Why Metaplanet is the only Bitcoin treasury surviving a brutal market shift that left Strategy investors totally exposed

Vanguard increased its position in Metaplanet from 14.12 million shares at the end of November to 15.64 million shares by Dec. 31, an 11% jump that sent speculation rippling through Bitcoin (BTC) treasury circles.

The move arrived at a moment when digital asset treasury companies had spent months nursing underwater positions and watching their market valuations compress below the value of their crypto holdings.

For those tracking the sector, the question became immediate: Is Vanguard betting that the DAT playbook works again, or is this just index mechanics doing what index mechanics do?

The reality is less dramatic than the framing suggests.

Vanguard Total International Stock Index Fund Investor Shares (VGTSX) held $573.7 billion in assets under management as of Dec. 31. Metaplanet now represents $40 million of that total, less than 0.01% of the fund.

VGTSX tracks the FTSE Global All Cap ex US Index, which means positions appear, expand, or contract mechanically in response to index reconstitutions, market cap drift, corporate actions, and fund flows.

Metaplanet’s inclusion and subsequent position increase likely reflect the company’s rising market capitalization and its growing weight within the index, not an active directional call by Vanguard on Bitcoin treasuries as an asset class.

That clarification matters because it reframes the question. The relevant inquiry isn’t whether Vanguard endorses the DAT thesis, as it doesn’t, but whether the underlying fundamentals that drive DAT valuations have shifted enough to justify renewed optimism.

The answer requires examining how the largest Bitcoin treasury operators are trading today, whether their market-to-net-asset-value ratios have re-expanded into premium territory, and whether they’re still accumulating Bitcoin at a pace that validates the equity-issuance flywheel that powered the sector’s ascent.

Premium regime vs repair mode

Market-to-net-asset-value (mNAV) serves as the primary lens for evaluating DAT health.

When mNAV trades above 1, equity is worth more than the underlying Bitcoin, enabling companies to issue shares, buy Bitcoin, and accrete value to existing holders even after dilution.

When mNAV falls below 1, the mechanism breaks. Issuing equity to buy Bitcoin destroys per-share value, and the playbook shifts toward capital preservation, buybacks, or slower accumulation.

CoinGecko’s crypto treasuries data, which calculates mNAV as enterprise value divided by the current market value of crypto holdings, provides a consistent cross-company snapshot.

