SEC Chair predicts 2-year timeline to put US fully on chain but the real $12.6 trillion opportunity isn’t equities

SEC Chair Paul Atkins told Fox Business in December that he expects US financial markets to move on-chain “in a couple of years.” The statement landed somewhere between prophecy and policy directive, especially coming from the architect of “Project Crypto,” the Commission’s formal initiative to enable tokenized market infrastructure.

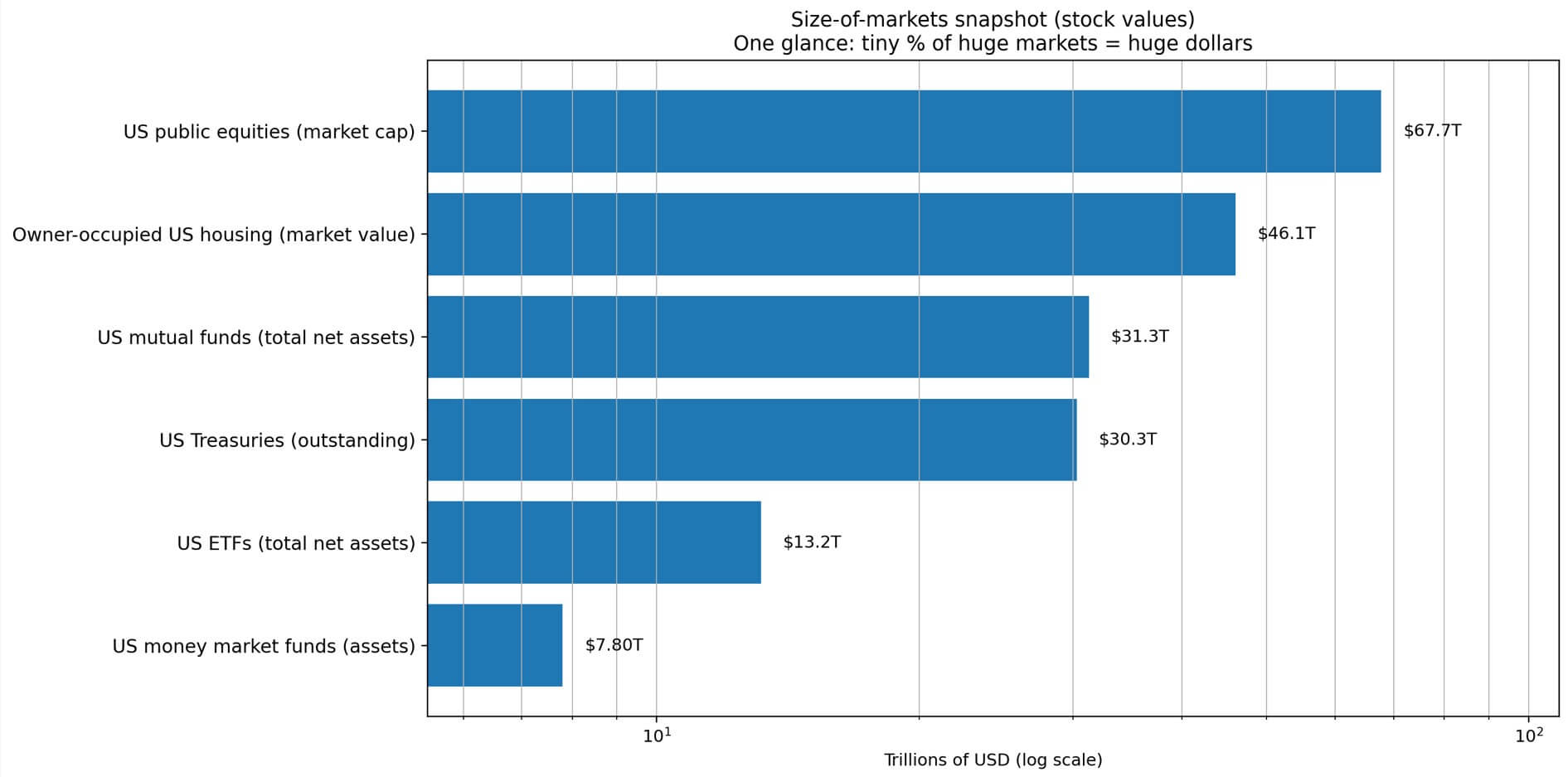

However, what does “on-chain” mean when applied to $67.7 trillion in public equities, $30.3 trillion in Treasuries, and $12.6 trillion in daily repo exposures? And which parts can realistically move first?

