2026-01-08 22:12:00

Since the November ISM PMI reports painted a mixed picture of the U.S. economy, market watchers looked ahead to the December figures to hopefully gain more clarity.

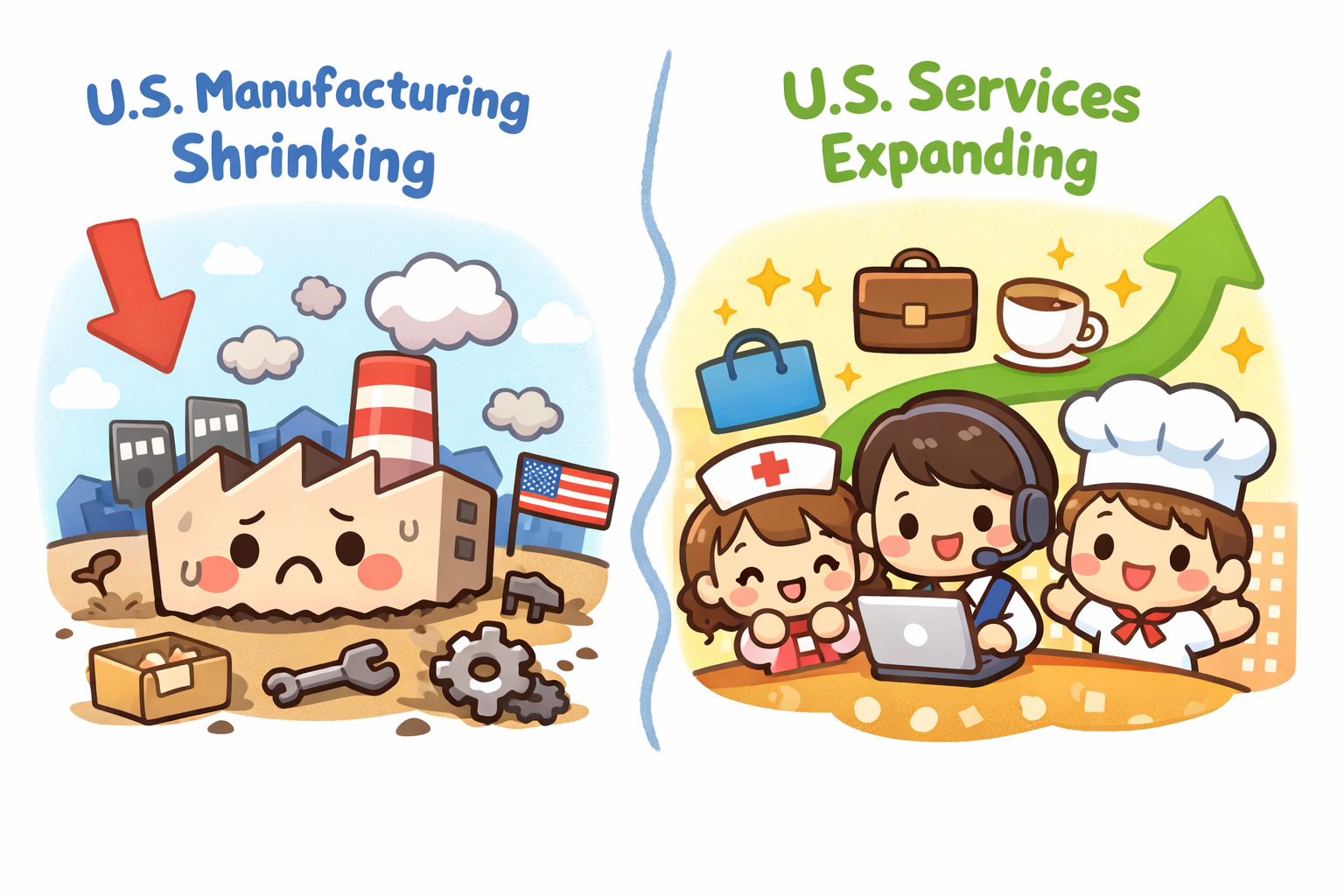

Instead, the latest batch of PMI readings further highlighted the diverging performance of the manufacturing and services sectors, giving an even more muddled outlook for U.S. recession odds and the Fed policy trajectory.

As it turns out, manufacturing is still struggling as factories keep contracting month after month. Meanwhile, the services sector (think restaurants, healthcare, financial firms) just posted its strongest reading in over a year.

So which is it? Is the economy on the brink of recession, or cruising along just fine?

The answer lies in understanding what December’s ISM surveys really tell us about where the economy is headed, what it means for recession odds, and how it could shape the Federal Reserve’s next moves

The Basics: What Are ISM Surveys?

Every month, the Institute for Supply Management asks hundreds of purchasing managers (a.k.a. the people who actually buy stuff for companies) a straightforward question: Are business conditions getting better, worse, or staying the same?