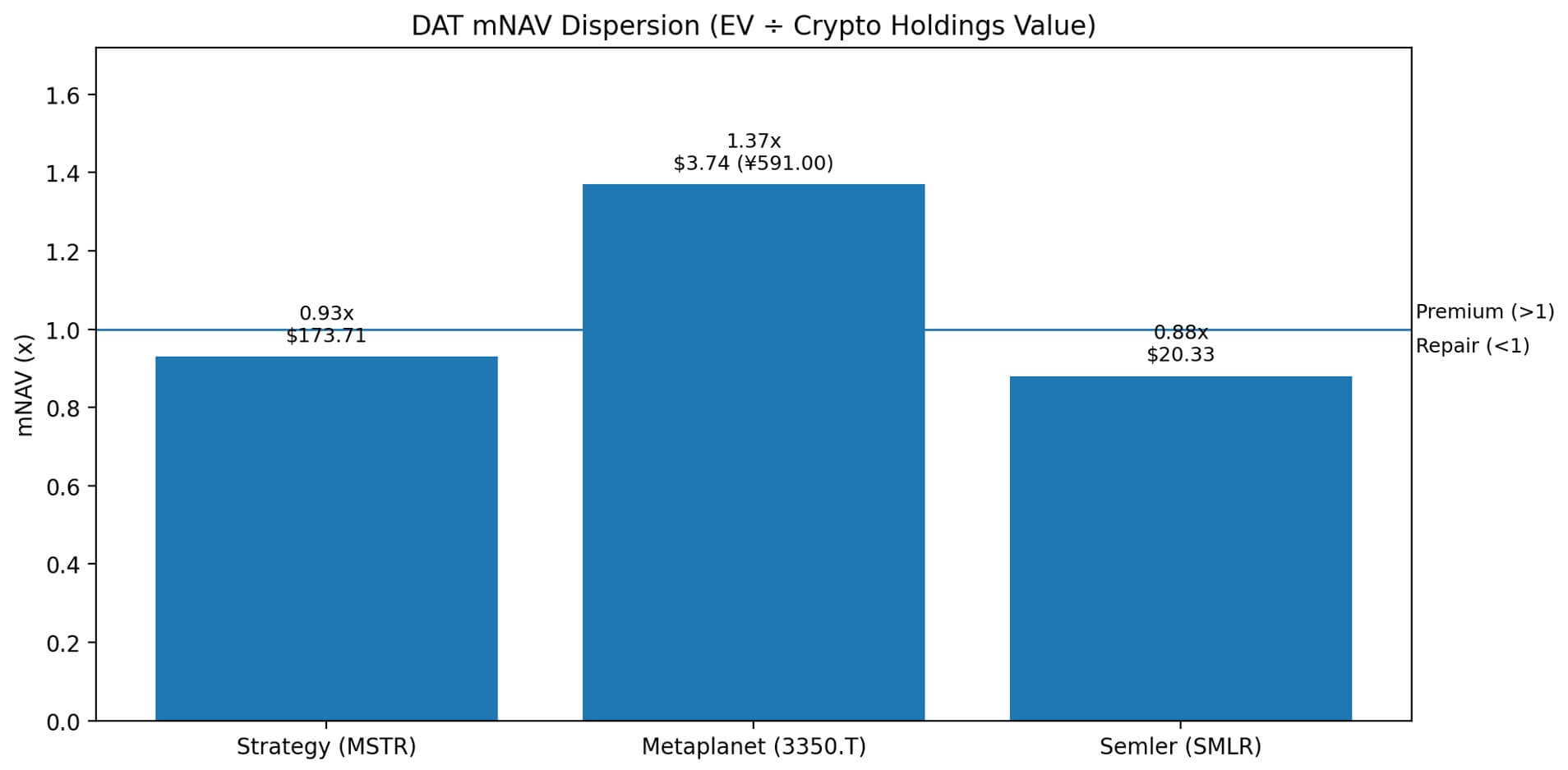

As of mid-January, the largest Bitcoin treasury operators show sharp dispersion rather than coordinated strength.

Strategy (MSTR), the sector’s flagship operator with 687,410 BTC, trades at $173.71 per share with an mNAV of 0.93x. The company added 13,627 BTC on Jan. 12 and another 1,283 BTC on Jan. 5, signaling continued accumulation despite trading below net asset value.

That positioning reflects a bet that the discount will close, but it also means that near-term equity issuance will be dilutive unless the stock re-rates higher.

Metaplanet (3350.T), the Japanese operator now attracting attention due to Vanguard’s index position, trades at ¥591 ($3.74) with an mNAV of 1.37x. The company holds 35,102 BTC and last disclosed a purchase of 4,279 BTC on Dec. 30.

That premium mNAV places Metaplanet in a fundamentally different regime than Strategy: equity issuance remains accretive, and the company retains the ability to expand its treasury without penalizing existing shareholders.

Semler Scientific (SMLR), a smaller operator holding 5,048 BTC, trades at $20.33 with an mNAV of 0.88x. The company’s most recent visible transaction on CoinGecko dates to Oct. 3, and the absence of January purchases suggests a shift toward capital discipline while the stock trades at a discount.

The pattern is clear: Metaplanet operates in premium territory, while Strategy and Semler remain in repair mode. That bifurcation complicates any claim that “DATs are back” unless the thesis hinges entirely on a single Japanese operator rather than sector-wide re-rating.

Why mNAV dispersion matters more than individual moves

The divergence between Metaplanet’s premium and Strategy’s discount reflects different market perceptions of execution risk, regulatory exposure, and the credibility of each company’s accumulation strategy.

Metaplanet benefits from operating outside the US regulatory jurisdiction and from a relatively clean narrative as a pure-play Bitcoin treasury without the operational complexity of Strategy’s convertible debt stack.

Strategy, despite aggressive accumulation and a well-established playbook, trades at a discount that suggests the market remains skeptical about near-term catalysts or is pricing in dilution risk from future equity raises.

That dispersion also exposes the limits of treating DATs as a homogeneous asset class.

