Markets navigated conflicting signals on Thursday as optimism around US-Iran nuclear talks pressured oil prices lower while hawkish Bank of Japan rhetoric lifted the yen, even as US equities struggled to overcome lingering concerns about AI sector valuations following Nvidia’s mixed reception.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- New Zealand ANZ Business Confidence for February 2026: 59.2 (67.0 forecast; 64.1 previous)

- Australia Private Capital Expenditure for December 31, 2025: 0.4% q/q (0.3% q/q forecast; 6.4% q/q previous)

- Japan Leading Indicators Index for December 2025: 111.0 (110.2 forecast; 109.9 previous)

- Swiss Non Farm Payrolls for December 31, 2025: 5.54M (5.54M forecast; 5.53M previous)

- Euro area Loans to Households for January 2026: 3.0% y/y (3.0% y/y forecast; 3.0% y/y previous)

- Euro area Loans to Companies for January 2026: 2.8% y/y (3.0% forecast; 3.0% y/y previous)

- Euro area Selling Price Expectations for February 2026: 11.5 (9.0 forecast; 10.0 previous)

-

Euro area Consumer Confidence for February 2026: -12.2 (-12.2 forecast; -12.4 previous)

- Euro area Consumer Inflation Expectations for February 2026: 25.8 (22.0 forecast; 24.1 previous)

- Canada Average Weekly Earnings for December 2025: 1.9% y/y (2.3% y/y forecast; 2.5% y/y previous)

- U.S. Initial Jobless Claims for February 21, 2026: 212.0k (210.0k forecast; 206.0k previous)

- U.S. Kansas Fed Manufacturing Index for February 2026: 10.0 (-1.0 forecast; -2.0 previous)

- New Zealand ANZ Roy Morgan Consumer Confidence for February 2026

Promotion: Use TradeZella’s AI Powered trade journal to deep-dive into your execution and see exactly how you performed during today’s trading session. Click here to get the TradeZella Edge and use code PIPS20 to save 20% on your subscription!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Thursday’s session delivered divergent asset performance as geopolitical developments in US-Iran relations competed with technology sector concerns and hawkish central bank messaging from Japan for market attention.

The S&P 500 declined 1.02% to close around 6,892, extending losses as the index failed to find support despite paring some intraday weakness. The benchmark opened lower during Asian trading hours but stabilized through the London session, eventually accelerating its decline into the US morning hours. The persistent weakness appeared linked to continued skepticism about artificial intelligence sector valuations, with Nvidia’s 5.5% decline weighing heavily despite the chipmaker’s better-than-expected quarterly results. The selloff reflected growing investor concerns that massive AI infrastructure spending may not translate into sustainable profit margins, particularly as competition intensifies in the compute space.

US 10-year Treasury yields fell 1.13% to settle around 4.01%, declining steadily through most of the session in a move that suggested safe-haven demand amid equity weakness and geopolitical uncertainty. Yields traded relatively flat through Asian hours near 4.057% before beginning a gradual descent during the U.S. session. The decline stabilized after touching session lows around 4.015% in late afternoon trading. The bond market’s strength occurred despite no significant domestic economic catalysts, possibly reflecting positioning ahead of Friday’s key economic releases or concerns about growth momentum given the equity selloff and mixed economic sentiment data from Europe.

Gold advanced 0.42% to close near 5,184 per ounce, grinding higher throughout the session in a pattern consistent with safe-haven flows and ongoing geopolitical tensions. The precious metal opened Asian trading around 5,163 and traded in a tight range through early London hours before beginning a steady climb that persisted into US afternoon trading. Gold reached session highs above 5,206 during mid-US session before pulling back modestly into the close. The advance came despite a firmer US dollar against most major currencies, suggesting demand was driven more by uncertainty around US-Iran negotiations and AI sector volatility than currency dynamics. With no direct gold-specific catalysts to point to, the metal’s strength likely reflected broad risk hedging as traders balanced optimistic signals from Geneva talks against the reality that previous rounds have failed to produce lasting agreements.

