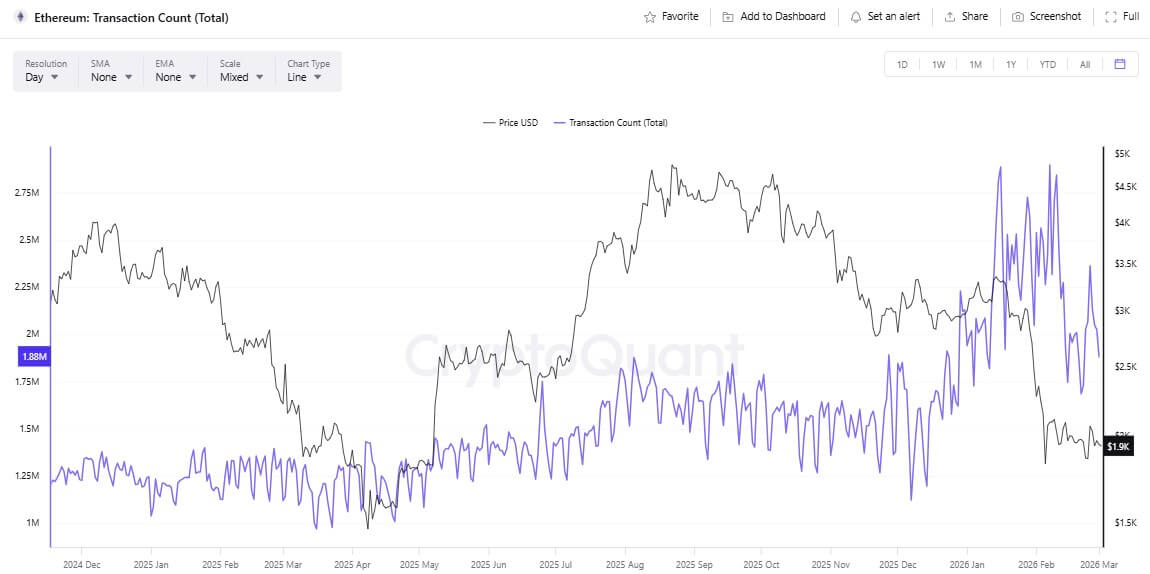

The current downtrend also differs from 2018 because Ethereum’s network is busier and its scaling roadmap is delivering.

Data from CryptoQuant shows Ethereum’s seven-day moving average of daily transactions reached a new high of nearly 2.9 million in early February.

The drivers for this milestone include continued growth in on-chain use cases, such as tokenizing real-world assets, as well as a shift toward cheaper execution, which has lowered transaction costs for users. Lower fees and higher throughput are generally a win for adoption.

But scaling progress has complicated a valuation framework that many investors leaned on in the post-Merge era.

The “ultrasound money” narrative, reinforced by EIP-1559 and the move to proof-of-stake, centered on fee burn as a potential path to shrinking the supply.

This mechanism still works in periods of high fee pressure when blockspace demand rises and fees jump, burn increases, and ETH can turn net deflationary.

However, the key point is that this path has become conditional rather than automatic.

When demand is normal, or when activity migrates to cheaper execution environments, burn pressure falls. The post-Dencun environment illustrates the trade-off. Blob data has made rollups cheaper to operate, allowing layer-2 fees to fall and capacity to expand.

For ETH holders, it also means the base layer may not extract the same fee revenue during ordinary conditions.

Data from Ultrasound.money has shown periods in which ETH issuance exceeds burn.

That weakens the simplified version of an always-deflationary story and forces a more nuanced debate about how Ethereum captures value in a rollup-dominant future.

The network can grow as a settlement layer while the token’s direct monetary case becomes harder to model using analogies investors understand, such as buybacks or dividends.

A six-month losing streak is useful in that context because it suggests the market is repricing the link between ecosystem growth and token value, at a time when macro conditions offer limited support.

What could end the streak?

The next phase for Ethereum likely falls into one of three broad paths.

The first is a capitulation-to-reset outcome. If March 2026 also closes lower, the streak matches the 2018 record, and the psychological burden increases.

In that scenario, ETF redemptions continue, stablecoin supply remains flat, and the options skew remains deeply negative, indicating that hedging demand still dominates.

Price then tends to test the lower edge of the implied volatility cone, not because Ethereum is broken, but because the market wants a bigger discount before taking risk again.

The second is a long period of chop and base-building. This is the less dramatic but perhaps more realistic outcome. Leverage keeps bleeding out, volatility remains elevated but is starting to stabilize, and ETH trades in a wide range while macro data remains mixed.

Ethereum can still show healthier application revenue and stronger layer-2 activity in that world. The difference is that price does not reward it immediately because it is waiting for better liquidity conditions.

The third is a liquidity turn. For ETH to stage a more durable rebound, it likely needs a macro tailwind, some combination of easing risk-off pressure, stabilizing ETF flows and renewed growth in stablecoin purchasing power.

If that happens, the market could start to see Ethereum’s scaling story differently. Instead of focusing on fee compression, investors could put more weight on Ethereum as the settlement layer for a larger economic surface area.

In that framework, the valuation argument moves away from burn alone and toward indispensability.

The main takeaway is that Ethereum is not simply repeating 2018. The market is testing a new narrative under stress.

Ethereum is becoming more usable, but in quiet periods, it is also less obviously monetizable through fees than many investors once assumed.

That tension, combined with macro risk appetite and the quality of capital flowing through ETFs, stablecoins, and derivatives, will determine whether this streak ends as a painful footnote or the start of a longer repricing.