Ripple has lastly completed its authorized battle in opposition to the US Securities and Change Fee, bringing authorized readability to its underlying coin, XRP (XRP). Now observers are asking whether or not XRP can lastly concentrate on offering a viable various to SWIFT.

The Society for Worldwide Interbank Monetary Telecommunication (SWIFT) has been the spine of worldwide cash transfers since its founding in 1973. Nonetheless, for a number of years, critics have mentioned that the system is outdated.

Many within the blockchain trade, together with Ripple CEO Brad Garlinghouse, argue that blockchain expertise offers larger throughput and higher transparency, making it a superior various to SWIFT.

Now that Ripple’s authorized battles have calmed down, can it present an affordable various to SWIFT?

How does Ripple stack as much as SWIFT?

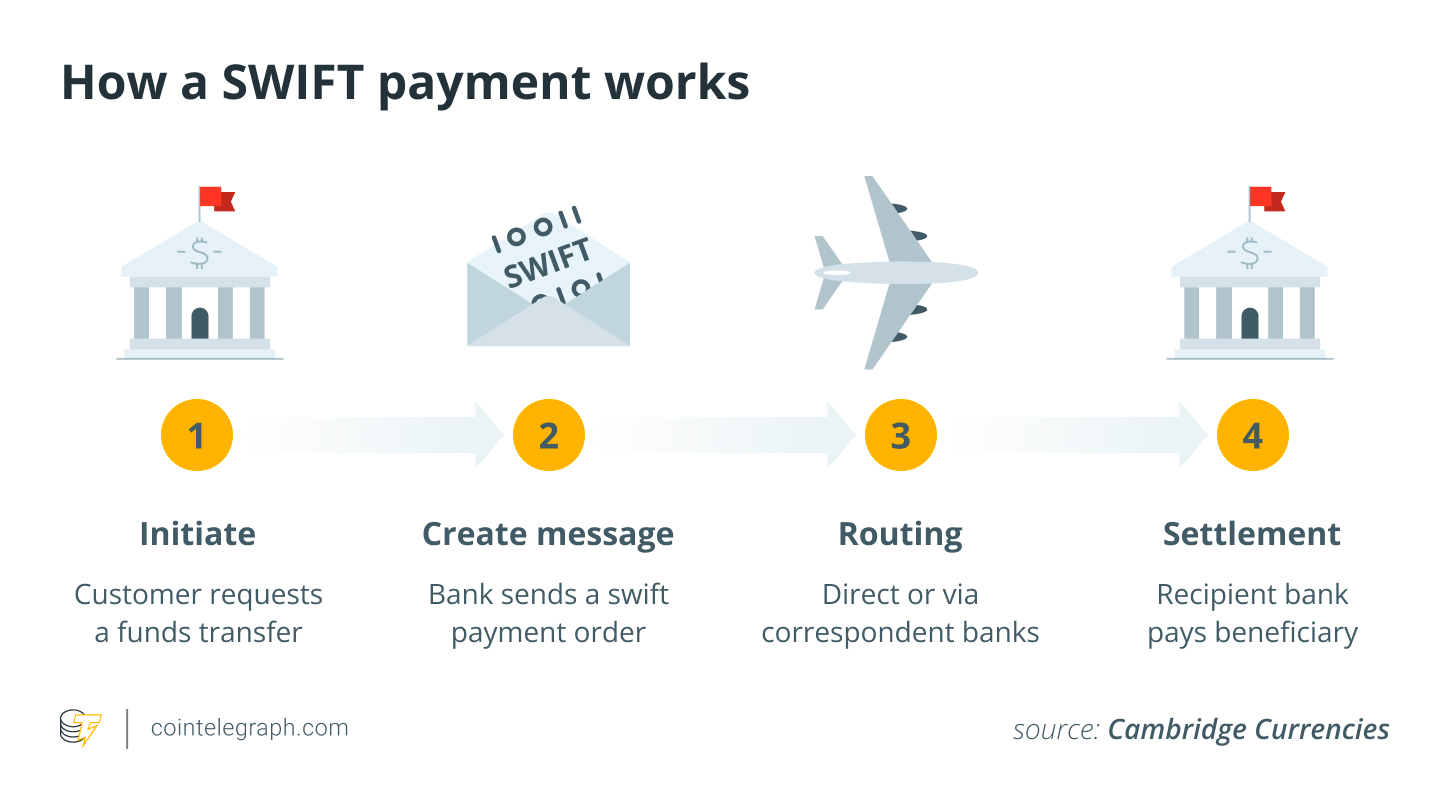

Over 50 years in the past, SWIFT changed Telex because the coding system underpinning worldwide monetary transactions. The system doesn’t ship cash itself however reasonably offers standardized codes and a safe messaging platform via which banks can coordinate cash transfers.

