Equity markets rebounded from AI-driven selloff concerns on Tuesday as technology stocks rallied on improved consumer confidence and reduced artificial intelligence disruption fears, though currency markets remained cautious ahead of President Trump’s evening State of the Union address.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

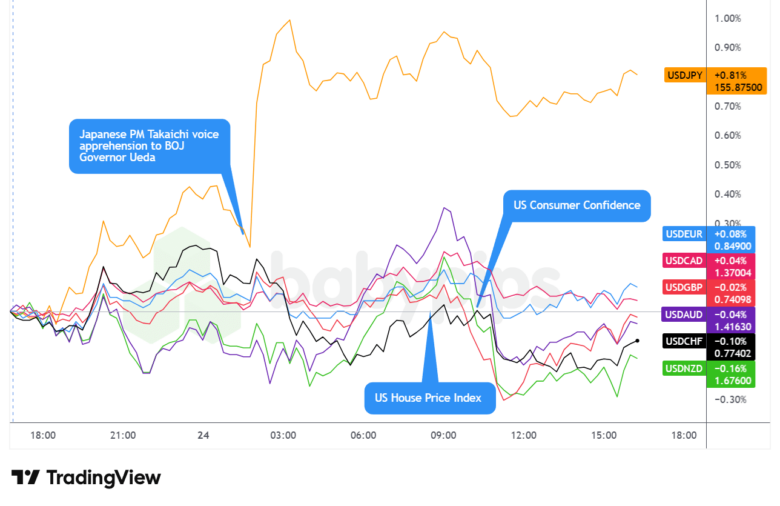

- Japanese Prime Minister Sanae Takaichi voice apprehension to Bank of Japan Governor Kazuo Ueda over more rate hikes

- France Business Confidence for February 2026: 102.0 (104.0 forecast; 105.0 previous)

- Swiss National Bank Chair Schlegel said that many parts of the economy has proved resilient despite tariffs and uncertainty

- U.K. CBI Distributive Trades for February 2026: -43.0 (-17.0 forecast; -17.0 previous)

- U.S. ADP Employment Change Weekly for February 7, 2026: 12.75k (10.25k previous)

- Canada Manufacturing Sales Prel for January 2026: -3.3% m/m (0.4% m/m forecast; 0.6% m/m previous)

- U.S. S&P/Case-Shiller Home Price for December 2025: -0.1% m/m (-0.1% m/m forecast; 0.0% m/m previous); 1.4% y/y (1.4% y/y forecast; 1.4% y/y previous)

- CB U.S. Consumer Confidence for February 2026: 91.2 (85.0 forecast; 84.5 previous)

- Richmond Fed Manufacturing Index for February 2026: -10.0 (-8.0 forecast; -6.0 previous)

- U.S. Wholesale Inventories for December 2025: 0.2% m/m (0.1% m/m forecast; 0.2% m/m previous)

- Dallas Fed Services Index for February 2026: -3.2 (1.6 forecast; 2.7 previous)

- U.S. Money Supply for January 2026: 22.44 (22.4 previous)

- Federal Reserve Governor Cook warned that the Fed may not be able to counter rising unemployment driven by artificial intelligence.

- Bank of England Governor Andrew Bailey said on Tuesday that an interest rate cut in March is an “open question”

- BOE Chief Economist Pill and BOE member Greene took a hawkish stance on interest rates on Tuesday on fears of inflation bouncing back up.

Promotion: Use TradeZella’s AI Powered trade journal to deep-dive into your execution and see exactly how you performed during today’s trading session. Click here to get the TradeZella Edge and use code PIPS20 to save 20% on your subscription!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Tuesday’s session reflected mixed themes as technology stocks rebounded from recent artificial intelligence disruption concerns, but broader market participation remained cautious amid mixed economic signals and geopolitical uncertainty.

U.S. equities rallied on the day, with the S&P 500 climbing 0.64% to close around 6,887. The index experienced light volatility during overnight trading before finding support during the London session near 6,833. The rally gained momentum heading into the US open and extended through midday, reaching session highs around 6,897 before pulling back modestly into the close. The advance appeared driven primarily by technology sector strength, with software firms rebounding after Anthropic’s messaging about AI integration rather than displacement likely helped ease recent concerns about entire business models becoming obsolete. Advanced Micro Devices jumped approximately 9% on Meta Platforms’ plans to spend billions on its gear, while the broader rally suggested improving risk sentiment following the better-than-expected consumer confidence report.

Gold declined 1.50% to settle near 5,157, pulling back from recent highs in what appeared to be profit-taking after the precious metal’s strong performance in preceding sessions. The metal slid through the Asia and London sessions but bottomed out heading into the US open, where it then stabilized. With no direct gold-specific catalysts to point to and equities rallying, the move likely reflected reduced safe-haven demand as risk appetite improved and traders repositioned ahead of President Trump’s evening State of the Union address.

Bitcoin fell 0.62% to trade near 64,223, underperforming traditional risk assets despite the equity rally. The cryptocurrency opened the session around 64,998 and dropped through Asian and London hours. Bitcoin recovered most of its intraday losses through US trade but remained in negative territory at the close.

WTI crude oil posted modest gains of 0.26% to close around 66.14. Oil opened the session near 66.26 and traded higher through the Asian session before declining during early London hours to lows around 65.53. The commodity found support and rallied ahead of the US session open then pulled back and fell lower through most of the rest of the US session. There were no specific energy-related catalysts during the trading day to directly explain the choppy price action, so it’s likely a mix of cautiousness surrounding geopolitical themes and wait-and-see mode ahead of the SOTU address.

