Major German bank opens free crypto access as MiCA ends the legality debate and sparks a bank rush

Germany’s ING Deutschland just made crypto exposure feel like buying an index fund, indicating the path Europe is taking in crypto adoption.

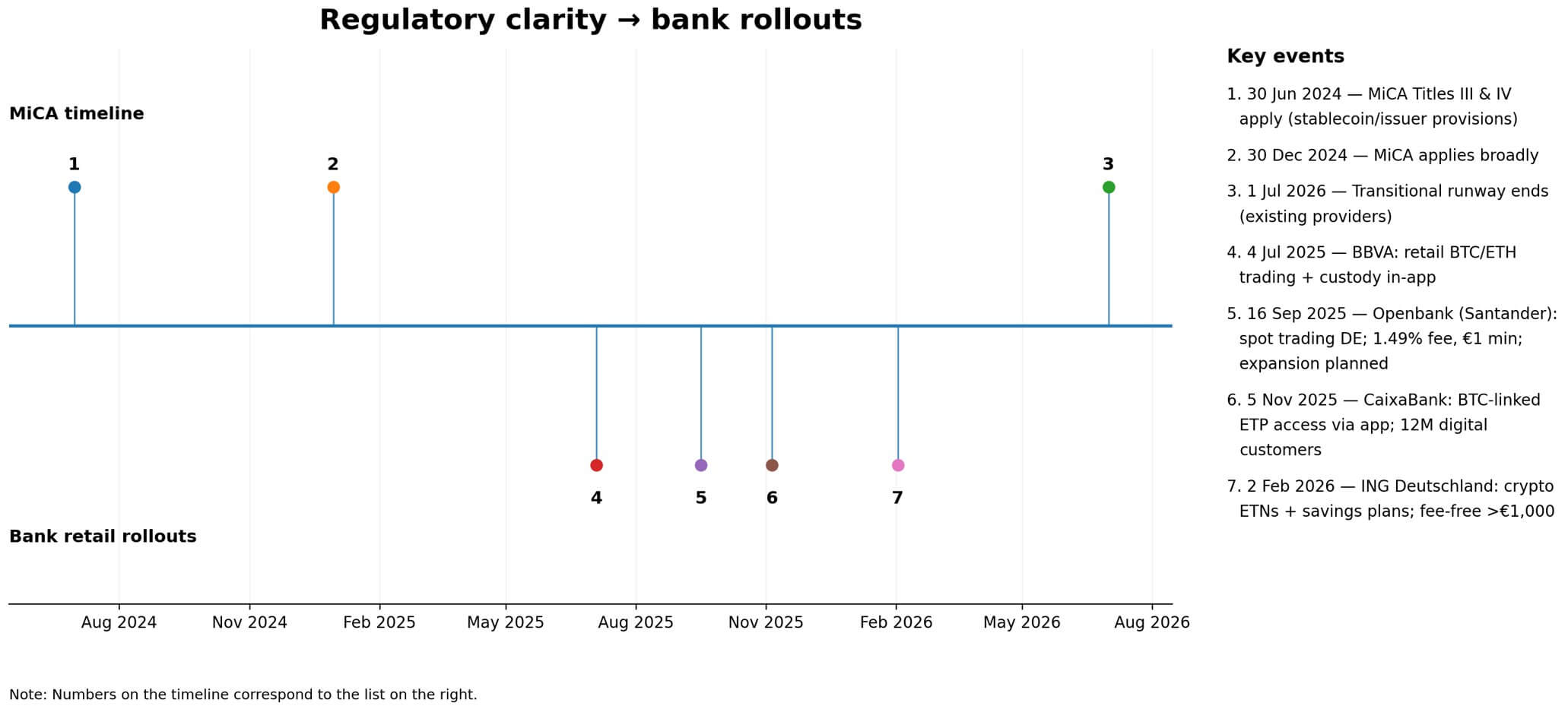

Starting Feb. 2, the bank’s 3.2 million brokerage customers can purchase crypto exchange-traded notes with zero order fees above €1,000 and set up automatic savings plans.

According to the announcement, there are no exchange signups or wallet management requirements, just another checkbox in the same app where they buy equities.

VanEck is supplying 11 crypto ETNs to the channel, covering Bitcoin, Ethereum, and several altcoins.

The move matters less because a major bank has decided that crypto is legitimate, and more because it plugs crypto into the distribution infrastructure that already processed 55.2 million securities transactions in 2025.

When the pipes are that wide, even modest adoption percentages translate to billions in routed assets.

The surge of interest from German banks isn’t driven by a sudden retail crypto boom. It reflects the impact of the European Union’s Markets in Crypto-Assets regulation, which removes lingering legal uncertainty and shifts competition toward distribution, pricing, and user experience.

That’s exactly where mass-market brokers can overwhelm standalone crypto platforms.

MiCA took full effect on Dec. 30, 2024, with stablecoin and issuer provisions kicking in six months earlier, and the transitional runway for existing crypto service providers runs through July 2026.

That timeline aligns with a wave of retail bank rollouts across Spain, Germany, and beyond, each treating crypto as a product category rather than a speculative frontier.

