Markets wrestled with renewed tariff uncertainty on Monday as President Trump’s weekend announcement of a 15% global tariff under Section 122 authority replaced the Supreme Court-struck reciprocal framework, while Federal Reserve Governor Christopher Waller dampened March rate cut expectations by describing the decision as a “coin flip” following January’s stronger employment data.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- New Zealand Retail Sales Growth for December 31, 2025: 0.9% q/q (1.0% q/q forecast; 1.9% q/q previous); 4.4% y/y (3.6% y/y forecast; 4.5% y/y previous)

- New Zealand Credit Card Spending for January 2026: 1.0% y/y (0.2% y/y forecast; -0.3% y/y previous)

- Swiss Producer & Import Prices for January 2026: -0.2% m/m (0.2% m/m forecast; -0.2% m/m previous); -2.2% y/y (-1.1% y/y forecast; -1.8% y/y previous)

-

Germany Ifo Business Climate for February 2026: 88.6 (87.9 forecast; 87.6 previous)

- Germany Ifo Expectations for February 2026: 90.5 (89.8 forecast; 89.5 previous)

- Chicago Fed National Activity Index for January 2026: 0.18 (0.3 forecast; -0.04 previous)

-

U.S. Factory Orders for December 2025: -0.7% m/m (0.9% m/m forecast; 2.7% m/m previous)

- U.S. Factory Orders ex Transportation for December 2025: 0.4% m/m (0.1% m/m forecast; 0.2% m/m previous)

- U.S. Dallas Fed Manufacturing Index for February 2026: 0.2 (-3.5 forecast; -1.2 previous)

- On Monday, Federal Reserve governor Christopher Waller said that January’s solid job gains could mean the Fed may skip a rate cut in March

- European Central Bank President Lagarde said on Monday that the ECB must be “agile” in setting monetary policy

Promotion: Use TradeZella’s AI Powered trade journal to deep-dive into your execution and see exactly how you performed during today’s trading session. Click here to get the TradeZella Edge and use code PIPS20 to save 20% on your subscription!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Monday’s session reflected persistent trade policy uncertainty as markets digested the implications of President Trump’s pivot to Section 122 tariff authority following the Supreme Court’s Friday ruling that struck down his IEEPA-based reciprocal framework.

Gold emerged as the session’s strongest performer, climbing 2.45% to close around $5,229 per ounce, reaching a three-week high. The precious metal’s advance likely reflected safe-haven demand amid heightened tariff uncertainty and geopolitical tensions. The rally appeared to accelerate during the US session, possibly correlating with Trump’s threatening remarks about nations that attempt to renegotiate trade deals, alongside ongoing US-Iran nuclear negotiation developments scheduled for Thursday.

WTI crude oil posted modest gains of 0.51% to settle near $66.40 per barrel. The advance likely reflected a combination of factors including supply concerns stemming from weekend reports that Iran signed a €500 million deal with Russia for advanced air-defense missiles, alongside ongoing uncertainty about US-Iran relations as nuclear talks approached. Oil found support despite tariff-related demand concerns that have pressured energy markets in recent weeks.

U.S. equities declined for a fourth consecutive session, with the S&P 500 falling 1.18% to close around 6,828. The index weakened steadily through the trading day, possibly reflecting concerns that renewed tariff confusion could disrupt corporate supply chains and dampen economic growth. The selloff correlated with Fed Governor Waller’s comments suggesting the central bank retains flexibility on rate policy (both cut and no cut on the table), with traders potentially focusing more on the “no cut” area of possibilities given January’s positive jobs data.

Bitcoin extended recent losses, dropping 4.97% to trade near $64,430. The cryptocurrency experienced selling pressure throughout the session with no apparent direct crypto-specific catalysts to point to. The weakness possibly reflected broader risk-off sentiment as traders digested the tariff policy uncertainty, or concerns that elevated interest rates and inflation may reduce appetite for speculative digital assets.

The 10-year Treasury yield declined 1.27% to approximately 4.03%. Bond yields fell through most of the session, likely correlating with the equity market weakness and safe-haven flows into government debt amid trade policy uncertainty. The move lower in yields occurred despite Waller’s hawkish-leaning comments about March rate cut odds being a “coin flip,” suggesting traders were more focused on growth risks from tariff disruptions than the timing of Fed easing.

Promoted: Smart trading is about more than just reading fundies and price action; it’s about having a platform that can handle high-volatility events like US-Iran geopolitical issues. Crypto.com provides a seamless interface for both beginners and seasoned pros. Learn more here at Crypto.com!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

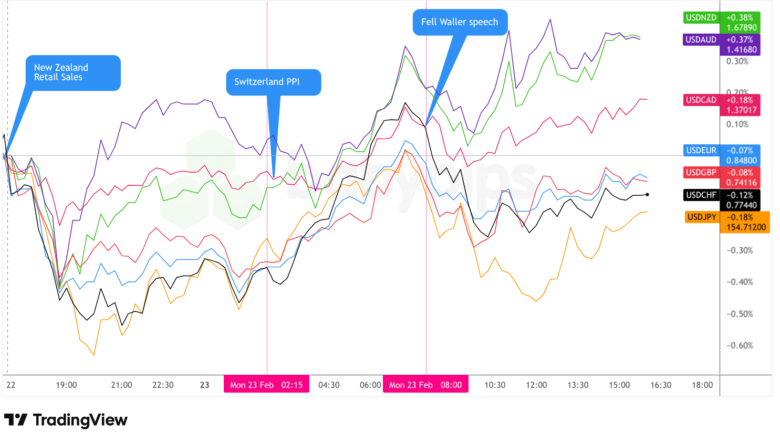

FX Market Behavior: U.S. Dollar vs. Majors

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar experienced choppy trading throughout Monday, ultimately posting mixed results against major currencies as traders navigated conflicting signals from tariff policy developments, Federal Reserve commentary, and geopolitical tensions.