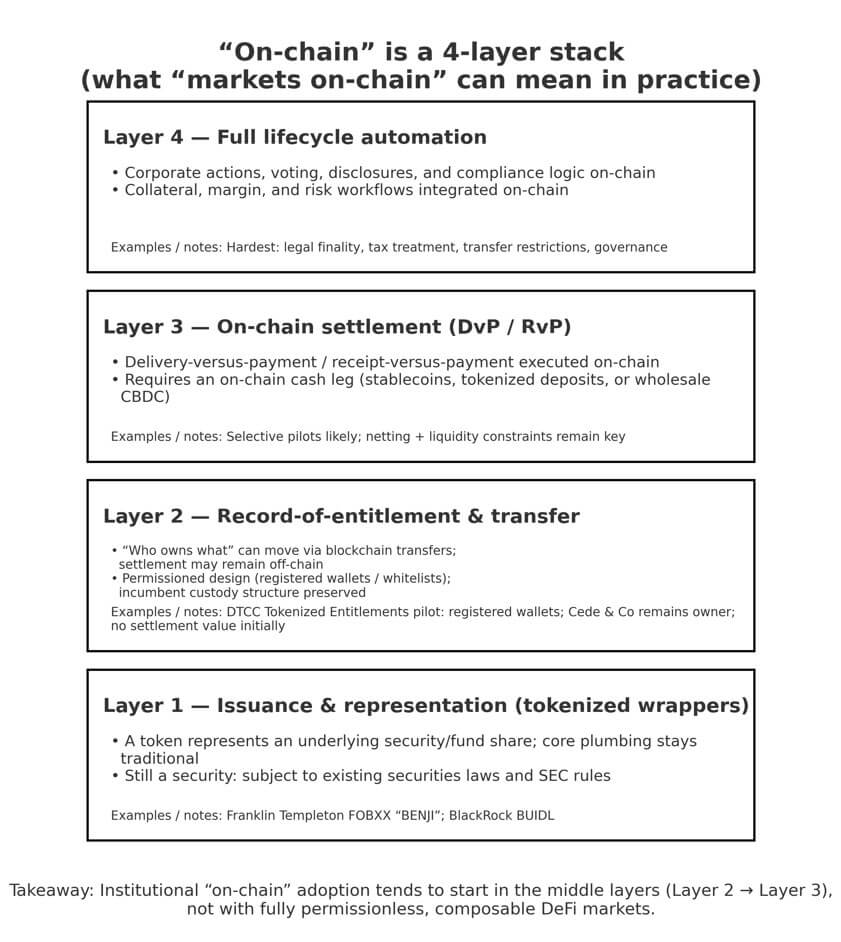

The answer requires precision. “On-chain” isn’t a single thing: it is a four-layer stack, and most of what Atkins described sits in the middle layers, not the DeFi-native endpoints that crypto Twitter imagines.

Four flavors of on-chain

The gap between tokenized wrappers and full lifecycle automation determines what’s plausible in two years versus two decades, so definition matters.

Layer one is issuance and representation: a token stands in for an underlying security, but the plumbing stays traditional. Think digitized share certificates. Atkins explicitly frames tokenization as smart contracts representing securities that remain subject to SEC rules, rather than as parallel asset classes.

Layer two is record-of-entitlement and transfer: the “who owns what” ledger moves via blockchain, but settlement still happens through incumbent clearinghouses. DTCC’s Dec. 11 no-action letter from the SEC Trading & Markets authorizes exactly this model.

The Depository Trust Company can now issue “Tokenized Entitlements” to participants via approved blockchains. However, the offer applies only to registered wallets. Cede & Co. remains the legal owner, and no initial collateral or settlement value is assigned.