Their answers get compiled into two key numbers:

ISM Manufacturing PMI: Surveys over 400 industrial companies about production, new orders, employment, and inventory levels.

ISM Services PMI: Surveys companies across finance, healthcare, retail, hospitality, and other service industries—sectors that make up nearly 80% of the US economy.

The magic number is 50. Above 50 means the sector is expanding. Below 50 means it’s contracting.

December’s Numbers: Split Personality Economy

Here’s what the December surveys showed:

Manufacturing PMI: 47.9 (down from 48.2 in November)

- 10th consecutive month in contraction territory

- New orders at 47.7 (still contracting but improving slightly)

- Employment at 44.9 (weak but better than November)

- Production at 51 (actually expanding, one of few bright spots)

Services PMI: 54.4 (up from 52.6 in November)

- Highest reading since June 2024

- New orders jumped to 57.9 (strong growth)

- Business activity at 56 (solid expansion)

- Employment at 51.4 (modest growth)

Why It Matters: The Economy’s Balancing Act

Here’s the critical thing to remember: Manufacturing only represents about 11% of the US economy while services account for nearly 80%.

Think of it this way: If 10 factories are struggling but 80 restaurants, hospitals, banks, and tech companies are thriving, the overall economy can still be in decent shape. That’s basically where the U.S. economy is at now.

But there’s a catch. Manufacturing has historically been a leading indicator, as it tends to warn about broader economic troubles before they hit. Factory orders dry up first, then the weakness spreads. Every U.S. recession since 1948 has featured a contracting manufacturing sector.

The Recession Math

So is the U.S. economy really headed for a recession? The data is genuinely mixed:

Warning signs from manufacturing:

- ISM below 50 for 10 straight months (25 out of the last 26 months)

- When manufacturing PMI stays below 42.5 for an extended period, it historically signals the overall economy is contracting

- Currently at 47.9: Not catastrophic, but still weak

- Employment in factories keeps shrinking (11 consecutive months of job cuts)

Reassuring signs from services:

- Services PMI at 54.4 shows healthy expansion

- The overall economy expands when the Services PMI is above 49

- Strong new orders suggest momentum will continue

- As long as 80% of the economy is growing, recession risk is limited

Current recession odds: Most economists put recession probability for 2026 at 30-40%. That’s elevated compared to normal times (15-20%), but not a done deal. Financial markets (based on prediction markets) show similar odds—around 25-35% chance of recession by end of 2026.

Impact on January Fed Meeting

The Federal Reserve meets January 27-28 to decide whether to cut interest rates further. Here’s why these ISM surveys matter for that decision:

The case for holding rates steady (what the Fed will likely do):

- Services sector strength means the economy isn’t falling apart

- Strong services PMI at 54.4 suggests GDP growth remains solid

- Market odds of a January rate cut: only 16% (according to CME FedWatch Tool)

- The Fed has already cut three times in 2025 (by 0.75% total)

- Current rates at 3.5-3.75% are already near “neutral” levels

The case for cutting (less likely):

- Manufacturing weakness continues unabated

- Factory employment keeps contracting

- Weak factory data could eventually spread to services

- Inflation has cooled to near the Fed’s 2% target

What to expect: The Fed will almost certainly hold rates steady at the January meeting. Fed Chair Jerome Powell has made it clear they’re in “wait and see” mode. Markets are pricing in perhaps one or two more cuts later in 2026, likely in the spring or fall, but only if economic data weakens further or inflation stays tame.

The Bottom Line

December’s ISM surveys paint a picture of an economy with a split personality. Manufacturing is clearly in a funk—10 months of contraction and counting. But the far larger services sector just posted its strongest reading in six months, suggesting the economy isn’t on the brink of collapse.

For recession watchers: The odds remain around 30-40% for 2026, which is elevated but not catastrophic. The key will be whether manufacturing weakness spreads to services, or whether services strength eventually pulls manufacturing up.

For Fed watchers: January 27-28 will almost certainly bring a “no change” decision on rates. The Fed has cut three times already and is now comfortable pausing to see how the economy evolves. Future cuts in 2026 will depend on whether employment weakens substantially or if inflation unexpectedly reheats.

What to watch next:

- January jobs report (releases early February) for signs of labor market weakening

- January inflation data (CPI on February 12) to see if progress toward 2% continues

- January ISM surveys (early February) to see if this divergence persists

- Fed decision January 28 for possible hints about March or April cuts

Remember that there are no guarantees in market behavior and outcomes, only probabilities. The split between manufacturing weakness and services strength creates genuine uncertainty about the path ahead. Be prepared for multiple scenarios, manage your risk accordingly, and don’t bet the farm on any single outcome.

Disclaimer: Trading and investing carry risk, and past performance does not guarantee future results. This article is for educational purposes only and should not be considered investment advice. Always do your own research and consider consulting with a financial advisor before making investment decisions. Seasonal patterns are observations, not predictions, and should never be the sole basis for trading decisions.

{kind=link}