2026-01-06 00:36:00

Summary:

-

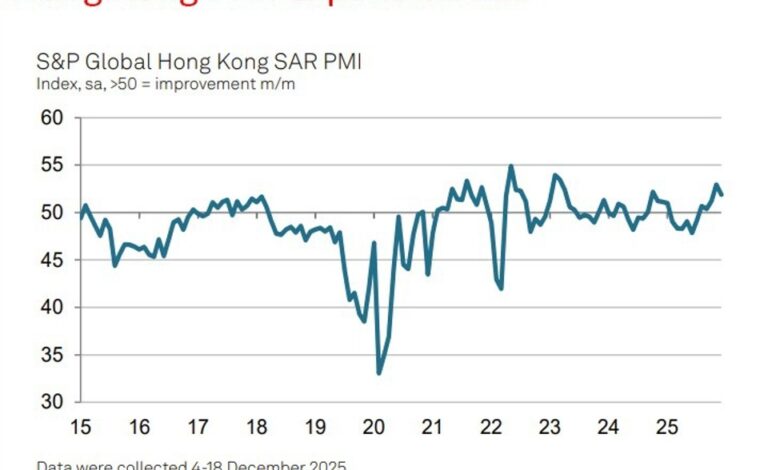

Hong Kong PMI remains in expansion for fifth month, 51.9 in December vs. 52.9 in November

-

Output and new orders grow at solid but slower pace

-

Backlogs rise for first time in a year

-

Selling prices increase at fastest rate since 2023

-

Business confidence improves into 2026

Business conditions across Hong Kong’s private sector continued to improve at the end of 2025, marking a fifth consecutive month of expansion, though momentum eased slightly as cost pressures intensified, according to the latest PMI data from S&P Global.

The headline Hong Kong SAR PMI slipped to 51.9 in December from 52.9 in November, remaining firmly above the 50 threshold that separates expansion from contraction. The reading points to a moderate but sustained improvement in business conditions and capped the strongest quarterly performance since early 2023.

Output rose for a fifth straight month, with growth easing from November but still among the strongest seen over the past three years. Firms cited continued improvements in demand conditions as the key driver, with sales increasing across both domestic and external markets. New orders also expanded at a solid pace, posting the second-strongest increase since April 2023, supported by higher customer numbers and improved client confidence. Notably, demand from mainland China and international markets contributed meaningfully to the upturn.

The sustained rise in new business began to stretch capacity. Backlogs of work increased for the first time in a year, a development often viewed as a forward-looking signal of further production gains ahead. While the accumulation of unfinished work remained modest, it was the most pronounced since November 2024, suggesting demand is increasingly testing firms’ operational limits.

Despite rising workloads, employment declined for a second consecutive month, largely due to the non-replacement of voluntary departures. At the same time, purchasing activity continued to rise, albeit at a slower pace, while input inventories increased for a seventh month. Firms also reported the first improvement in supplier delivery performance since May, reflecting more timely arrivals of inputs.

Price pressures were a standout feature of the December survey. Input costs rose at a solid pace, driven by higher raw material prices and a sharp acceleration in staff-related expenses, which increased at the fastest rate since June 2024. In response, firms raised selling prices at the quickest pace in 26 months, marking the strongest charge inflation since October 2023.

Looking ahead, sentiment improved further. While firms remained cautious about global growth and tariff risks, pessimism about the year-ahead outlook eased to its lowest level since mid-2023, underpinned by growing confidence in domestic economic conditions.

Commenting on the data, Usamah Bhatti, Economist at S&P Global Market Intelligence, said rising backlogs point to potential further output gains, while easing pessimism suggests the recovery has gained firmer footing into 2026.