WTI crude oil whipsawed throughout the session in volatile trading that appeared closely tied to evolving commentary on US-Iran nuclear negotiations. Oil opened Asian trading near 65.81 and initially rallied toward 66.63 during early London hours, possibly on overnight concerns about Middle East tensions following Vice President Vance’s comments about Iran’s nuclear weapons program. However, the rally quickly reversed as Oman’s foreign minister reported “unprecedented openness” in Geneva talks, with prices plunging to session lows around 63.59 during mid-London trading. Oil recovered through the US session, stabilizing in a choppy range between 65.00 and 65.50. The dramatic intraday reversal reflected market sensitivity to any progress in nuclear talks that could eventually lead to sanctions relief and additional Iranian supply, though traders appeared skeptical given the history of failed negotiations.

Bitcoin declined 2.13% to close around 67,422, extending recent weakness in a move that appeared disconnected from traditional risk asset performance. The cryptocurrency traded lower through Asian before beginning a stronger decline during US morning trading. With no apparent crypto-specific catalysts to point to, the weakness possibly reflected continued deleveraging in speculative positions or concerns that AI sector uncertainty might spill over into other technology-adjacent assets. The decline came despite gold’s advance, suggesting Bitcoin’s safe-haven credentials remain secondary to its correlation with risk appetite in growth-oriented technology sectors.

Promoted: Smart trading is about more than just reading fundies and price action; it’s about having a platform that can handle high-volatility events like geopolitical issues high profile earnings events. Crypto.com provides a seamless interface for both beginners and seasoned pros. Learn more here at Crypto.com!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

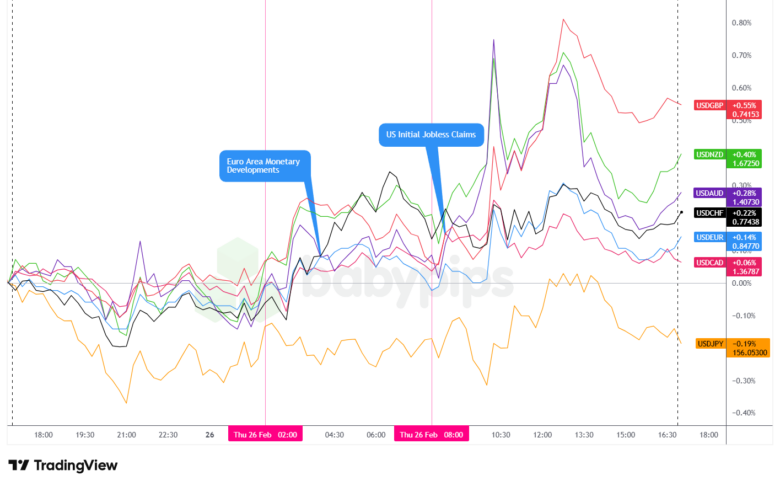

FX Market Behavior: U.S. Dollar vs. Majors

Overlay of USD vs. Majors – Chart Faster With TradingView

The US dollar posted choppy but ultimately stronger performance on Thursday, closing as a net outperformer against most major currencies with the notable exception of the Japanese yen, which rallied on increasingly hawkish Bank of Japan rhetoric.

During the Asian session, the dollar dipped initially against most major currencies before stabilizing and trading sideways heading into the London session. The early weakness appeared to correlate with overnight positioning adjustments, though no significant regional economic catalysts emerged to drive clear directional momentum. Japanese markets provided the primary exception, with the yen strengthening following comments from BOJ Governor Ueda indicating the central bank remains on track to tighten further if economic conditions strengthen. BOJ board member Hajime Takata, widely regarded as the most hawkish voice on the policy board, reinforced this message by warning that policymakers must focus on inflation overshoot risks as medium- and long-term price expectations rise. These comments appeared to shift market pricing for potential rate hikes in March or April, lending support to the yen that persisted throughout the session.

