2026-01-29 21:20:00

Visa beat Q1 expectations as resilient payment volumes and strong cross-border growth offset a maturing global spending cycle.

Summary:

-

Visa beat expectations on earnings and revenue, driven by resilient global payment activity.

-

Cross-border volumes rose strongly, highlighting continued recovery in travel and international spending.

-

Payment volumes and processed transactions broadly met or slightly trailed consensus but remained solid.

-

Management flagged continued cost discipline while guiding to low double-digit expense growth for FY2026.

-

Results reinforce Visa’s steady-growth profile despite mixed macro signals

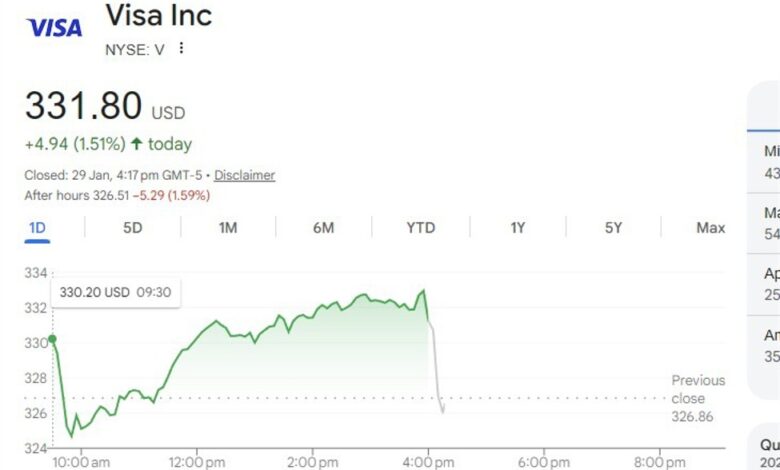

Visa delivered a solid set of first-quarter FY2026 results, comfortably beating earnings and revenue expectations as global electronic payment activity remained resilient.

Adjusted earnings per share came in at $3.17, ahead of market forecasts, while revenue rose to $10.90 billion, also exceeding consensus estimates. The performance was underpinned by steady consumer spending trends and ongoing expansion in digital payments across regions.

Total payment volume reached $3.87 trillion, slightly above expectations, reflecting continued growth in everyday card usage. Processed transactions totaled 69.4 billion, broadly in line with estimates, suggesting volumes remain healthy even as growth normalises from earlier post-pandemic surges.

A key highlight was cross-border activity. Cross-border volumes, adjusted for currency effects, rose 12% year-on-year, supported by ongoing strength in international travel, e-commerce, and cross-border services spending. The data suggests global mobility trends remain constructive despite geopolitical uncertainty and uneven economic momentum.

Looking ahead, Visa guided to low double-digit operating expense growth for the full FY2026 year. Management signalled continued investment in technology, security, and network capabilities, while maintaining discipline on costs. The outlook implies confidence in revenue growth keeping pace with investment needs, preserving margins over the medium term.

Overall, the results reinforce Visa’s positioning as a high-quality global payments franchise with durable cash-flow generation. While transaction growth has moderated from peak levels, underlying trends in digital adoption and cross-border activity continue to provide structural support for earnings growth.