Google Cloud and MoneyGram just signed on to run launch Midnight nodes for new privacy network banks want

Google Cloud, MoneyGram, Vodafone’s Pairpoint, and eToro will run launch-phase nodes on Midnight, a zero-knowledge privacy network targeting a mainnet launch at the end of March 2026.

The pitch isn’t anonymity, but selective disclosure. It’s the ability to prove compliance or settlement eligibility without broadcasting raw customer data onto a public ledger.

Midnight describes these operators as “federated,” meaning a limited, named set running the protocol under explicit coordination rules to prioritize uptime and operational stability during the Kūkolu launch phase.

This phase will be followed by an eventual transition to broader community-driven decentralization, flagged as the Foundation’s intent but not yet scheduled.

This isn’t privacy coins. It’s a zero-knowledge tool that lets firms share verifiable proofs, such as KYC status, eligibility constraints, and settlement completion, while keeping sensitive customer and business data out of public view.

Privacy with guardrails

Midnight’s core claim is that institutions need privacy primitives that don’t trip regulatory wires.

The network uses zero-knowledge proofs to enable selective disclosure: a bank proves it ran AML checks without revealing transaction details, and a broker proves customer accreditation without revealing the customer’s identity.

Disclosure must be explicitly stated in applications, such as “privacy-by-default, disclosure-by-choice” in the network’s framing, making it legible to compliance teams rather than a regulatory red flag.

The federated operator model reflects a deliberate trade-off between centralization.

Launch stability matters more than ideological purity when regulated firms test production workloads, so Midnight starts with a curated set of node operators who commit to participating and adhering to coordination rules.

The Foundation says it intends to transition away from this federated structure toward full decentralization later, but no timeline or criteria have been published.

The real-world implication: Midnight prioritizes operational reliability over censorship resistance at genesis, betting that enterprise-grade infrastructure today builds credibility for broader validator participation tomorrow.

Blue-chip infrastructure players

Google Cloud brings cloud infrastructure and references its Confidential Computing capabilities alongside Mandiant monitoring.

Blockdaemon, which Midnight notes secures over $110 billion in digital assets, joins as a validator services provider. AlphaTON and Shielded Technologies round out the infrastructure side.

The regulated business operators add distribution credibility.

MoneyGram operates in more than 200 countries and territories, giving the network a payments-infrastructure footprint. Pairpoint, the Vodafone and Sumitomo venture, ties in telecom and IoT angles. eToro, with over 35 million users, represents a brokerage and retail trading infrastructure.

| Operator | Category | What it signals (1 line) |

|---|---|---|

| Google Cloud | Cloud/infra | Enterprise hosting + security tooling (Confidential Computing/Mandiant refs) |

| Blockdaemon | Validator services | Institutional-grade validation + “$110B+ secured” claim |

| AlphaTON | Infra | Technical operator capacity |

| Shielded Technologies | Infra | Privacy/security alignment |

| MoneyGram | Payments | Distribution footprint (“200+ countries/territories” claim) |

| Pairpoint (Vodafone/Sumitomo) | Telco/IoT | Enterprise connectivity + data flows angle |

| eToro | Brokerage/retail | Retail rails (“35M+ users” claim) |

| Remaining operators TBD (optional) | — | “Reported target: 10 nodes” (if you keep that line) |

MoneyGram, Pairpoint, and eToro represent three of ten launch nodes, suggesting Midnight plans to name additional operators before the end of the March deadline.

The Foundation hasn’t published a full roster yet, leaving the final composition partially undefined.