Distribution as strategy

ING’s brokerage footprint reveals why the ETN route creates leverage that other channels can’t match. The bank closed 2025 with €134.6 billion in deposit volume, up 22% year-over-year, and 3.2 million brokerage accounts, up from 2.8 million.

If crypto ETNs capture just 1% of that deposit volume, ING would route roughly €1.35 billion into crypto exposure without requiring customers to manage private keys or navigate exchange KYC.

At 3% penetration, the figure reaches €4 billion, and at 5% it approaches €7 billion.

Those aren’t predictions, but arithmetic that illustrates how behavioral inertia works in the bank’s favor. Customers already trust the interface, already hold other securities in the same account, and already understand how savings plans automate accumulation.

Crypto becomes another asset class toggle rather than a separate decision tree.

The regulatory wrapper matters because it allows banks to treat crypto exposure as any other listed security for reporting, execution, and tax purposes. That reduces operational friction and compliance ambiguity, making it easier for risk committees to approve product launches.

ING isn’t making a crypto bet, it’s making a distribution bet, and the underlying asset happens to be crypto-linked.

Europe’s on-chain activity supports the view that demand exists and is growing, even if it’s not always visible through traditional finance channels.

Chainalysis data shows European transaction volumes recovering to a monthly peak of $234 billion in December after a mid-2024 slump, with major markets processing substantial annual volumes.

Russia processed $376.3 billion, the UK $273.2 billion, Germany $219.4 billion, Ukraine $206.3 billion, and France $180.1 billion for the period from July 2024 through June 2025.

Germany’s volumes grew 54% over that span, a jump Chainalysis attributes in part to clearer implementation dynamics under MiCA. The regulation didn’t create demand, but it removed the uncertainty that was keeping institutional and retail players on the sidelines.

The rollout parade

ING isn’t pioneering, but rather joining a cohort of European banks that decided 2025 was the year to normalize crypto access for retail customers.

Spain’s BBVA launched Bitcoin and Ethereum trading and custody for all retail customers of legal age on July 4, 2025, making the service available directly through its banking app with no advisory overlay.

Customers initiate trades themselves, and the bank handles custody. Openbank, part of the Santander group, opened spot crypto trading for German customers on Sept. 16, 2025, offering Bitcoin, Ethereum, Litecoin, Polygon, and Cardano with a 1.49% trading fee and a €1 minimum, with plans to expand to Spain.

CaixaBank introduced access to two Bitcoin-linked ETPs from Invesco and WisdomTree on Nov. 5, 2025, distributing them through its digital banking platform and imagin app to a user base the bank pegs at 12 million digital banking customers.

Each rollout follows a similar pattern: crypto products get slotted into existing digital infrastructure, fees are disclosed upfront, and the bank’s compliance and custody teams handle the operational complexity.

The customer experience feels more like buying a stock or ETF than opening a Coinbase account, which lowers the barrier to adoption.

That’s the distribution advantage: banks can onboard millions of users who would never navigate an exchange independently but will click a button in an app they already use for bill payments and mortgage statements.

MiCA’s stablecoin provisions accelerated another shift that reinforces the regulated-rails thesis.

The European Securities and Markets Authority’s interim register lists 15 e-money token issuers managing 25 single-currency stablecoins, and MiCA compliance pressure has effectively excluded Tether’s USDT from EU crypto-asset service-provider contexts.

Circle’s euro-denominated stablecoin, EURC, grew 2,727% between July 2024 and June 2025, per Chainalysis, as compliant issuers filled the vacuum.

That preference for regulatory alignment is evident in both institutional and retail behavior, suggesting European users will gravitate toward products and platforms that operate within the MiCA framework rather than challenge it.