Translation: on-chain custody and 24/7 transfer without replacing NSCC netting tomorrow.

Layer three requires on-chain settlement with an on-chain cash leg, consisting of delivery-versus-payment using stablecoins, tokenized deposits, or wholesale central bank digital currency. Atkins discussed DvP and the theoretical possibility of T+0, but he also acknowledged that netting is the core of clearinghouse design.

Real-time gross settlement changes liquidity needs, margin models, and intraday credit lines. That’s harder than a software upgrade.

Layer four is a full lifecycle on-chain solution that covers corporate actions, voting, disclosures, collateral posting, and margin calls, executed via smart contracts. This is the final state that touches governance, legal finality, tax treatment, and transfer restrictions.

It’s also the furthest from current SEC authority and market-structure incentives.

Atkins’ two-year timeline maps most cleanly to layers two and three, not a wholesale migration to composable DeFi markets.

Sizing the addressable universe

The prize is enormous, even if adoption starts small, because tiny percentages of giant markets are giant.

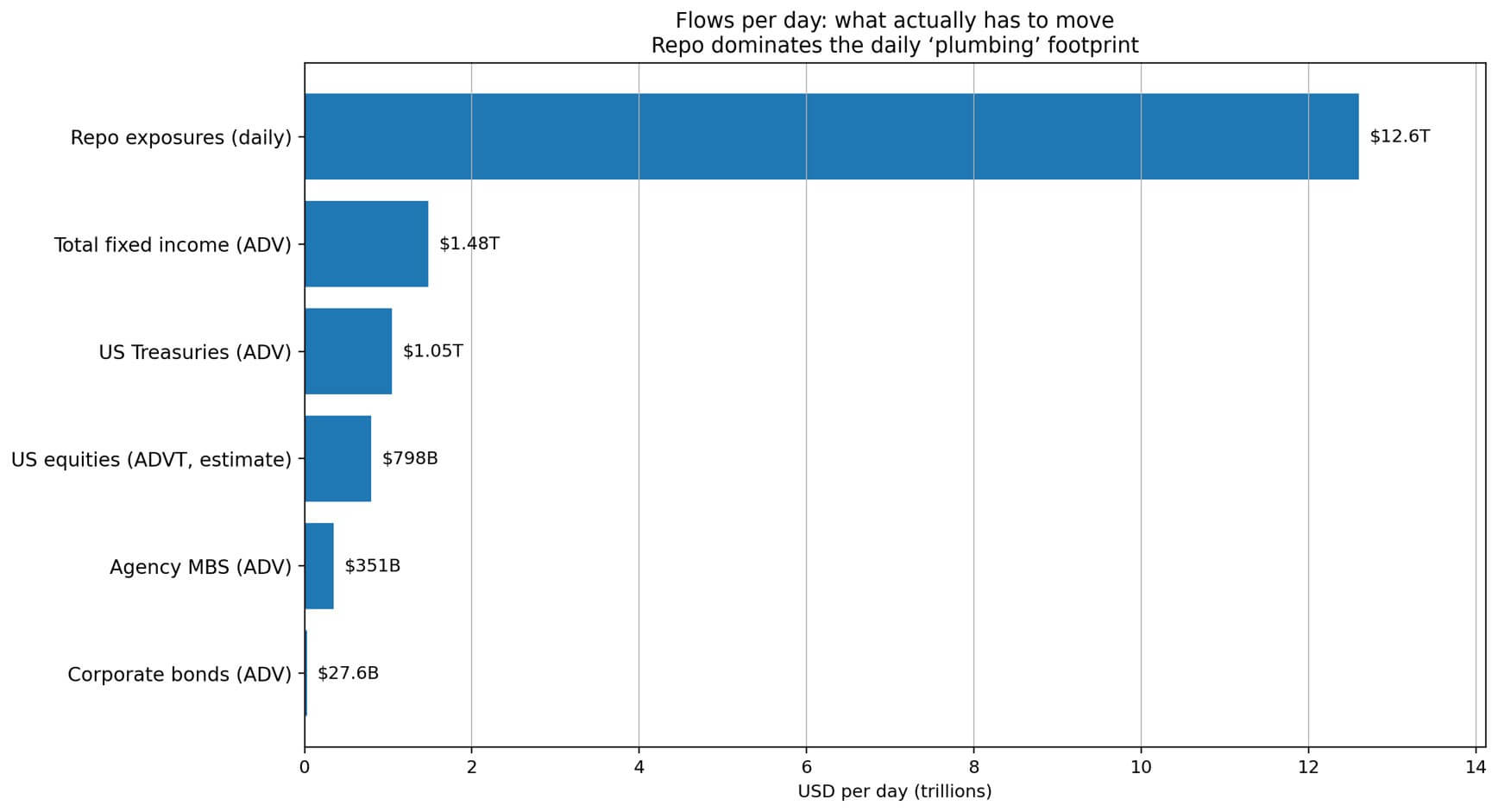

US public equities carried a market cap of $67.7 trillion at the end of 2025, per SIFMA. Trading intensity averaged 17.6 billion shares per day in 2025, with an estimated average daily trading value of around $798 billion.

One percent of the equity market cap, converted to tokenized entitlements, equals $677 billion. Half a percent of daily trading value equals $4 billion in gross settlement throughput per day, assuming blockchain could eliminate the netting that currently collapses billions in trades into far smaller net obligations.

Treasuries are bigger by flow. The market stands at $30.3 trillion in outstanding volume as of the third quarter of 2025, with an average daily trading volume of $1.047 trillion.

Yet the real monster is repo: the Office of Financial Research estimates average daily repo exposures of $12.6 trillion in the third quarter of 2025, spanning cleared, tri-party, and bilateral arrangements.

If tokenization’s pitch is de-risking settlement and improving collateral mobility, repo is where the argument becomes legible. Two percent of daily repo exposure is $252 billion, a plausible early wedge if institutions see operational and transparency wins.

Corporate credit and securitized products add another dimension.