The privacy gap gets quantified

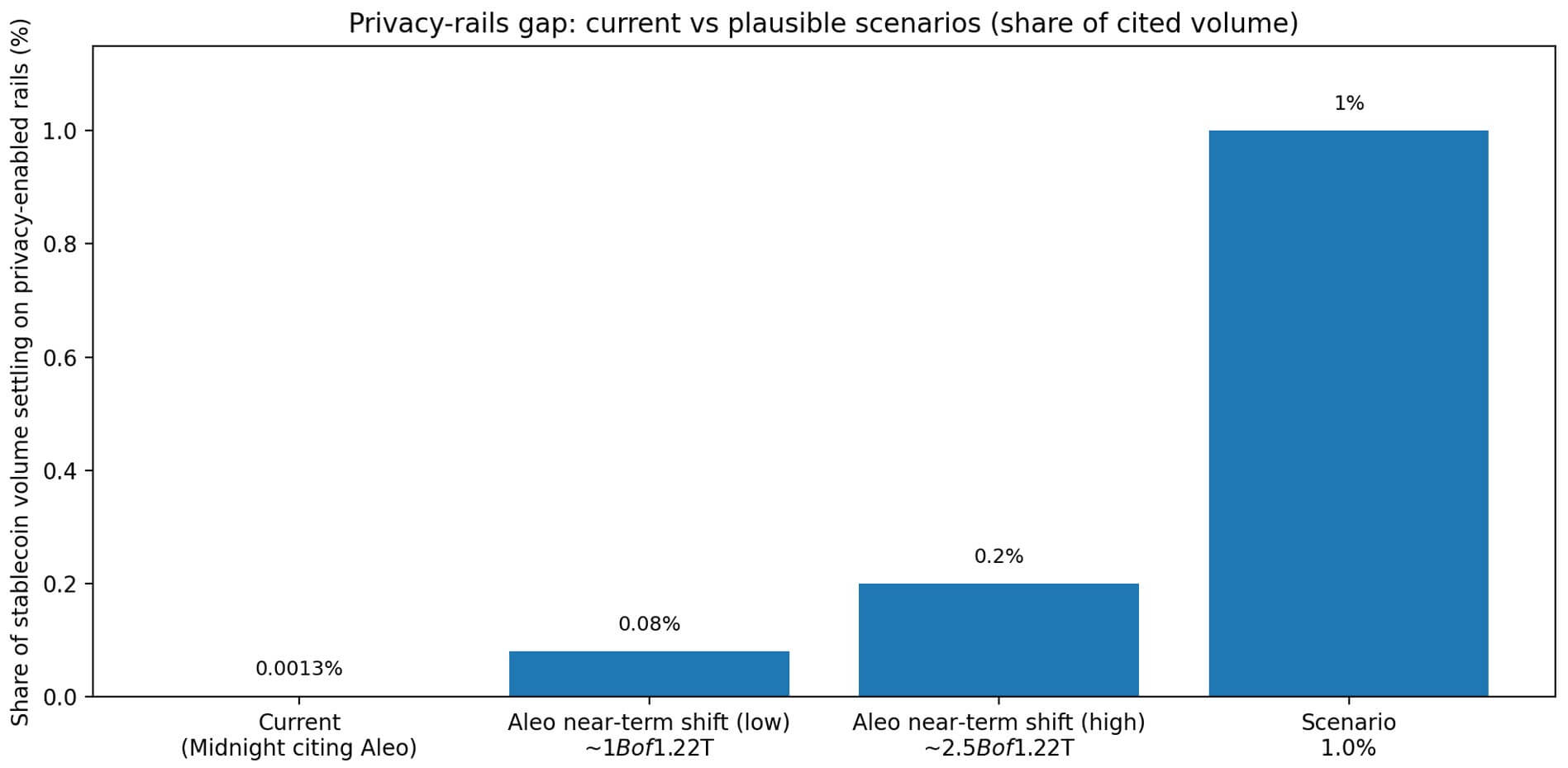

Midnight cites research from Aleo’s 2025 Privacy Gap Report, which claims $1.22 trillion in institutional stablecoin transaction volume, with only 0.0013% settling on privacy-enabled rails.

The framing positions privacy not as a niche crypto-native feature but as an institutional bottleneck: massive on-chain flows moving on transparent infrastructure because compliant privacy tooling doesn’t exist yet.

The timing forces an operator-first strategy. With a mainnet deadline at the end of March, Midnight needed a credible node set locked in early enough to test coordination, uptime, and operational playbooks before genesis.

Recruiting household names, such as cloud providers, payment processors, and telcos, signals enterprise-grade seriousness and creates a trust anchor for early applications.