A buyer will make a cash switch request. Their financial institution will then ship the request to the recipient financial institution, and that request could undergo a number of different banks within the community. Precise settlement occurs via established banking relationships and clearing programs.

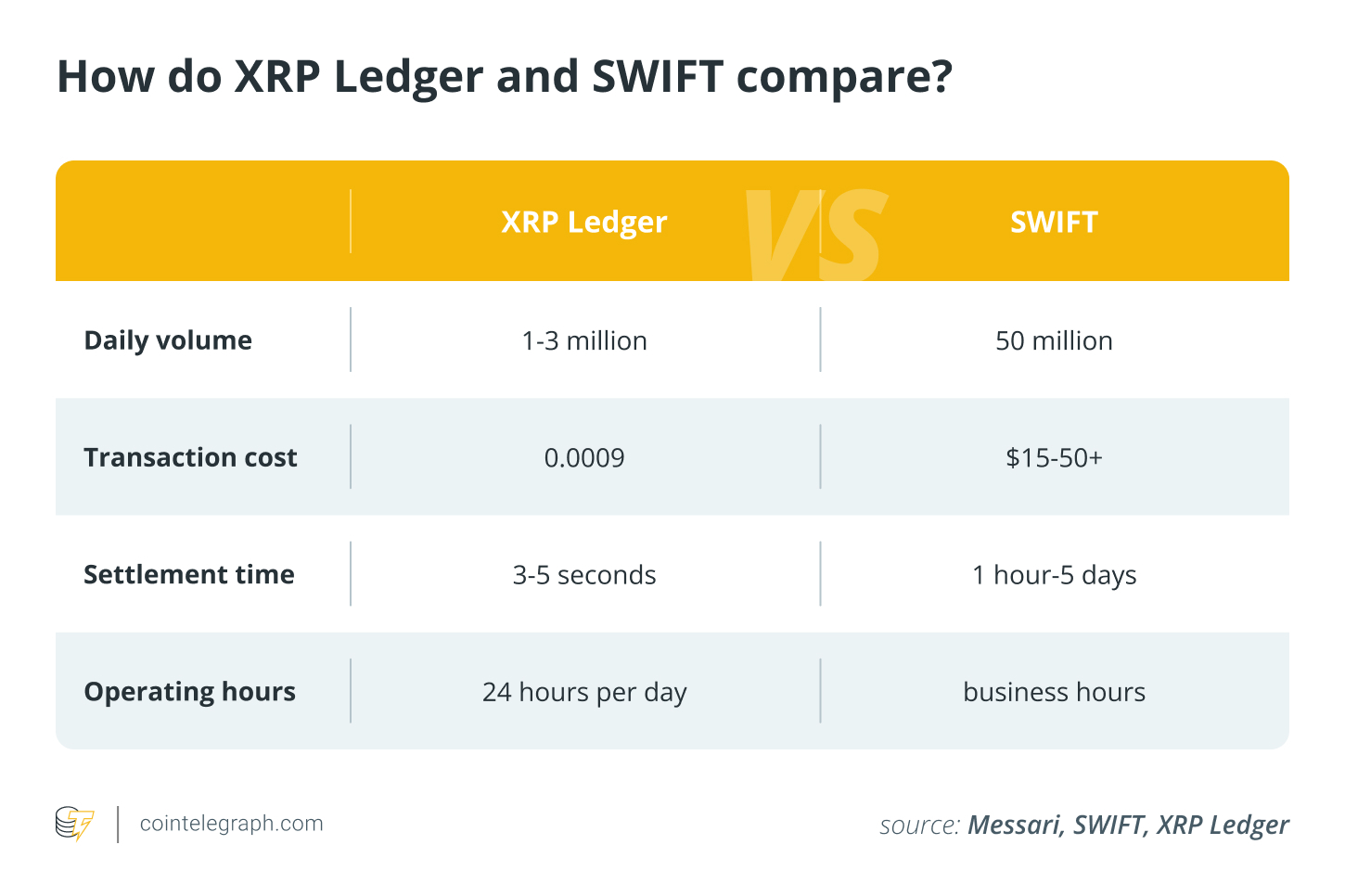

SWIFT processes over 53 million messages day by day throughout 40,000 cost routes, 220 nations and over 11,500 establishments.

However there are some main complaints with SWIFT. Transactions can take a number of days and are rife with charges. Moreover, the complicated community of financial institution companions means it’s tougher to make sure visibility.

There are additionally delays and failures. SWIFT mentioned in January 2024 that one in 10 transactions fails, whereas one in 20 settles late.

The community has undergone a lot of upgrades since its inception, together with .

ISO 20022, which goals to offer clearer cost information and extra transparency by Nov. 25, 2025. Nonetheless, critics declare it’s in the end outdated “legacy” tech operating on decades-old XML expertise.