Flows stay sticky

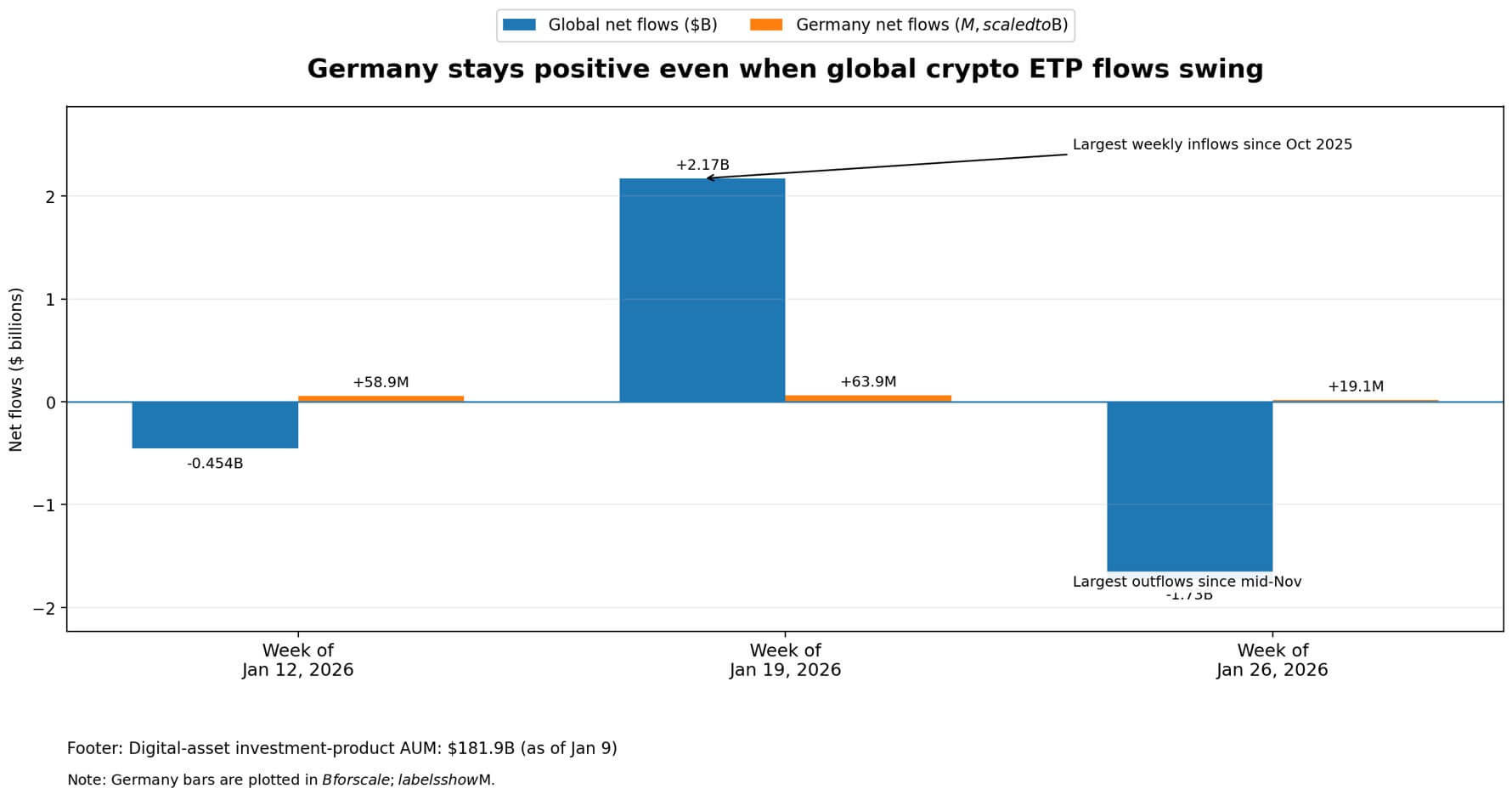

CoinShares‘ weekly investment product flow data provides a real-time proxy for demand, and the tape shows that German flows often move independently of global trends, supporting the view that regulated distribution channels drive stickier adoption.

The week of Jan. 19, 2026, saw $2.17 billion in global inflows, the largest weekly total since October 2025, with Germany contributing $63.9 million.

The following week brought $1.73 billion in outflows, the largest since mid-November, yet Germany still posted $19.1 million in inflows. The week of Jan. 12 saw $454 million in global outflows, but Germany recorded $58.9 million in inflows.

That pattern of positive or less-negative flows during risk-off periods suggests a different investor base than the one driving US ETF volatility. Brokerage-mediated exposure, especially when packaged as savings plans, tends to be stickier because it’s often automated and less reactive to short-term price swings.

Digital asset investment product assets under management stood at $181.9 billion as of Jan. 9, according to CoinShares, which includes both ETFs and ETNs globally.

The weekly flow swings between multi-billion inflows and outflows illustrate that macro sensitivity remains high. Still, the German inflow resilience suggests that regulated rail adoption could smooth some of that volatility as distribution broadens.

If ING’s launch converts even a fraction of its depot base into recurring crypto buyers through savings plans, it adds a layer of structural demand that doesn’t depend on price momentum or influencer narratives.

What’s at stake

The ING rollout and the broader European bank parade aren’t about whether crypto is “going mainstream,” since that framing assumes crypto was ever separate from mainstream finance.

The real question is who controls the on-ramps and whether those on-ramps favor self-custody platforms or regulated intermediaries.

MiCA tilts the playing field toward the latter by making compliance predictable and by giving banks a clear path to offer crypto products without navigating a patchwork of national rules.

That doesn’t kill decentralized exchanges or self-custody wallets, but it does mean the default path for most retail users will run through institutions they already bank with.

If ING’s 3.2 million brokerage customers adopt crypto ETNs at rates comparable to those for other asset classes, the bank could route billions into crypto exposure with minimal marketing spend, since the distribution lever is already in place.

Multiply that across BBVA, Openbank, CaixaBank, and the next wave of banks likely to follow, and Europe’s regulated rails start to look like the highest-volume channel for retail crypto adoption.

This isn’t because Europeans love crypto more than Americans do, it’s because European regulation made it easier for banks to operate.

The pipes are live, the fees are competitive, and the interface is familiar. What happens next depends less on crypto’s narrative and more on whether banks can convert deposit relationships into asset allocation defaults.