Broader privacy demand shows up in mainstream surveys. Midnight references Pew Research, which found 81% of respondents were concerned about how companies use their data, with 62% saying it’s impossible to go through daily life without corporations collecting information.

Enterprise primitive vs. federated theater

The bull case treats selective disclosure as a missing primitive for on-chain finance.

Blue-chip operators signal infrastructure and regulatory credibility at launch. Privacy-with-proofs solves real compliance friction: prove you ran checks, prove counterparty eligibility, prove settlement constraints, all without exposing customer records or proprietary business data to public chains.

If successful, Midnight becomes the compliance layer for tokenized securities, payment rails, and identity verification that need verifiable privacy.

The skeptic case sees federated launch as trust assumptions dressed up as pragmatism. A curated operator set running under coordination rules isn’t censorship-resistant decentralization, but a permissioned network with a roadmap promise.

Big names don’t guarantee usage. The real test is whether production applications ship and whether the Foundation publishes credible criteria and timelines for opening validation beyond the initial set.

Operators as distribution infrastructure

Node operators don’t just validate transactions, they function as distribution and trust infrastructure.

Google Cloud signals developer tooling and enterprise cloud integration. MoneyGram and Pairpoint represent payments and IoT data flows. eToro represents retail trading on-ramps.

If these operators translate into production integrations, such as KYC-compliant DeFi, privacy-preserving settlement rails, and tokenized securities with selective disclosure, the network justifies its roster of operators.

The privacy-rails gap Midnight cites offers a scale anchor. If privacy-enabled settlement grows from 0.0013% of stablecoin volume to even 0.1%, that’s $1.25 billion per month shifting to selective-disclosure infrastructure. At 1%, it’s $12.5 billion per month.

Aleo’s own framing suggests $1 billion to $2.5 billion per month as a plausible near-term shift if compliance tooling matures.

Decentralization timeline and application delivery

The federated model creates immediate assumptions about trust.

Midnight controls the operator set, participation rules, and coordination mechanisms at launch. The Foundation’s stated intent to transition toward decentralization matters only if backed by published criteria, timelines, and validator onboarding pathways.

Application delivery determines whether the infrastructure matters. Midnight has signaled new reporting metrics and telemetry around network activity, but production dApps and integrations remain unannounced.

If mainnet launches at the end of March without live applications, and selective disclosure is used for real compliance workflows, the operator roster validates nothing except marketing.

The measurable outcomes

Remaining operator announcements before the end-of-March deadline will reveal whether Midnight hits the reported ten-node target and whether additional operators bring new sectors or geographies.

Published decentralization criteria and timelines determine whether federated launch is a pragmatic choice or a permanent state.

If Midnight releases validator onboarding requirements, governance transition plans, and measurable milestones for community participation, the skeptic’s case weakens.

Genesis applications and integrations around mainnet readiness show whether operators convert into usage. Metrics to watch are production dApps, privacy-preserving settlement rails, or tokenized securities using selective disclosure.

Operator logos without applications mean infrastructure without demand.

Network telemetry and activity reporting, which Midnight says it’s designing, will quantify transaction volume, proof generation, and validator performance.

Compliance layer or controlled launch theater

The broader question isn’t whether privacy tooling matters, but whether Midnight’s federated-then-decentralized model produces a credible compliance primitive or stalls as a permissioned network with household-name validators.

If the hypothesis holds, selective disclosure becomes the default for regulated on-chain activity.

Institutions prove compliance without exposing customer data, settlement rails preserve privacy without compromising auditability, and tokenized securities protect investor information while meeting disclosure requirements.

If it fails, privacy infrastructure fragments across competing networks, federated launch becomes permanent centralization, and big-name operators exit when applications don’t materialize.

The outcome depends on whether Midnight ships decentralization milestones and whether developers build applications that need privacy with proofs, not just privacy.

The end-of-March mainnet deadline starts the clock. Everything after that, like decentralization progress, application delivery, and validator expansion, determines whether Midnight’s blue-chip roster built a compliance layer or just ran an expensive testnet with good PR.