SWIFT could have the benefit of ubiquity and clear institutional adoption, however Ripple gives a transparent benefit in technological phrases, with sooner transaction and settlement speeds, in addition to decrease prices.

In 2018, simply a few years earlier than Ripple’s years-long authorized battle with the SEC would start, Garlinghouse informed Bloomberg, “What we’re doing and executing on a day-by-day foundation is, actually, taking up SWIFT” as banks and remittance firms signed on to make use of XRP Ledger.

So, with institutional companions signing on and the XRP worth on a tear during the last 12 months, what’s stopping Ripple’s ledger from difficult SWIFT?

So, why hasn’t Ripple overtaken SWIFT?

Cassie Craddock, managing director for UK and Europe at Ripple, informed Cointelegraph, “We don’t see blockchain as a possibility to switch legacy rails, reasonably a approach of augmenting and modernizing the prevailing monetary infrastructure, creating alternatives for larger effectivity and interoperability.”

Nonetheless, “scaling to the extent of conventional suppliers requires tackling two key hurdles: usability and regulation.”

Relating to regulation, Ripple was, till not too long ago, a part of a very high-profile court docket case.

In December 2020, the SEC below Chairman Jay Clayton sued Ripple Labs for failing to register its XRP tokens as securities below US regulation. The fee alleged that the corporate and its executives raised capital via unregistered securities gross sales. What adopted was an costly, years-long court docket battle.

In 2023, Decide Analisa Torres dominated that the programmatic gross sales of XRP didn’t require securities registration, however that its XPR gross sales to institutional traders did. The court docket didn’t difficulty its last $125-million civil penalty to Ripple till August 2024.

Associated: Ripple vs. SEC: How the lawsuit strengthened XRP’s narrative

By October, Ripple and the SEC had filed respective appeals, however following the election of US President Donald Trump and the realignment of the SEC’s priorities for crypto, each events lastly agreed to drop their case in early August 2025.

The case could have hampered XRP adoption within the US, however throughout the case, it signed partnerships with establishments in quite a few different jurisdictions across the globe. Moreover, the case provides XRP particularly distinctive authorized readability — one thing few cryptocurrencies can boast.

Nonetheless, authorized readability will not be sufficient for Ripple to overhaul the world’s largest funds community, as banks themselves should be satisfied to alter how they function.

Pseudonymous software program engineer and blockchain proponent Vincent Van Code mentioned that platforms utilizing SWIFT “course of billions day by day, however they’re inflexible, pricey, and deeply siloed. A core alternative can take 5–7 years and a whole bunch of tens of millions of {dollars}—an unlimited operational threat.”

They mentioned that banks don’t change their programs as a result of “each financial institution already ‘speaks SWIFT,’ making it the most secure, least expensive choice. Even initiatives like SWIFT GPI are simply patches on an almost 50-year-old basis.”

Van Code concluded that Ripple has to deal with fragile legacy cores and “uneven” international regulation and assuage risk-averse banks — all whereas countering perceptions about its underlying token’s liquidity.

“SWIFT’s ubiquity is its moat, and breaking that community impact will take time.”

Craddock mentioned that “establishments want instruments that really feel acquainted,” and that new rules, notably the GENIUS Act, are a “step towards clear guidelines that give establishments confidence to undertake blockchain in a compliant approach.”

“Stablecoins like Ripple USD are serving to bridge this hole — they’re easy to grasp, pegged 1:1 to the US greenback and behave like money in digital kind. That familiarity is why we’re seeing conventional monetary gamers more and more comfy utilizing crypto and blockchain tech right this moment.”

Personal funds acquire floor

It’s unclear whether or not Ripple can tackle SWIFT sooner or later, overcoming the entrenched enterprise practices of the banking sector and less-than-enthusiastic regulators.

Nonetheless, crypto is ascendant within the US, the place lawmakers are making carveouts for digital property to meet essential roles within the conventional finance system. Congress has clearly expressed its choice for the proliferation of personal stablecoins over a digital greenback or central financial institution digital forex (CBDC).

Congress has not outright banned a CBDC, nevertheless it has created a regulation whereby solely the legislature can create one, excluding the Federal Reserve or business entities. On the identical time, it handed the GENIUS Act, which supplies clear guidelines for stablecoin issuers.

In March, after the SEC dropped its investigation into Ripple, Garlinghouse informed Fox Information that “the market alternative is huge” within the US and mentioned that there’s a possibility to modernize the cost programs from SWIFT.

“The Trump impact is profound […] you’re gonna see that within the adoption of those [blockchain] applied sciences.”

Journal: ChatGPT’s hyperlinks to homicide, suicide and ‘unintentional jailbreaks’: AI Eye