Corporate bonds outstanding total $11.5 trillion, with an average daily trading volume of $27.6 billion. Agency mortgage-backed securities traded $351.2 billion per day in 2025, while non-agency MBS and asset-backed securities combined for another $3.74 billion daily.

Total fixed-income trading hit $1.478 trillion per day in 2025. These markets already operate through custody chains and clearing infrastructure that tokenization could streamline without regulatory surgery.

Fund shares represent a different entry point. Money market funds hold $7.8 trillion in assets as of early January 2026. Mutual funds have $31.3 trillion, and ETFs hold $13.17 trillion.

Tokenized fund shares don’t require rearchitecting clearinghouses, as they sit at the product wrapper layer. Franklin Templeton’s FOBXX positions itself as an on-chain money fund, BlackRock’s BUIDL reached nearly $3 billion in assets last year.

Tokenized Treasuries tracked by RWA.xyz total $9.25 billion, making them a leading on-chain real-world asset category.

Real estate splits into two categories. Owner-occupied US housing carried a market value of $46.09 trillion in the third quarter of 2025. Still, county deed registries won’t tokenize at scale in two years, as property law and administrative reality move slower than software.

The financialized slice, consisting of REITs, mortgage securities, and securitized real estate exposure, already lives in the securities plumbing and can move earlier.

What moves first: a ladder of regulatory friction

Not all on-chain adoption faces the same level of resistance. The path of least friction starts with products that behave like cash and ends with registries embedded in local government administration.

Tokenized cash products and short-dated bills are already happening.

Tokenized Treasuries at $9.25 billion represent meaningful scale relative to other real-world assets on-chain. If distribution expands through broker-dealer and custody channels, a five-to-twenty-times expansion over two years, from $40 billion to $180 billion, becomes plausible, especially as stablecoin settlement infrastructure matures.

Collateral mobility follows close behind. Repo’s $12.6 trillion daily footprint makes it the most credible target for tokenization’s delivery-versus-payment pitch.

Even if only 0.5% to 2% of repo exposures shift to on-chain representation, that’s $63 billion to $252 billion in transactions where tokenized collateral reduces settlement risk and operational overhead.