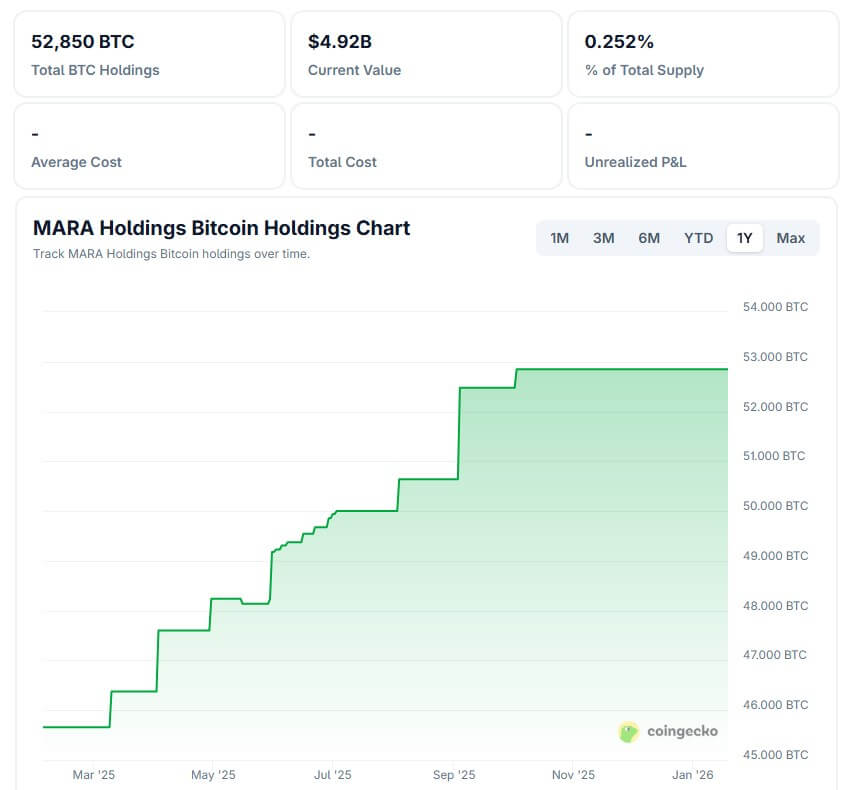

MARA Holdings, a Bitcoin miner with treasury operations, holds 52,850 BTC and trades at an mNAV of 1.44x, reflecting a different valuation dynamic tied to mining economics and operational leverage.

Coinbase, often cited alongside treasury operators, trades at an mNAV of 34.65x. This number reveals why operating businesses with revenue streams unrelated to Bitcoin holdings should not be evaluated using DAT frameworks.

The cleanest read on whether the sector is recovering requires tracking month-over-month mNAV trends across the largest pure-play operators.

If Strategy, Metaplanet, and Semler all show rising mNAVs over the past three months, the case for a regime shift strengthens. If only Metaplanet is re-rating while others remain flat or compressed, the story is narrower: one company executing well in a favorable jurisdiction, not a sector-wide revival.

The flywheel only works when equity trades are rich

Late last year, analysts flagged Bitcoin treasury stocks as distressed assets, with late entrants trapped underwater as their cost bases climbed above $100,000 per Bitcoin while spot prices pulled back.

The core tension hasn’t disappeared: when mNAV falls below 1, the accretive-dilution thesis collapses. Issuing equity to buy Bitcoin at a discount to NAV destroys value for existing holders, rendering the entire model inoperable until the stock re-rates.

Strategy’s continued accumulation despite a sub-1 mNAV suggests the company is either betting on a near-term stock recovery or prioritizing Bitcoin accumulation as a long-term positioning move, regardless of short-term dilution.

Metaplanet’s premium mNAV enables it to maintain the flywheel without those trade-offs, which explains why the company remains active in the market.

The absence of recent Semler purchases aligns with rational capital allocation under discount conditions. When equity trades at 0.88x net asset value, buying more Bitcoin with dilutive equity makes shareholders poorer on a per-share basis.

The logical response is to pause accumulation, focus on operational efficiency, or explore buybacks if liquidity permits.

What would confirm “DATs are back”

A credible claim that digital asset treasuries have returned to form requires three conditions: broad-based mNAV expansion across multiple operators, sustained Bitcoin accumulation at accretive valuations, and evidence that equity markets are rewarding the model rather than penalizing it.

Right now, only one of those conditions holds, and it applies only to a subset of the sector.

Metaplanet’s premium mNAV and Vanguard’s mechanically driven position increase demonstrate that pockets of strength exist, particularly among operators outside the US jurisdiction with clean balance sheets and disciplined execution.

But Strategy’s discount and Semler’s accumulation pause indicate that the broader market remains unconvinced, at least at current Bitcoin prices and equity valuations.

The sector isn’t back, but bifurcated. Outcomes increasingly tied to company-specific execution rather than rising tides lifting all boats.