The London session brought a reversal in dollar fortunes as the greenback rebounded against major currencies and stabilized through European trading hours. The recovery appeared to correlate with mixed European economic sentiment data, particularly disappointing readings from the euro area that showed services sentiment falling to 5.0 from 7.2 and economic sentiment declining to 98.3 versus 99.4 expected. More concerning for euro bulls, selling price expectations jumped to 11.5 from 10.0, well above the 9.0 forecast, while consumer inflation expectations surged to 25.8 from 24.1, signaling persistent price pressures that could complicate ECB policy decisions. Industrial sentiment also deteriorated further, falling to -7.1 from -6.8. These softer eurozone indicators appeared to provide relative support for the dollar, though the greenback dipped slightly heading into the US session, possibly reflecting pre-positioning ahead of US economic data.

During the US session, the dollar rallied steadily through most of US trading hours, even with Initial Jobless Claims coming in slightly above the 210,000 forecast but still suggesting labor market resilience. The Kansas Fed Manufacturing Index provided an upside surprise, surging to 10.0 from -2.0 previous, well above the -1.0 forecast, offering evidence that manufacturing activity may be stabilizing in some regions despite broader industrial weakness. The dollar maintained its bid through US afternoon trading before pulling back modestly heading into the close, possibly on profit-taking as traders squared positions ahead of Friday’s busy economic calendar.

Promoted: While new firms come and go with the volatility, The5ers has spent the last 10 years perfecting a funding model that works for the trader. It’s why over 1.6 million traders worldwide trust them to provide the capital and scaling needed to turn market analysis into meaningful professional growth.

Learn more about The5ers Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Upcoming Potential Catalysts on the Economic Calendar

- Japan Tokyo CPI for February 2026 at 11:30 pm GMT

- Japan Industrial Production Prel for January 2026 at 11:50 pm GMT

- Japan Retail Sales for January 2026 at 11:50 pm GMT

- U.K. Gfk Consumer Confidence for February 2026 at 12:01 am GMT

- Australia Private & Housing Sector Credit for January 2026 at 12:30 am GMT

- Japan Construction Orders for January 2026 at 5:00 am GMT

- Japan Housing Starts for January 2026 at 5:00 am GMT

- Germany Import Prices for January 2026 at 7:00 am GMT

- France GDP Growth Rate Final for December 31, 2025 at 7:45 am GMT

- France Non Farm Payrolls QoQ for December 31, 2025 at 7:45 am GMT

- France Inflation Rate Updates Prel for February 2026 at 7:45 am GMT

- Swiss KOF Leading Indicators for February 2026 at 8:00 am GMT

- Swiss GDP Growth Rate Final for December 31, 2025 at 8:00 am GMT

- Germany Employment Update for February 2026 at 8:55 am GMT

- Euro area ECB Consumer Inflation Expectations for January 2026 at 9:00 am GMT

- Canada CFIB Business Barometer for February 2026 at 12:00 pm GMT

- Germany Inflation Rate Prel for February 2026 at 1:00 pm GMT

- Canada GDP Prel for January 2026 at 1:30 pm GMT

- U.S. PPI for January 2026 at 1:30 pm GMT

Friday’s calendar features dense data flow across multiple regions, with particular focus on inflation readings from France and Germany that could influence ECB policy expectations following Thursday’s mixed eurozone sentiment indicators. Japan’s Tokyo CPI and industrial production data will be closely watched for signals about the strength of the economic backdrop supporting the BOJ’s increasingly hawkish messaging.

During the US session, the January PPI report represents the key catalyst, with markets seeking confirmation that producer-level price pressures are moderating to support the disinflation narrative, while Canada’s preliminary January GDP will provide insight into whether North American growth momentum carried into the new year despite ongoing trade policy uncertainties.

Stay frosty out there, forex friends!

Promoted: The Strategy is Half the Battle; Your Mindset is the Rest.

Today’s Daily Recap highlights a market driven by geopolitical drivers and AI themes. But as any pro will tell you, a great thesis can still fail if the trader lacks the discipline to execute it.

In “Unknown Market Wizards,” Jack Schwager interviews successful traders to reveal a common truth: their edge isn’t just knowledge or skills—it’s their psychological resilience and rigid risk control. Whether you’re navigating the odds of war or AI related earnings, learn how the “wizards” stay clinical when the rest of the market is emotional.

Master Your Trading Mindset with Market Wizards!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.