The next step is permissioned transfer of mainstream securities entitlements.

DTCC’s pilot authorizes tokenized entitlements for Russell 1000 equities, Treasuries, and major-index ETFs, held via registered wallets on approved blockchains.

If participants treat this as a balance sheet and operations upgrade, such as 24/7 movement, programmable transfer logic, and better transparency, 0.1% to 1% of the US equity market cap could become “on-chain eligible entitlements” within two years. That’s $67.7 billion to $677 billion in tokenized claims, even before settlement value gets assigned.

Equities settlement and netting redesign sit higher on the friction ladder. Moving to T+0 or real-time gross settlement changes liquidity requirements, margin calculations, and intraday credit exposure.

Central counterparty clearing exists because netting reduces the amount of cash that must move.

Eliminating netting means either finding new sources of intraday liquidity or accepting that gross settlement applies only to a subset of flows.

Private credit and private markets carry a considerable notional value, with estimates ranging from $1.7 trillion to $2.28 trillion. Yet, transfer restrictions, servicing complexity, and bespoke deal terms make them slower to standardize.

Tokenization helps with fractional ownership and secondary liquidity, but regulatory clarity around exemptions and custody models still lags.

Real-world registries rank last. Tokenizing a property deed doesn’t exempt it from local recording statutes or title insurance requirements. Even if the financial exposure moves on-chain through securitization, the legal infrastructure supporting ownership claims won’t.

Smaller than the hype, larger than zero

Most tokenized securities will be on-chain but not open to the public.

DTCC’s pilot model is permissioned even on public blockchains, with registered wallets, allowlisted participants, and institutional custody. That’s still “on-chain” in the transparency and operational efficiency sense Atkins described. It’s just not “anyone can provide liquidity.”

The DeFi-addressable wedge is biggest where the asset already behaves like cash.

Tokenized bills and money market fund shares are already collateral in crypto market infrastructure, and BlackRock’s BUIDL is a visible example.

Stablecoins provide the bridging layer, with a $308 billion supply, serving as the on-chain settlement asset base that makes delivery-versus-payment plausible without a wholesale CBDC. Before stocks go on-chain, dollars did.

A concrete way to size this: using tokenized cash products as the starting numerator, applying haircuts for transfer restrictions and custody models, and estimating the fraction that can interact with smart contracts.

If tokenized Treasuries and money market fund products reach $100 billion to $200 billion, and 20% to 50% can be posted into permissioned or semi-permissioned smart contracts, that implies $20 billion to $100 billion of plausible on-chain collateral.

This is enough to matter for repo workflows, margin posting, and institutional DeFi.

What this means in practice

Atkins didn’t offer a detailed roadmap, but the pieces are visible.

The SEC granted DTCC a no-action letter in December 2025 to pilot tokenized entitlements. Tokenized Treasuries and money market funds are scaling. Stablecoin supply provides an on-chain cash layer. Repo markets dwarf equities by daily flow, and collateral mobility is where tokenization’s risk-reduction argument is strongest.

The two-year timeline isn’t about every security moving to Ethereum. It’s about critical mass in the middle layers: layer two entitlements that live on-chain but settle through familiar infrastructure, and layer three experiments where delivery-versus-payment happens on-chain for specific asset classes and counterparties.

Even at 1% adoption across Treasuries, money market funds, and equities entitlements, that’s over a trillion dollars in on-chain representation.

The US isn’t alone. The UK opened a Digital Securities Sandbox. Hong Kong issued HK$10 billion in digital green bonds. The EU’s DLT Pilot Regime establishes a framework for regulated experimentation in issuance, trading, and settlement on distributed ledgers.

This is a global market-infrastructure modernization cycle, not a speculative overhang.

DTCC’s quarterly metrics on tokenized entitlements, such as total value, daily transfers, registered wallets, and approved chains, are useful for tracking.

The same applies to repo transparency data from the Office of Financial Research, tokenized Treasury and money market fund assets under management, and stablecoin supply as a proxy for settlement capacity.

Those numbers will show whether “on-chain in a couple of years” was policy or aspiration.