Treasury yields advanced 0.05% to settle around 4.034% on the 10-year note, with yields trading in a relatively tight range throughout the session. Bonds opened around 4.034% and remained largely rangebound through Asian and London trading despite the mixed economic data releases. Yields dipped modestly during the US morning before stabilizing into the afternoon close. The muted bond market reaction suggested traders were parsing the mixed signals from weaker regional Fed manufacturing data against the stronger consumer confidence report, with positioning likely cautious ahead of President Trump’s State of the Union address scheduled for later in the evening.

Promoted: Smart trading is about more than just reading fundies and price action; it’s about having a platform that can handle high-volatility events like US-Iran geopolitical issues. Crypto.com provides a seamless interface for both beginners and seasoned pros. Learn more here at Crypto.com!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

FX Market Behavior: U.S. Dollar vs. Majors

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar traded choppy and mixed throughout Tuesday, closing with an arguably neutral to slightly positive lean against major currencies despite dovish commentary from multiple Federal Reserve officials.

During the Asian session, the US dollar traded mostly choppy and sideways against the major currencies with an arguably net bullish lean. The modest dollar strength came despite Japanese Prime Minister Takaichi voicing concerns to BOJ Governor Ueda about further rate hikes, which typically would support yen weakness. China’s decision to hold its loan prime rates steady at 3.0% and 3.5% provided little directional catalyst, while China’s onshore yuan climbed to its strongest level against the dollar in nearly three years as traders returned from a nine-day holiday. The dollar’s resilience during Asian hours possibly reflected cautious positioning ahead of the US consumer confidence data and President Trump’s evening speech.

The London session brought the dollar lower initially before a modest rebound heading into the US open. During the Tuesday morning London session, the US dollar pulled back slightly against most major currencies, possibly correlating with improving risk sentiment in European equity markets. French business confidence came in weaker than expected at 102.0 versus 104.0 forecast, while UK CBI Distributive Trades disappointed sharply at -43.0 versus -17.0 expected, yet these misses failed to provide sustainable dollar support. Bank of England Governor Bailey’s comments characterizing a March rate cut as an “open question” added to sterling volatility, though the pound’s reaction remained muted. The dollar rebounded modestly heading into the US session open, possibly reflecting pre-positioning ahead of the consumer confidence release.

The U.S. session saw choppy two-way trading with the dollar initially strengthening before reversing direction. After the U.S. session opened, the U.S. dollar rebounded and then reversed lower against the major currencies following the better-than-expected consumer confidence report at 10:00 am ET, which showed a reading of 91.2 versus 85.0 expected. The strong confidence data initially pressured the dollar as improved consumer sentiment reduced expectations for aggressive Fed easing, but this reaction proved short-lived. After the U.S. equities open, the dollar bottomed out just after the London session closed and slowly ground higher heading into the end of the Tuesday session. The intraday reversal possibly reflected multiple factors, including dovish Fed commentary from Governor Cook about AI-driven unemployment risks, mixed regional Fed manufacturing data showing continued weakness, and cautious positioning ahead of President Trump’s State of the Union address scheduled for 9:00 pm ET.

Promotion: If your confidence has grown in your market awareness & strategies with this market recap, and you wanna take action, Maven Trading can help. They provide simulated funding challenges starting as low as $13, allowing you to trade major pairs with professional-sized capital. No time limits mean you can take swing plays on these market themes without the pressure of a ticking clock.

Learn More About Maven Trading Today!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Upcoming Potential Catalysts on the Economic Calendar

- Australia CPI Growth Rate for January 2026 at 12:30 am GMT

- Australia Construction Work Done for December 31, 2025 at 12:30 am GMT

- U.S. President Trump State of the Union Speech at 2:00 am GMT

- Germany GDP Growth Rate Final for December 31, 2025 at 7:00 am GMT

- Germany GfK Consumer Confidence for March 2026 at 7:00 am GMT

- France Consumer Confidence for February 2026 at 7:45 am GMT

- Swiss Economic Sentiment Index for February 2026 at 9:00 am GMT

- Euro area CPI Growth Rate Final for January 2026 at 10:00 am GMT

- U.S. MBA 30-Year Mortgage Rate for February 20, 2026 at 12:00 pm GMT

- Canada Wholesale Sales Prel for January 2026 at 1:30 pm GMT

- U.S. Fed Barkin Speech at 2:35 pm GMT

- U.S. EIA Crude Oil Stocks Change for February 20, 2026 at 3:30 pm GMT

- U.S. Fed Musalem Speech at 6:20 pm GMT

- U.S. Fed Balance Sheet for February 25, 2026 at 9:30 pm GMT

Wednesday’s calendar features President Trump’s State of the Union address overnight, which could provide clarity on the administration’s economic priorities and any policy initiatives that might influence market sentiment heading into the remainder of the week. Australian inflation data early Wednesday Asia morning may offer insights into Reserve Bank of Australia policy trajectory, while eurozone final CPI figures could influence ECB rate cut expectations.

During the US session, Canadian wholesale sales and Fed speeches from Barkin and Musalem will be monitored for any shifts in central bank communication following Tuesday’s mixed economic data. The EIA crude oil inventory report could spark energy market volatility given recent geopolitical tensions, while markets remain sensitive to any fresh commentary on the balance between labor market resilience and inflation persistence.

Stay frosty out there, forex friends!

Promotion: We’ve got the Fundies to help us choose markets and biases, but a great thesis needs a precise entry. Bring your daily recap insights to life on TradingView’s Supercharts. Use professional-grade drawing tools and 100,000+ community indicators to identify the exact technical levels where the smart money is moving. Don’t just follow the trend—visualize it.

Level Up Your Edge on TradingView

Disclosure: To help support our content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.