During the Asian session, the dollar dipped at the Monday open, possibly reflecting overnight positioning adjustments following Trump’s Saturday announcement of the 15% global tariff increase. However, the greenback found a bottom mid-morning Asia and slowly rebounded heading into the London open. With Japanese and mainland Chinese markets closed for holidays, thin regional liquidity likely amplified some of the currency moves. The dollar’s recovery through the latter part of the Asian session possibly correlated with growing recognition that Trump’s new tariff framework, while legally different, maintains significant trade barriers that could support the dollar’s safe-haven appeal.

The London session brought the most decisive directional move, with the dollar rallying on net against the major currencies. The advance likely reflected a combination of factors including better-than-expected German Ifo business climate data (88.6 versus 87.9 forecast), which may have reduced European growth concerns but didn’t meaningfully pressure the dollar. More significantly, reports that the European Union froze ratification of its US trade deal likely reinforced perceptions that global trade tensions remain elevated, potentially supporting dollar safe-haven flows. The dollar’s strength during London hours occurred despite the absence of major US economic catalysts, suggesting positioning adjustments and cross-border capital flows were the dominant drivers.

After the US session open, the dollar dipped again as traders likely positioned ahead of Fed Governor Waller’s speech. However, the greenback quickly found a bottom and rebounded through the rest of the session. Waller’s comments around 8:00 am ET characterized a March rate cut as a “coin flip” and emphasized that policy remains restrictive but there’s “no rush” to ease given elevated inflation. This balanced message appeared to support the dollar by tempering aggressive rate cut expectations without entirely removing Fed flexibility. The dollar’s recovery through the US afternoon possibly also reflected Trump’s threatening social media post about “much higher” tariffs for nations attempting to renegotiate trade deals, which may have reinforced safe-haven demand for the greenback.

The mixed currency performance suggested that Monday’s dominant theme was uncertainty rather than a clear directional trade policy narrative, with traders likely awaiting clarity on whether Trump’s Section 122 tariffs will face legal challenges or whether trading partners will honor existing agreements under the new framework.

Promotion: If your confidence has grown in your market awareness & strategies with this market recap, and you wanna take action, Maven Trading can help. They provide simulated funding challenges starting as low as $13, allowing you to trade major pairs with professional-sized capital. No time limits mean you can take swing plays on these market themes without the pressure of a ticking clock.

Learn More About Maven Trading Today!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Upcoming Potential Catalysts on the Economic Calendar

- France Business Confidence for February 2026 at 7:45 am GMT

- U.K. CBI Distributive Trades for February 2026 at 11:00 am GMT

- U.S. Fed Golsbee Speech at 1:00 pm GMT

- U.S. ADP Employment Change Weekly for February 7, 2026 at 1:15 pm GMT

- Canada Manufacturing Sales MoM Prel for January 2026 at 1:30 pm GMT

- U.S. House Price Index for December 2025 at 2:00 pm GMT

- U.S. Fed Bostic Speech at 2:00 pm GMT

- U.S. Fed Collins Speech at 2:00 pm GMT

- U.S. Fed Waller Speech at 2:15 pm GMT

- U.S. Fed Cook Speech at 2:30 pm GMT

- U.S. Wholesale Inventories MoM for December 2025 at 3:00 pm GMT

- U.S. Richmond Fed Manufacturing Index for February 2026 at 3:00 pm GMT

- U.S. CB Consumer Confidence for February 2026 at 3:00 pm GMT

- U.S. Dallas Fed Services Index for February 2026 at 3:30 pm GMT

- U.S. Money Supply for January 2026 at 6:00 pm GMT

Tuesday’s calendar features elevated volatility potential with a heavy slate of Federal Reserve speakers including Goolsbee, Bostic, Collins, Waller, and Cook throughout the US session. Markets will parse their commentary for additional clarity on the March rate decision following Waller’s Monday characterization of the vote as a “coin flip.” The ADP weekly employment report at 1:15 pm GMT could provide insight into private sector hiring trends ahead of Friday’s official February jobs data, though traders may approach the figure cautiously given recent distortions from the government shutdown.

The Conference Board consumer confidence reading at 3:00 pm GMT will be closely monitored for any deterioration in sentiment stemming from renewed tariff uncertainty and elevated inflation concerns. Weakness in consumer confidence could reinforce concerns about economic momentum heading into the spring, potentially supporting the case for earlier Fed rate cuts despite Waller’s hawkish-leaning Monday remarks.

Markets remain sensitive to any developments in the ongoing tariff saga, particularly whether additional trading partners follow the EU’s lead in freezing trade deal ratification or whether the Trump administration provides clarity on how Section 122 tariffs will be implemented and enforced.

Stay frosty out there, forex friends!

Promoted: How Do Professionals Trade Tariff News?

You’ve seen the retail reaction to the tariff whiplash—now see the institutional one. Brent Donnelly’s “The Art of Currency Trading” (4.7 stars & 517 reviews on Amazon) bridges the gap between the news headlines you read and the execution on your screen. It’s a practical, “no-fluff” guide to how professional FX desks navigate the exact type of geopolitical volatility described in today’s report.

Learn more about “The Art of Currency Trading” at Amazon

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.